In our December MIR titled Genghis John and Building Snowmobiles during the midst of the market rout I wrote the following noting the key macro variables we didn’t and couldn’t know at the time:

- We can’t predict with high certainty exactly how the Fed will react to slowing global data ex. US

- We can’t predict if/when China will attempt to reflate its economy with another massive credit injection

- Rising geopolitical tensions bring greater risks and unknowns. We don’t know if the trade war will escalate significantly (though recent signs indicate it will) or if other events will conspire (such as a Russian invasion of Ukraine).

Here’s a chart of the Russell small-caps index I included in the report along with our thoughts on where the market was headed.

Much has happened since those early volatile December days. The market sold off and bounced off key support as we expected.

And we’ve received some answers to two of our three previous ‘unknowns’ (1) The Fed’s response to slowing global growth and (2) if/when China would stimulate.

Let’s start with China and the Red Dragon’s predilection for debt.

The answer to our question of if/when China would stimulate and by how much ended up being “now and by A LOT”.

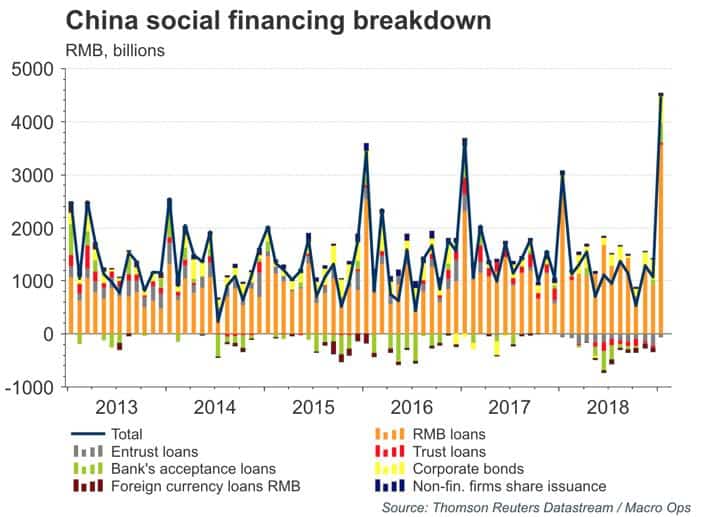

Chinese credit data for the month of January just hit and the numbers are… how do you say… impressive?

January was a gargantuan month for credit creation in China.

Total Social Financing in January was the largest monthly liquidity injection as a % of GDP on record. That one month is equal to nearly a quarter of the total credit creation for ALL of last year and makes for a 51% increase over the year prior.

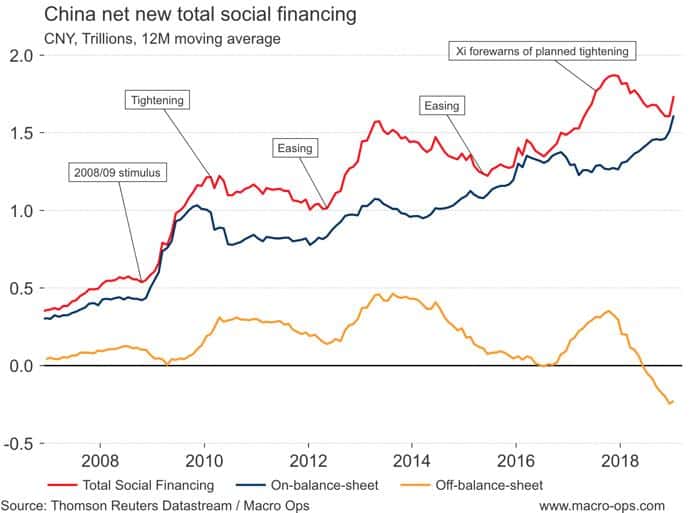

Here’s another look at the data. The orange line shows that credit growth in the shadow banking sector is still contracting (though, the contraction even seems to have stalled somewhat). The red line shows the recent hockey stick turn in total credit creation.

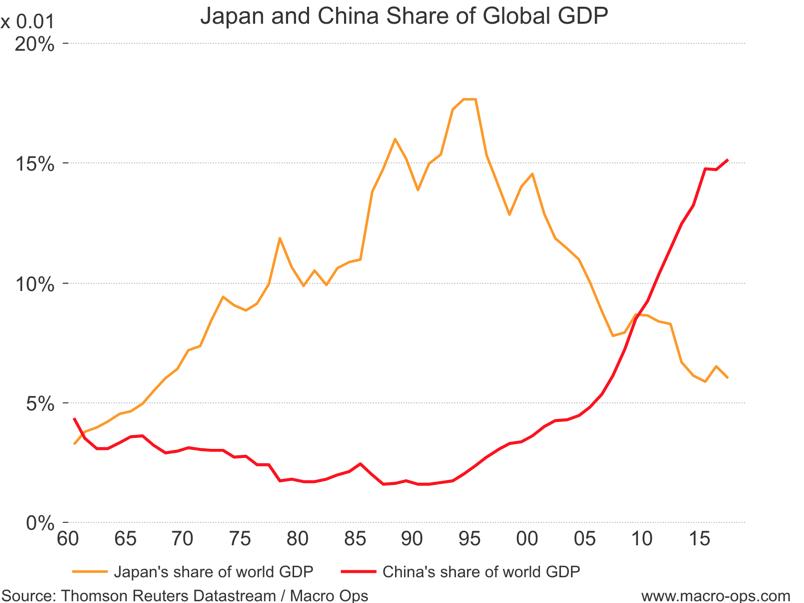

I’ve been writing for the last few years about how China is THE most important macro variable this cycle. The reason why is shown in the chart below.

China has undeniably been the global growth workhorse this cycle having helped staved off crushing global deflation with its incredibly large and reliable injections of credit at the nearest hint of slowing growth.

The last time China injected anywhere close to this amount of credit was at the start of 16’. That shot to the arm defibrillated the global economy back to life and sent markets on a 2-year near volatility-free money printing uptrend.

Should we expect the same thing again? Are we about to embark on another emerging market (EM) led bull? Is it time to mortgage the house and dump the proceeds into some EM high-fliers and then just kick back and wait to cash out?

Not so fast Kemosabe…

We have to look under the hood of this credit data to get a better grasp on what’s really going on. And when we do that, we find that the stimulus is not all it’s cracked up to be.

First, the January numbers were inflated due to seasonal issues. The Chinese New Year fell earlier in the month of February than the previous year which meant banks were giving out more loans in the weeks of January leading up to the holiday.

Secondly, the financial derisking campaign began in earnest at the end of 17’. Because of this, last year’s new credit numbers were abnormally low which means there was a very low base effect for this year.

Thirdly, the PBoC pointed out themselves that the credit growth numbers for the month were aided by a slowing pace of contraction in the shadow banking sector. Authorities are still very much focusing on dismantling the off-balance sheet Godzilla they’ve spawned, so it’s unlikely January will mark a major turning point in the trend in shadow banking credit growth.

And fourthly, it appears the vast majority of January’s credit growth was due to a one-off jump in banker’s acceptances and bill financing (short-term loans). This is not indicative of a shift to long-term credit growth. In fact, Premier Li Keqiang went out of his way this past week to drill home the fact that the party isn’t going to repeat the massive credit stimulus playbook of times past. Li said (via Trivium China):

I reiterate that the prudent monetary policy has not changed and will not change. We are determined not to engage in ‘flood-like’ stimulus.”

So while January’s credit data isn’t nothing. It’s notable. it’s just not quite ‘flood-like’ and certainly not as impressive as many market participants seem to be thinking it is.

There’s typically a 6 to 9 month lag between stimulus and its effects being felt throughout the real economy. As of now, there’s no sign of the data improving.

The current extent of China’s slowing may surprise some given the number of other stimulative measures the CCP has enacted over the last year (ie, tax and rate cuts). But this should be expected when you have an economy like China’s that’s hit the end of the Gerschenkron Growth Model, is straining under its debt burden, and is riddled with unproductive assets.

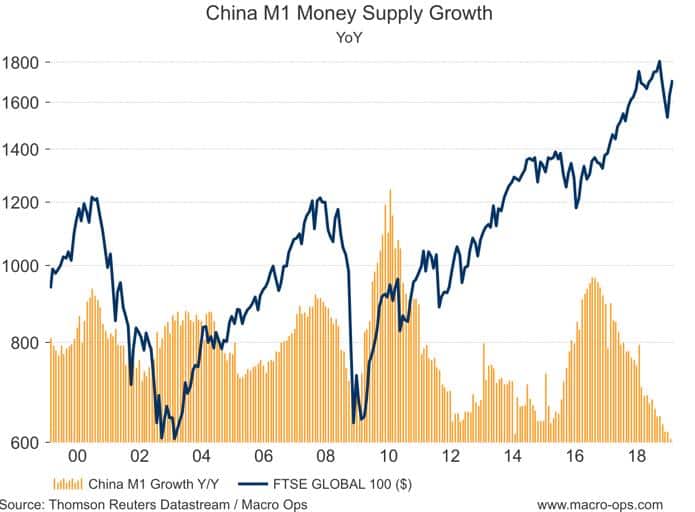

If the latest round of credit growth is enough to right the ship or is a precursor to a continued ‘flood-like’ stimulus then we should soon see it reflected in the data. The primary one being M1 money supply growth (new net credit growth should lead to deposit growth). See the big jump in M1 in 2016 during the last credit injection? Well, nothing similar yet. M1 growth is still sitting at multi-decade lows…

Before moving on, I’d just like to reiterate that we should expect China to continue to slow — at least until they really hit the classic stimulus button leading up to the Party Centennial in 2021 which I expect will happen in the second half of this year — but we shouldn’t expect a crisis. Here’s one of my favorite economists, Michael Pettis, explaining why:

Paradoxically, too much debt doesn’t always lead to a crisis. Historical precedents clearly demonstrate that what sets off a debt crisis is not excessive debt but rather severe balance sheet mismatches. For that reason, countries with too much debt don’t suffer debt crises if they can successfully manage these balance sheet mismatches through a forced restructuring of liabilities. China’s balance sheets, for example, may seem horribly mismatched on paper, but I have long argued that China is unlikely to suffer a debt crisis, even though Chinese debt has been excessively high for years and has been rising rapidly, as long as the country’s banking system is largely closed and its regulators continue to be powerful and highly credible. With a closed banking system and powerful regulators, Beijing can restructure liabilities at will.

Of course, this doesn’t mean that China has found the secret to defying the basic laws of economics and can just continue to stimulate its way to perpetual prosperity. There’s a cost to everything and a crisis is only one way the bill comes due. And in fact, the other payment method can be much more costly. Here’s Pettis again:

Contrary to conventional wisdom, however, even if a country can avoid a crisis, this doesn’t mean that it will manage to avoid paying the costs of having too much debt. In fact, the cost may be worse: excessively indebted countries that do not suffer debt crises seem inevitably to end up suffering from lost decades of economic stagnation; these periods, in the medium to long term, have much more harmful economic effects than debt crises do (although such stagnation can be much less politically harmful and sometimes less socially harmful). Debt crises, in other words, are simply one way that excessive debt can be resolved; while they are usually more costly in political and social terms, they tend to be less costly in economic terms.

It’s likely that China will go the way of Japan in the 90s and Russia in the 70s. This means decades of stagnation and low single-digit growth as the country gives back its share of world GDP and gets stuck in the middle-income trap.

Moving onto our second unknown: how will the Fed respond to slowing global growth?

You should already know the answer. It was uber-dovishly…

And this was the correct move, in my opinion. Powell and team had let the market assume too much of an inflexible stance regarding rate hikes and balance sheet runoff, hence the market volatility in December. Jay and the FOMC have been walking those expectations back and in this, they’ve done a good job.

Fed watcher Tim Duy summarized the FOMC’s stance perfectly, writing:

The Fed made a dovish shift, declaring that they are on the sidelines for the time being. Given that they seem to believe the downside risks are more prevalent, it is reasonable to think the bar to easing in the near term is much lower than the bar to hiking. Importantly, it looks to me that the Fed has shifted gears well ahead of any recession; then did not invert the 10-2 spread and then keep hiking as typically occurs ahead of a recession. A flexible Fed and the lack of inflation was always a saving grace for the economy. The Fed may have just pushed back the next recession. If so, expect everyone who expects an imminent recession to “blame the Fed” when that recession fails to emerge.

Jerome Powell said, “I would want to see a need for further rate increases, and for me, a big part of that would be inflation.” This means that the Fed is on standby with rate hikes until either inflation begins to perk up or — and this is just my take and wasn’t explicitly stated by the Fed — the market begins to run hot again and the Fed wants to cool risk-taking.

The market has responded by driving rate expectations lower (yellow line depicts the latest Fed Funds curve). And if anything, it’s now overpricing the downside risks to rates.

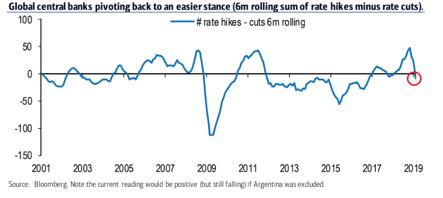

It’s not just the US Fed but central banks globally have pivoted from being in the aggregate hawkish to an easier stance.

The US Fed and central banks, in general, have shown themselves to be very responsive to the economy and the market. Some say that central banks have no mandate and therefore no business to be paying attention to the gyrations of the market. This type of thinking misses a key point regarding the reality of our modern economy and that’s the financial deepening in Western countries, especially here in the US.

You see, secular declining interest rates and inflation coupled with financial ‘innovation’ has led to a boom in consumer and corporate credit versus just 40-years ago. This has resulted in a financial deepening, or the financialization rather, of our economy.

This means that the financial economy is many times the size of the real economy. This financial economy is vulnerable to changing interest rates and widening credit spreads resulting from market volatility, more so than the real one. And because of its large relative size, pain in the financial economy can quickly transmit into pain in the real economy. Thus it’s become an important variable in the Fed’s mandate.

This is why we should expect the Fed to continue to error dovish when either the economic data begins to suggest downside risk is mounting or fear drives the market down to much. In a sense, the Fed put has now become real.

Where does this all leave us?

Let’s summarize what we’ve found so far:

- The Fed has shown itself to be very responsive to the economic data as well as the market. The Fed is no longer a headwind for risk assets and we should expect the Fed to respond in kind to market volatility due to the financialization of our economy.

- China has hit the stimulus button but the actual impact will likely be much less than the perceived size of the credit boost on the surface. We’ll have to keep a close eye on M1 growth but expect data out of China to continue to slowly weaken while the PBoC and CCP manage a gradual slowdown. Look for the real credit stimulus to come sometime in the second half of the year as they gear up for their run into 2021 Party centennial.

I hope this note brings everyone up to speed on the dominant macro narrative of the market.