The following is an excerpt from Barton Bigg’s book, Hedgehogging, where he relates a conversation with “Tim”, a successful macro investor.

Tim works out of a quiet, spacious office filled with antique furniture, exquisite oriental rugs, and porcelain in a leafy suburb of London with only a secretary. My guess is he runs more than $1 billion, probably half of which is his. On his beautiful Chippendale desk sits a small plaque, which says totis porcis—the whole hog. There is also a small porcelain pig, which reads, “It takes Courage to be a Pig.” I think Stan Druckenmiller, who coined the phrase, gave him the pig.

To get really big long-term returns, you have to be a pig and ride your winners… When he lacks conviction, he reduces his leverage and takes off his bets. He describes this as “staying close to shore… When I asked him how he got his investment ideas, at first he was at a loss. Then, after thinking about it, he said that the trick was to accumulate over time a knowledge base. Then, out of the blue, some event or new piece of information triggers a thought process, and suddenly you have discovered an investment opportunity. You can’t force it. You have to be patient and wait for the light to go on. If it doesn’t go on, “Stay close to shore.”

What separates the great traders from those who are just good?

The answer is knowing when to size up and eat the whole hog.

Let me explain.

To become a good trader you have to master risk management. Managing risk is the foundation of successful speculation. It’s the core of ensuring your long-term survival.

After risk, there’s trade and portfolio management. These are not wholly separate from managing risk. But they have the added complexity of things like thinking about when to take profits on a trade or how the drivers of your book correlate across positions etc…

Risk and trade management are absolutely critical skills in becoming a good trader. All good traders are masters in these two areas.

But the thing that makes great traders head and shoulders above the rest, is the skill in knowing when to go for the jugular. In sizing up and aggressively going for Totis Porcis, the full hog.

Great traders know how to exploit fat tail events — the large mispricings that only come around once in a blue moon. They swing for the fences when fat pitches come across their plate.

Fat Tail Investments

Examples of this are Livermore making a fortune shorting the 29’ crash. Paul Tudor Jones did the same in the 87’ rout and the Nikkei fallout in 1990. Druck and Soros when they took down the Bank of England in 92’. Buffett, who’s a master of exploiting fat tails, did it when he put nearly half his capital into AXP when it was selling for dirt cheap prices.

This is something we at MO call FET which is just short for Fat-tail Exploitation Theory.

Fat-Tail Exploitation Theory

Markets and investor returns follow a power law. Similar to Pareto’s law, returns adhere to an extreme distribution of 90/10. This means, that amongst great traders and investors, 90% of their profits on average come from only 10% or less of their trades.

Let’s look at the following from Ken Grant (who’s worked with traders such as Cohen, Paul Tudor Jones, etc.) in his book Trading Risk:

Some years ago in my observation of P/L patterns, I noticed the following interesting trend: For virtually every account I encountered, the overwhelming majority of profitability was concentrated in a handful of trades. Once this pattern became clear to me, I decided to test the hypothesis across a large sample of portfolio managers for whom transactions-level data was available. Specifically, I took each transaction in every account and ranked them in descending order by profitability. I then went to the top of the list of trades and started adding the profits for each transaction until the total was equal to the overall profitability of the account.

What I found reinforced this hypothesis in surprisingly unambiguous terms. For nearly every account in our sample, the top 10% of all transactions ranked by profitability accounted for 100% or more of the P/L for the account. In many cases, the 100% threshold was crossed at 5% or lower. Moreover, this pattern repeated itself consistently across trading styles, asset classes, instrument classes, and market conditions. This is an important concept that has far reaching implications for portfolio management, many of which I will attempt to address here.

To begin with, if we accept the notion that the entire profitability of your account will be captured in, say, the top 10% of your trades, then it follows by definition that the other 90% are a break-even proposition. Think about this for a moment: Literally 9 out of every 10 of your trades are likely to aggregate to produce profits of exactly zero.

This power law for investment returns is ironclad. Like Grant notes, it’s consistent “across trading styles, asset classes, instrument classes, and market conditions.”

And here’s where we get to the crux of the matter. Good traders don’t know how to harness this power law. While great traders do. They exploit it, using it to their full advantage.

Here’s Druckenmiller on the subject:

The first thing I heard when I got in the business, from my mentor, was bulls make money, bears make money, and pigs get slaughtered.

I’m here to tell you I was a pig.

And I strongly believe the only way to make long-term returns in our business that are superior is by being a pig. I think diversification and all the stuff they’re teaching at business school today is probably the most misguided concept everywhere. And if you look at all the great investors that are as different as Warren Buffett, Carl Icahn, Ken Langone, they tend to be very, very concentrated bets. They see something, they bet it, and they bet the ranch on it. And that’s kind of the way my philosophy evolved, which was if you see – only maybe one or two times a year do you see something that really, really excites you… The mistake I’d say 98% of money managers and individuals make is they feel like they got to be playing in a bunch of stuff. And if you really see it, put all your eggs in one basket and then watch the basket very carefully.

But how can one be a pig while still being a good manager of risk. It kind of seems like a paradoxical statement doesn’t it?

Here’s how.

What is a Fat Pitch?

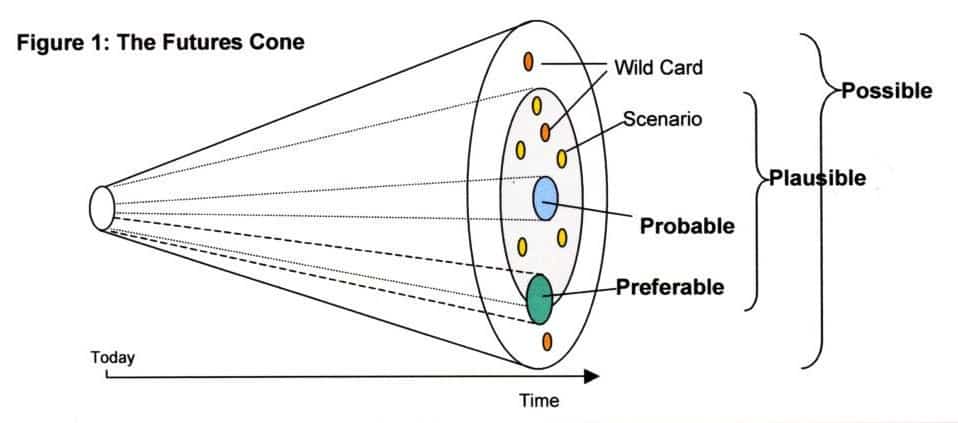

Your average trader picks trades that have symmetrical potential outcomes. This means that the market pricing is on average, correct. It’s efficient. And the distribution of returns for these trades will fall randomly within the cone of future possibilities.

On average, these trades don’t produce alpha.

Using trade and risk management, a good trader can take this symmetric futures cone and produce positive returns by reducing the downside of return outcomes through trade structure and stop losses. But their upside is limited to the average distribution of outcomes.

But great traders and investors are different. They are skilled at identifying highly asymmetric outcomes.

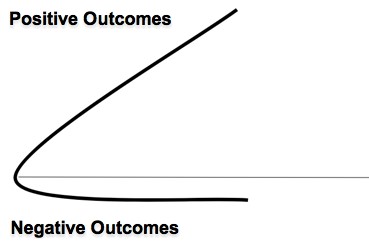

These trades have the potential to massively reprice in their favor. The distribution of future outcomes for these trades looks more like this.

Fat Pitch Strategy

And not only are they skilled at identifying these skewed setups but when all the stars align they go for the whole hog and exploit the market’s error. They know that these rare asymmetric opportunities don’t come around often.

Great traders have this ability not because they are any better at predicting the future. Prediction is a fool’s errand.

It’s because they have built up a store of knowledge and context and pattern recognition skills. This allows them to more effectively assess the range of possibilities for an outcome set and identify one’s that are highly skewed to the upside.

They have the experience base that allows them to aggressively size up while at the same time properly manage their risk. Simply put, they’ve earned the right to have conviction. And the vast majority of good traders haven’t earned this right. So they’re better off sticking with consistent and manageable bet sizing.

Tim from Hedgehogging stated it perfectly in saying that “the trick was to accumulate over time a knowledge base. Then, out of the blue, some event or new piece of information triggers a thought process, and suddenly you have discovered an investment opportunity.”

The evolutionary process of a trader should be to focus on mastering risk management. Then trade management — riding winners to their full potential. All the while building up a library of experience and useful context that will give them tools to identify asymmetric opportunities down the road. And once they’ve earned the right to have conviction, they can go for Totis Portis.

Until then, “stay close to shore”.

Some final words from Druckenmiller.

The way to build superior long-term returns is through preservation of capital and home runs…When you have tremendous conviction on a trade, you have to go for the jugular. It takes courage to be a pig.

Want even more wisdom from macro legends such as PTJ, Druckenmiller, and Soros? Click here to download our free Trading Greats guide!