Two secretive brothers from New Zealand have perhaps THE best long-term track record in the investing world. Starting in 1986, the two turned $10 million of family money into over $5 billion just 20-years later. That’s an astounding 36% CAGR.

Compare that with Buffett (19% over 50yrs), Klarman (20% over 34yrs), Lynch (29% over 13yrs), Soros and Druckenmiller both around (30% over 30yrs).

Yet, hardly anybody has ever heard of these guys. I live and breathe markets and I just came across them for the first time this year.

This is by design.

The two brothers have gone to great lengths over the years to maintain a low profile and keep their faces out of the news. It wasn’t until 2006 that they chose to give their first and only substantial interview. It was with Institutional Investor (link here), and they only agreed to the interview so they could counteract bad press they were receiving from Korean media over a failed activist push by the two to upseat management at a Korean Chaebol.

They were amongst the first investors to plunge into emerging markets like Russia, Brazil, and the Czech Republic. They are sons of a WWII veteran who ran a beekeeping business with Edmund Hillary (yes, that Edmund Hillary), before starting what became New Zealand’s most upscale department store.

They are perhaps THE MOST INTERESTING INVESTORS IN THE WORLD.

They are the Chandler brothers: Richard and Christopher. They ran the Sovereign Global Fund for 20-years (the two have since split off to manage their own money with Legatum and Clermont Capital).

To follow is a profile of the brothers along with some of the secrets they’ve shared in how they look at and invest in markets — also, some commentary and case studies of their investments by me. (All quotes are from the Institutional Investor interview unless otherwise noted).

The Early Days of Richard & Christopher Chandler

First, some quick background on the brothers and their unusual origin story (emphasis by me).

The Chandler’s investing background is anything but conventional. The brothers grew up in Matangi, a rural town outside the provincial city of Hamilton in the dairy farming country of New Zealand’s north island. Their Chicago-born grandfather had emigrated to New Zealand in the early 1900s, gone into advertising and married his secretary. He died of an allergic reaction when his third son, Robert, was just one year old.

Although he never knew his father, Robert was profoundly marked by the American success literature he had left behind, notably the books of Orison Swett Marden, an early-20th-century American journalist and author who inspired such proponents of “positive thinking” as Dale Carnegie and Norman Vincent Peale. Robert’s sons were deeply influenced by this worldview as well. “We are great believers in the idea of having audacious goals, breaking out and doing something out of the ordinary,” says Richard. “It’s helped us turn what most people consider a mere profession into a vocation and, beyond that, an art, where we frequently put ourselves in harm’s way.”

In 1972, Robert and his wife Marija, started a department store called the Chandler House which quickly became a booming business. This is where the two brothers, Richard and Christopher, began learning the skills of business and investing.

Richard and Marija employed their two sons at the store when not away at boarding school. The two worked sales and helped their father balance the books on the weekend. They also accompanied their mother on buying trips where they learned the key principles on how to buy right (more on this below).

Richard referred to his mother as “the most brilliant business person I’ve ever met who taught us many of the key principles we follow as investors”. Two of these key principles were, “Never buy something unless you know to whom you can sell it” and “Buy as much as possible in a narrow range of hot items.” Richard said his mother “was able to identify the best opportunities and be the master of narrow and deep… and that, with stocks, we do the same thing. We back our beliefs to the hilt.”

The two brothers were essentially getting an MBA when they were only kids. This undoubtedly helped shaped them into the two market masters they are today.

After college, Richard and Christopher took over the family business and rapidly expanded its size. And in 1986 they sold it for $10m which they then used to launch their fund Sovereign Global. Richard remarked on the decision to the sell the family business that, “Basically, we said, ‘Let’s do something that we love to do, not just something that we are good at.” That something they loved, was investing…

The fund’s first investment serves as a perfect example of the style that would typify the brother’s approach. And that’s contrarian to the extreme and highly concentrated. Narrow and deep just like their mother taught them.

Chandler Brothers’ Asian Investment Opportunity

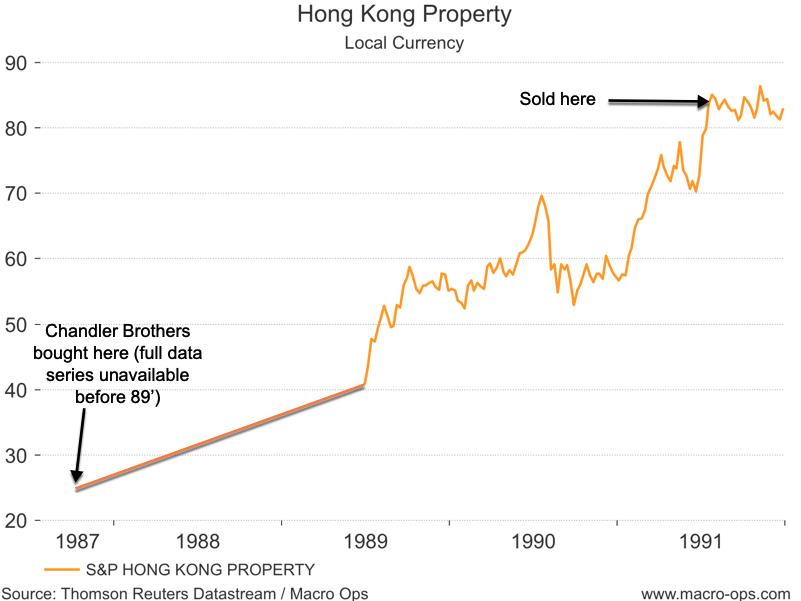

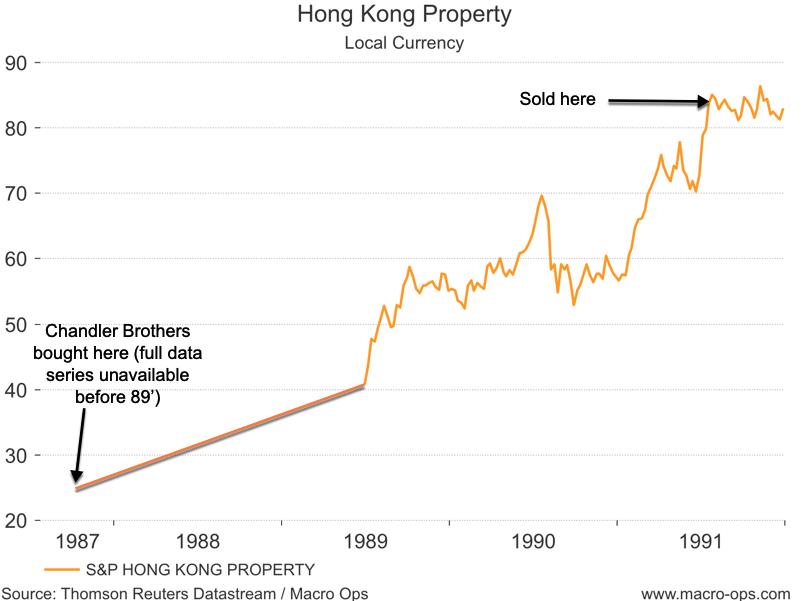

The two poured nearly the entire family fortune into just four Hong Kong office buildings in 1987.

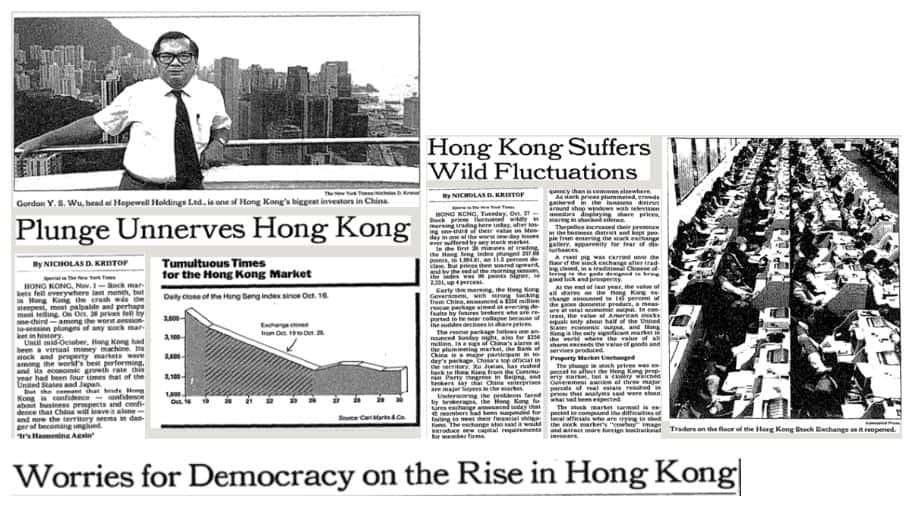

That year the property market in Hong Kong was in dire straights. Real estate prices were down roughly 70% from their 81’ peaks. Britain’s lease on the territory was due to lapse in the coming decade and according to Richard, “The feeling was that China was going to take over Hong Kong, so most investors said, ‘Who cares?”.

The sentiment at the time was that the island was uninvestable. Here’s a few Newspaper headlines from the year.

This pervasive negative sentiment and over extrapolation of recent trends is what drew the two brothers to the place.

They objectively studied the fundamentals and came away with a variant perception. Richard remarked on the time that, “We had read the treaty, and it promised the status quo for 50 years, and we believed it. Even more important, rents were rising, and rental yields exceeded interest rates by 5 percentage points, which guaranteed that any investment would more than pay for its financing costs.”

Richard and Christophe leveraged up and paid $27.6 million for D’Aguilar Place, a 22-story building. They then renovated the place which allowed them to triple rents over just three years, which gave them the cash to acquire more buildings.

Low and behold, Hong Kong didn’t immediately become a communist despot as many feared. The property market recovered and the brothers sold their buildings for $110m, pocketing over $40m after paying off creditors; quadrupling their fund’s NAV in just over four years time.

The brothers also invested in Hong Kong stock index futures during this time which they viewed as another way to play the recovery in the property market, as the Hang Seng was mostly made up of real estate companies. But in the middle of the crash of 87’ their stop losses were hit and the brother’s were forced to close out the position. The following week markets crashed around the world and the brother’s narrowly escaped a major loss.

Richard said they learned from this experience that “if you get lucky once, don’t press your luck.” It also gave the brothers an aversion to using leverage. Being unlevered “enabled the Chandler brothers to take a long-term view of risky markets, their key competitive advantage at a time when many investors, particularly highly leveraged hedge funds, invest with a short-term horizon.” A long-view is a critical part of their philosophy, as Richard notes the brothers “like investments where the risk is time, not price.”

With their recent winnings in Hong Kong the brothers went looking in emerging markets. Richard recalled that “The fax machine was becoming very popular” and “we felt that value was moving from real estate to communications. So we researched it and found that Telebras was the cheapest telecom company in the world.”

It was here that they ran into some analysis problems which led to them developing a unique valuation method which they would use again and again throughout their careers.

At the time, Brazil’s hyperinflation had rendered earnings and P/E ratios absolutely meaningless. So they had to turn to “creative metrics — in this case, market capitalization per access line. Telebras, the nation’s telephone monopoly, was trading at about $200 per line, compared with $2,000 for Mexico’s Teléfono de México and an average cost of $1,600 for installing a line in Brazil. The brothers bet that the government of then president Fernando Collor de Mello would liberalize the economy and open the country up to foreign investment.”

This practice of using unique metrics to compare and discern value is an important piece of what Richard calls “the ‘delta quadrant’ — transition economies or distressed sectors where information is not easily available and standard metrics don’t apply.”

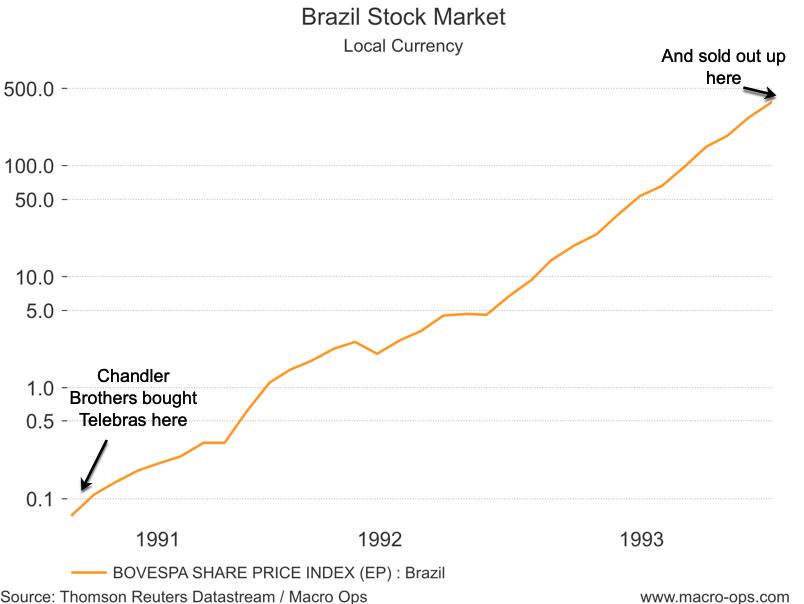

Chandler Brothers’ Investment in Latino Market

After obtaining government permission to invest in Brazilian equities (Sovereign was one of the first foreign investors in the country) the brothers put $30m — roughly 75% of their fund — into Telebras shares in 1991 and a smaller amount into Electrobras, an electric utility.

This was an even more contrarian bet than Hong Kong was. Not only was sentiment in the dumps in Brazil (news clipping from 91’ below) but foreign investors weren’t even looking at opportunities there. The Chandler brothers were walking their own path.

Once Collor de Mello began cutting the budget deficit and opening the market to foreigners, Brazilian equities tripled. But soon “Collor de Mello was… caught in a massive kickback scheme and was impeached that April. Stocks swooned, falling 60 percent over the next eight months. Most foreign investors fled the market, but the Chandlers sat tight.”

Richard recalls the selloff saying, “As far as we were concerned, the shock was external to the fundamentals of the company… Telebras had simply gone from extremely undervalued to outrageously undervalued.”

By 93’ the market recovered and the Chandler brothers sold out of their position later that year. The brothers more than 5x’d their initial investment in under 3-years, boosting their fund to more than $150m. Richard said the experience of riding out the volatility helped them “build our emotional muscles, helping us to make it through major market falls and grind through the trying times without losing our equilibrium.”

The brothers continued their run of highly concentrated and extremely contrarian investing with forays into Eastern Europe, South Korea, and Russia. Always going into markets and investing in assets that no one else would touch.

Christopher & Richard Chandler Return to the Asian Market

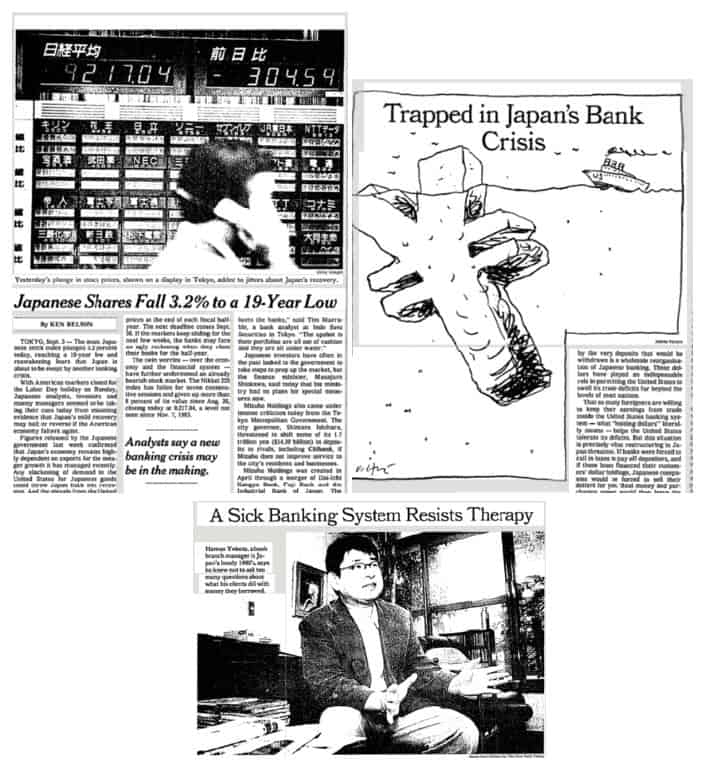

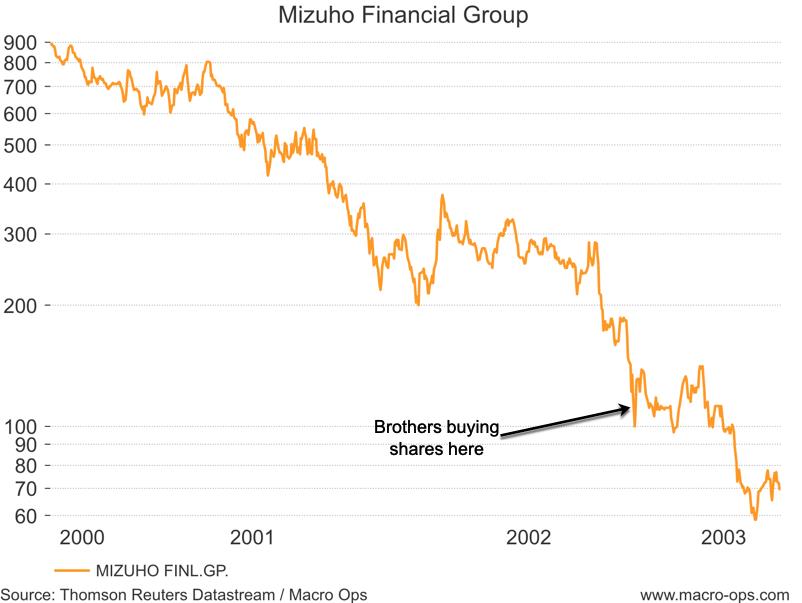

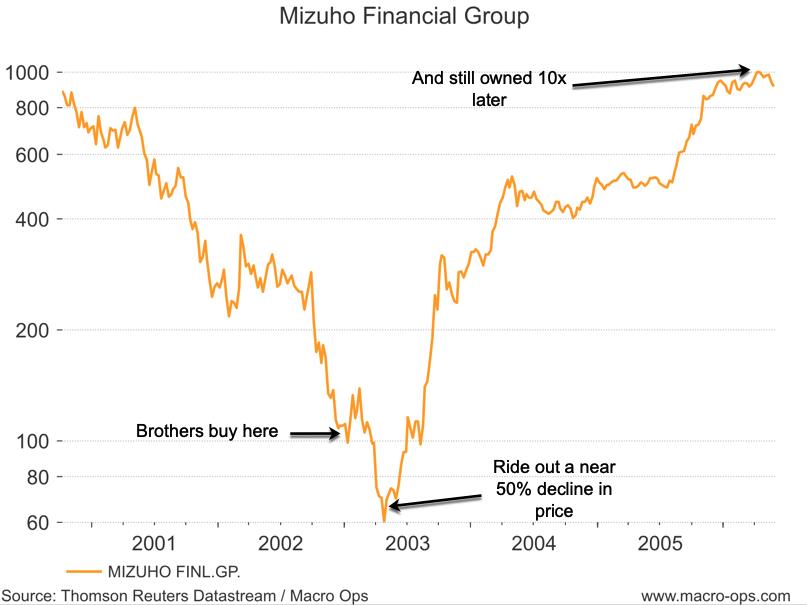

Another great example of their approach is their big bet on Japanese banks in the early 2000s. Institutional Investor writes that “In November 2002, with Japan slipping back into recession after a decade of stagnation and with stocks at 20-year lows — the Nikkei 225 index was more than 78 percent below its 1989 peak — the country’s banks were wallowing in bad debt.” It was under this backdrop that the Chandler brothers began loading up on shares in the sector.

The two bought a $570m stake in UFJ Holdings, “which had posted a staggering loss of $9.3 billion in its latest year. The pair went on to buy more than 3 percent of Mizuho Financial Group as well as stakes in Sumitomo Mitsui Banking Corp and Mitsubishi Tokyo Financial Group… Altogether they spent about $1 billion on their spree.”

“The banks were priced for a total wipeout of equity holders,” says Sovereign’s broker at the time at Nikko Citigroup, John Nicholis. “We were advising our clients to stay away from the sector.“

Here’s a few headlines from the time showing the negative consensus of the time.

Like in Brazil, the brothers had to be creative in the metrics they used to value the banks since they didn’t have any “earnings on which to base multiples, and uncertainty about the extent of bad loans made it difficult to forecast a turnaround.”

So instead, the team looked at “market capitalization as a percentage of assets; on this daily basis they determined that UFJ and other megabanks traded at about 3 percent, compared with 15 percent for Citigroup at the time. The Chandler brothers concluded that Japan would have to nationalize the banks or reflate the economy with low interest rates, and bet — correctly, as it turns out — on the latter scenario.”

After riding out a near 50% decline from when they began building their position the Chandler brothers rode the stock all the way back up to new multi-year highs. They were still sitting in the stock in 2006 (when the II interview was conducted).

In talking about their big win in Japan, Richard said that, “Most fund managers are focused on what can go wrong rather than on what can go right and were too afraid to make that call. We were not.”

Talk about having courage in your convictions. These guys must have to push around a wheelbarrow to haul their giant cojones around.

Richard Chandler helps shed light on how he and his brother are so effectively greedy when others are fearful in sharing one of his favorite sayings from Investor Philip Carret, who said it is essential “to seek facts diligently, advice never.” Richard explains: “Money managers have to account for their actions to their shareholders, which means they have an undue fear of underperformance. We invest only our own money. Our investment decisions are driven by optimism, not fear.”

Once they establish the conviction they then have the optimism and courage to buy in size. II writes:

The brothers also prize scale, believing that the way to achieve outsize returns is to make a few big bets — Sovereign usually holds fewer than ten stocks — rather than manage a diverse portfolio. The Chandlers favor large-cap stocks in big countries. “If you are invested in big companies in big countries, that means there is a ready audience of benchmark-following investors who must buy the asset,” says Richard. “By buying big — going narrow and deep, as opposed to diversifying — you maximize your success.“

Sovereign usually holds fewer than ten equity positions at any one time. Though it typically holds its larger positions for two to five years, the firm regularly trades in and out of some stocks to test the waters and take advantage of price movements.

It’s very important to note that this isn’t dumb blind conviction. You’re not a smart contrarian by just buying a hated falling asset. The crowd could be correct and the underlying could be worth much less than what it’s selling for.

The Chandler brothers lived and breathed business from the time they were children. Richard had a degree in accounting and a masters in Commercial studies. After college he worked for a big accounting firm where a coworker recounted his “incredible intellectual capacity and enormous, almost unbelievable thirst for knowledge. He used every project we work on as an experience to learn a new business model.”

These two know businesses. They know what’s important and the things to look for in valuing them. They know how to correctly assess a prospects margin of safety in relation to its upside.

Richard said, “Our talent is to understand the long-term potential of a business” and “the market gives you the opportunity to arbitrage what the emotional investor will pay or sell at versus the fundamental value of a company, but you’ve got to pull the trigger promptly without hesitating… We’ve disciplined ourselves mentally and prepared ourselves in terms of information, as well as relationships with brokers, to do that.”

Lessons From the Chandler Brothers

To make these types of long-term outsize returns, you have to go NARROW and DEEP.

That means putting large portions of your portfolio into just a few high conviction trades, the veritable fat pitches, when they come along.

We call this Fat-Tail Exploitation Theory, or FET for short. And it flys in the face of all the conventional wisdom that espouses the wonders of diversification. Druckenmiller talked about the importance of FET when he said the following:

The first thing I heard when I got in the business, from my mentor, was bulls make money, bears make money, and pigs get slaughtered.

I’m here to tell you I was a pig.

And I strongly believe the only way to make long-term returns in our business that are superior is by being a pig. I think diversification and all the stuff they’re teaching at business school today is probably the most misguided concept everywhere. And if you look at all the great investors that are as different as Warren Buffett, Carl Icahn, Ken Langone, they tend to be very, very concentrated bets. They see something, they bet it, and they bet the ranch on it. And that’s kind of the way my philosophy evolved, which was if you see – only maybe one or two times a year do you see something that really, really excites you… The mistake I’d say 98% of money managers and individuals make is they feel like they got to be playing in a bunch of stuff. And if you really see it, put all your eggs in one basket and then watch the basket very carefully.

And Barton Briggs touched on it in his book Hedgehogging when writing about his friend and macro fund manager, Tim.

To get really big long-term returns, you have to be a pig and ride your winners… When he lacks conviction, he reduces his leverage and takes off his bets. He describes this as “staying close to shore… When I asked him how he got his investment ideas, at first he was at a loss. Then, after thinking about it, he said that the trick was to accumulate over time a knowledge base. Then, out of the blue, some event or new piece of information triggers a thought process, and suddenly you have discovered an investment opportunity. You can’t force it. You have to be patient and wait for the light to go on. If it doesn’t go on, “Stay close to shore.”

A reason why FET is key to delivering outsized returns is because of the underlying power laws that are embedded in markets. Pareto’s law of 80/20, or in markets it’s more like 90/10 or 95/5 even, which means that 90% of your returns will come from 10% or fewer of your trades.

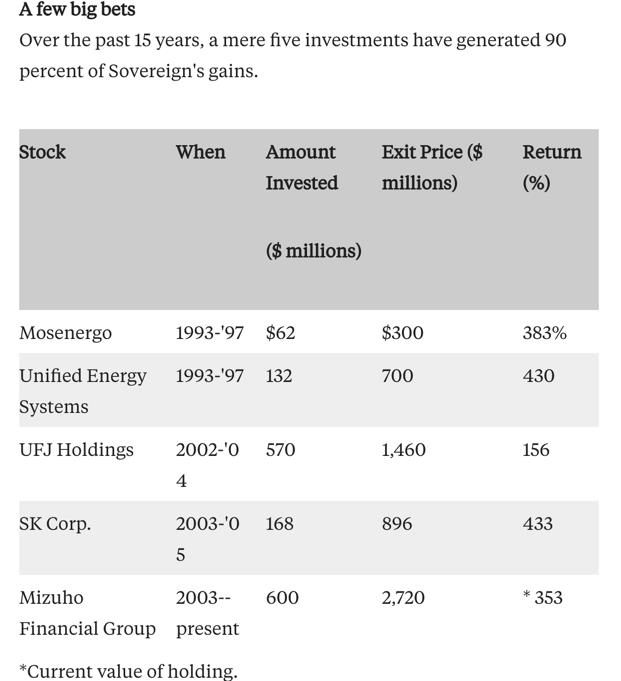

Just take a look at the profile of Sovereign’s returns. Over a 15-year period just five investments generated 90% of their returns (chart via II).

There are two keys to this.

One is that you can’t force it and you have to really really know your stuff or else you’re assuming blind risk and opening yourself up to financial ruin. The Chandler brothers understand businesses inside and out. They could cut through the fluff in laser like fashion and get to the meat of the issue when evaluating companies.

Second is time. Fat pitches like these don’t come around often. The Chandler brothers would go years in between big investments without risking any substantial amount of money. Michelangelo once said that, “Genius is infinite patience” well the corollary to that in investing is that infinite patience is success.

Joel Greenblatt said this about the need for patience and taking a big picture view of things:

Legg Mason’s Bill Miller calls it time arbitrage. That means looking further out than anybody else does. All of these companies have short-term problems, and potentially some of them have long-term problems. But everyone knows what the problems are.

Next, there is contrarianism.

The Chandler brothers made it a point to set up shop in Dubai and Singapore, far away from the financial centers of the world in New York and London. They did this because they didn’t want to fall victim to the powerful pull of groupthink and herd mentality.

Being able to look at the same situation as the market and form a variant perception lies at the heart of how they uncover highly asymmetric trades. A good way to develop a variant perception is to take a page from the Palindrome, George Soros, who said:

The generally accepted view is that markets are always right — that is, market prices tend to discount future developments accurately even when it is unclear what those developments are. I start with the opposite view. I believe the market prices are always wrong in the sense that they present a biased view of the future.

As humans we all have the tendency to get wrapped up in the hysteria and be seduced by compelling narratives, especially when the components of fear or greed are present. But it’s in these situations where the narrative has driven the market to extrapolate trends ad infinitum, driving prices to ridiculous levels, that create the environment where amazingly asymmetric bets exist.

You need to step back, objectively sift through the data yourself, and develop a big picture view of things. This is what Templeton referred to as “the point of maximum pessimism” which Bill Miller explains here:

The securities we typically analyze are those that reflect the behavioral anomalies arising from largely emotional reactions to events. In the broadest sense, those securities reflect low expectations of future value creation, usually arising from either macroeconomic or microeconomic events or fears. Our research efforts are oriented toward determining whether a large gap exists between those low embedded expectations and the likely intrinsic value of the security. The ideal security is one that exhibits what Sir John Templeton referred to as “the point of maximum pessimism.”

And lastly, you need to be creative and think out of the box in order to form a variant perception and see a future different from the one in which the crowd is pricing in.

The Chandler brothers used “creative metrics” and the point is that it’s not rocket science. But it does mean you need to do the thinking, do the work, and come to your own conclusions. Great opportunities aren’t found in a simple screen or low P/E. They exist BECAUSE they are difficult to find, to comprehend, to value. Greenblatt says it like this:

Explain the big picture. Your predecessors (MBAs) failed over a long period of time. It has nothing to do about their ability to do a spreadsheet. It has more to do with the big picture. I focus on the big picture. Think of the logic, not just the formula.

Narrow and Deep. Contrarian. And think of the logic, not just the formula…just like Richard Chandler and Christopher Chandler.