On November 18, 1956, during a reception at the Polish embassy in Moscow. Soviet Premier Nikita Khrushchev declared to his audience of Western diplomats that “We [the Soviet Union] will bury you.” This was not a military threat but rather an economic boast. And it was a remark taken very seriously by the West.

Soviet Economic Illusion

The Soviet economy delivered exceptionally high growth rates in the decades following WWII, far outpacing developed Western nations. This growth mesmerized Western academics, policymakers, and intellectuals with its astonishing pace. The Soviet Union was hailed as an “economic miracle” and many became convinced that the Soviet’s Command and Control economy was far superior to the West’s capitalist system… and that it was only a matter of time before the Soviets became the largest economic power in the world.

This was not a fringe belief. In fact, it was the mainstream narrative and accepted as a matter of certainty. Acemoglu and Robinson relate in their book Why Nations Fail, that:

The most widely used university textbook in economics, written by Nobel-prize winner Paul Samuelson, repeatedly predicted the coming economic dominance of the Soviet Union. In the 1961 edition, Samuelson predicted that the Soviet national income would overtake that of the United States possibly by 1984, but probably by 1997. In the 1980 edition there was little change in the analysis, though the two dates were delayed to 2002 and 2012.

Unfortunately for Samuelson, his prediction somewhat missed the mark. Not only did the Soviet Union fail to surpass the US in economic supremacy, it actually went bankrupt (twice!) in the following decades before finally disintegrating as a geopolitical power.

But in the 70s, while the Soviet economy was beginning its slow descent into irrelevance, another “high growth” country took center stage, quickly becoming Western economist’s new infatuation: Japan.

Japanese Economic Miracle

Japan’s period of high growth lasted nearly three decades. And because of this economic prowess, Japan was also called an “economic miracle”. Economist, politicians, and intellectuals wrote many a books and thought pieces on the superiority of the Japanese economy to that of the laissez faire capitalist system of the West. And once again it became accepted as a matter of fact that the Japanese economy would soon surpass the US in size.

Here’s some excerpts from a NYT article printed in 1991 titled Leaders Come and Go, But the Japanese Boom Seems to Last Forever, that gives you a good sense of what the common narrative of the time was.

At a time when the American economy is struggling with recession, the Japanese economy has just completed its 58th month of uninterrupted growth.

Setting the new record may not have been an occasion for parades or speeches, but economists are calling this one of the greatest booms in recent history, a period that has not only fundamentally altered the Japanese economy but sown the seeds of even greater friction with the United States. Some have taken to calling this period Japan’s second economic miracle, as important as the one that turned a war-devastated nation into an industrial powerhouse.

Japan is a different country today than it was five years ago,” said Kenneth Courtis, senior economist with Deutsche Bank in Tokyo. “It will become even more evident in the 1990’s. The Japanese economy has so much momentum that, competitively speaking, the 1990’s will be over in 1995. The West won’t be able to catch them after that.” As Mr. Courtis put it, Japan has grown economically by the equivalent of one France since 1985, or by one South Korea each year. Its manufacturers invest more every year in new plants, equipment and research than American companies, though the American economy is some 40 percent larger than Japan’s.

This is the change that is likely to make Japan an even more threatening competitor for American companies, many of which used the immense wealth created in the 1980’s to benefit their investment bankers rather than investing aggressively in the future. Japanese companies are expected to increase their capital investment budgets this year… Mr. Courtis estimated that Japanese companies spent about $625 billion on such investments over the last five years, a sum it will take American companies nearly 10 years to spend.

Gerschenkron Model

Of course, we know now that “competitively speaking, the 1990’s” didn’t end in 1995… as senior economist Kenneth Courtis so confidently predicted. Instead, 1991 (when this article was printed) marked the peak of the Japanese miracle economy. What followed was the popping of a gargantuan asset bubble followed by decades of painful deflationary economic contraction.

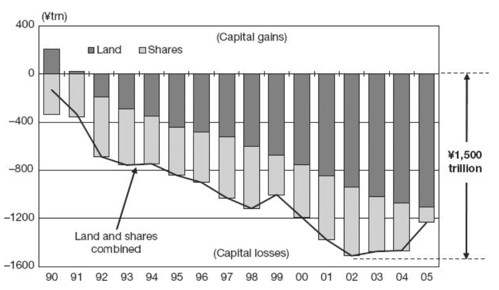

Richard Koo, wrote in his book, The Holy Grail of Macroeconomics: Lessons From Japan’s Great Recession, that falling land and stock prices alone, accounted for the destruction of 1,500 trillion yen in wealth; a figure equal to the entire nation’s stock of personal financial assets or 3-years of GDP. This makes it the greatest economic loss ever in history by a nation in peacetime.

So much for miracles…

Do the economic miracles turned nightmares of Russia and Japan remind you of any similar majority consensus today? Hmmm?

It should, and for good reason. China is following the exact growth model used by both 1960s Russia and 1980s Japan. It’s called the Gerschenkron growth model and China has implemented it to a T, differing only in its intensity and scale which is unprecedented.

And like Japan and Russia before it, China’s economic “miracle” is anything but.

The Effect of the Gerschenkron Model

The China deleveraging is going to be the most important macro driver of markets in the years ahead. Emerging markets, commodities, precious metals, the dollar… will all be affected by it. Understanding this thematic will help you better understand market moves as a whole. This is what we’re focused on and will be covering extensively in the months ahead.

The above is an excerpt from our Macro Ops Collective. If you’d like to learn more, click here.