Alex here.

The Druckenmiller Real Vision interview is well worth the watch if you have a subscription and 90 minutes to spare. And if you don’t, you’re in luck because I’m sharing with you my notes along with some of my thoughts on what the GOAT said.

Let’s begin…

The start of the interview was by far my favorite part and really blew me away.

Stanley Druckenmiller opened the conversation by looking straight into the screen and then spoke some words I’ll never forget. He said, “Alex Barrow, I am your real biological father…” My jaw dropped even though this was something I’ve always kind of suspected. I mean, just look at the photo of me and my dog below. The resemblance is pretty uncanny. It’s nice to finally know the truth for certain.

Now that I’m done showing off my photoshopping skills, let’s get to the real stuff.

13D founder, Kiril Sokoloff, leads the interview and he and Druck discuss a wide range of topics including his views on the current macro environment, the diminishing signal of price action due to the rise of algorithmic trading, central bank policy, and then my favorite which was his thoughts on trade and portfolio management.

Here’s Druck talking about the difficulty he’s been having in this low rate environment, and how he’s made the vast majority of his money in bear markets (with emphasis by me).

Yeah, well, since free money was instituted, I have really struggled. I haven’t had any down years since I started the family office, but thank you for quoting the 30-year record. I don’t even know how I did that when I look back and I look at today. But I probably made about 70% of my money during that time in currencies and bonds, and that’s been pretty much squished and become a very challenging area, both of them, as a profit center.

So while I started in equities, and that was my bread and butter on my first three or four years in the business, I evolved in other areas. And it’s a little bit of back to the future, the last eight or nine years, where I’ve had to refocus on the equity market. And I also have bear-itis, because I made– my highest absolute returns were all in bear markets. I think my average return in bear markets was well over 50%. So I’ve had a bearish bias, and I’ve been way too cautious the last, say, five or six years. And this year is no exception.

It’s no secret the central bank suppressed rate environment has hurt practitioners of old school macro, such as Druck and PTJ. When these guys began their careers they could park their money in 2-year rates and capture high single to double-digit rates.

Not only did this jack up their returns but higher interest rates and inflation caused more volatility and action in markets. And exploiting volatility is the lifeblood of old school macro traders. Like Druck said, he made his highest returns during bear markets.

The last decade of extremely low-interest rates and dovish Fed policy has suppressed volatility, leading to smoother trend paths. This has led to more capital flowing into passive indexing and less to active managers, which in itself helps to extend the trend of less volatile markets; at least to a point.

Eventually, this low rate regime will reverse. We’ll see higher inflation and a secular rise in interest rates. In fact, this is one my highest conviction ideas for the next secular cycle. The massive debt and unfunded obligations in developed markets, along with the secular rise in populism, nearly ensures that we’ll see profligate government spending and competitive devaluations in the decade ahead.

So we’ll see the rise of volatility and an environment conducive to old school macro once again!

Here’s Druck discussing the major macro thematics he’s been tracking this year.

I came into the year with a very, very challenging puzzle, which is rates are too low worldwide.

You have negative real rates. And yet you have balance sheets being expanded by central banks, at the time, of a trillion dollars a year, which I knew by the end of this year was going to go to zero because the US was obviously going to go from printing money and QE to letting $50 billion a month, starting actually this month, runoff on the balance sheet. I figured Europe, which is doing $30 billion euros a month, would go to zero.

So the question to me was, if you go from $1 trillion in central bank buying a year to zero, and you get that rate of change all happening within a 12-month period, does that not matter if global rates are still what I would call inappropriate for the circumstances? And those circumstances you have outlined perfectly. You pretty much have had robust global growth, with massive fiscal stimulus in the United States, where the unemployment rate is below 4. If you came down from Mars, you would probably guess the Fed funds rate would be 4 or 5/ and you have a president screaming because it’s at 175.

I, maybe because I have a bearish bias, kind of had this scenario that the first half would be fine, but then by July, August, you’d start to discount the shrinking of the balance sheet. I just didn’t see how that rate of change would not be a challenge for equities, other than PEs, and that’s because margins are at an all-time record. We’re at the top of the valuation on any measures you look, except against interest rates. And at least for two or three months, I’ve been dead wrong.

So that was sort of the overwhelming macro view. Interestingly, some of the things that tend to happen early in a monetary tightening are responding to the QE shrinkage. And that’s obviously, as you’ve cited, emerging markets.

We talked about this obvious market mispricing in our latest MIR, The Kuhn Cycle (Revisited). The old narrative of low rates for longer had become extremely entrenched. And this narrative consensus has created a certain amount of data blindness, as is typical with popular and enduring narratives. This data blindness has led to a large mispricing of interest rates, particularly in developed markets.

Where things get interesting is all the corollaries that stem from a low rate narrative like this. Think of the billions of dollars that have poured into private equity over the last decade. The current PE model is predicated on the assumption of interest rates staying low, which is needed for their businesses’ long-term funding needs and justification for their sky-high valuations etc…

A really interesting section of the interview is when Druck talks about the diminishing signaling value in price action. He says:

The other thing that happened two or three months ago, mysteriously, my retail and staple shorts, that have just been fantastic relative to my tech longs, just have had this miraculous recovery. And I’ve also struggled mightily– and this is really concerning to me. It’s about the most trouble I’ve been about my future as a money manager maybe ever is what you mentioned– the canceling of price signals.

But it’s not just the central banks. If it was just the central banks, I could deal with that. But one of my strengths over the years was having deep respect for the markets and using the markets to predict the economy, and particularly using internal groups within the market to make predictions. And I think I was always open-minded enough and had enough humility that if those signals challenged my opinion, I went back to the drawing board and made sure things weren’t changing.

There are some great nuggets in here. I’ve long thought that one of the most important skill sets of a great trader — and something Druck has in spades — is to be extremely flexible mentally; never marrying oneself to a viewpoint or thesis and continuously testing hypotheses against the price action of the market.

Market Wizard Bruce Kovner said he owed much of his success to this, saying:

One of the jobs of a good trader is to imagine alternative scenarios. I try to form many different mental pictures of what the world should be like and wait for one of them to be confirmed. You keep trying them on one at a time. Inevitably, most of these pictures will turn out to be wrong — that is, only a few elements of the picture may prove correct. But then, all of a sudden, you will find that in one picture, nine out of ten elements click. That scenario then becomes your image of the world reality.

And Livermore noted the importance of flexibility when he wrote, “As I said before, a man does not have to marry one side of the market till death do them part.”

Now compare this to the “Fintwit experts” who have peddled a doom and gloom outlook for the last 7 years without ever taking a step back to maybe rejigger the models they use to view the world, which have been so consistently wrong.

Anyways, Druck then goes on to lay out the cause behind the diminishing power of price signals.

These algos have taken all the rhythm out of the market and have become extremely confusing to me. And when you take away price action versus news from someone who’s used price action news as their major disciplinary tool for 35 years, it’s tough, and it’s become very tough. I don’t know where this is all going. If it continues, I’m not going to return to 30% a year any time soon, not that I think I might not anyway, but one can always dream when the free money ends, we’ll go back to a normal macro trading environment.

The challenge for me is these groups that used to send me signals, it doesn’t mean anything anymore. I gave one example this year. So the pharmaceuticals, which you would think are the most predictable earning streams out there– so there shouldn’t be a lot of movement one way or the other– from January to May, they were massive underperformers. In the old days, I’d look at that relative strength and I’ll go, this group is a disaster. OK. Trump’s making some noises about drug price in the background.

But they clearly had chart patterns and relative patterns that suggest this group’s a real problem. They were the worst group of any I follow from January to May, and with no change in news and with no change in Trump’s narrative, and, if anything, an acceleration in the US economy, which should put them more toward the back of the bus than the front of the bus because they don’t need a strong economy.

They have now been about the best group from May until now. And I could give you 15 other examples. And that’s the kind of stuff that didn’t used to happen. And that’s the major challenge of the algos for me, not what you’re talking about.

Well, I’ll just, again, tell you why it’s so challenging for me. A lot of my style is you build a thesis, hopefully one that no one else has built; you sort of put some positions on; and then when the thesis starts to evolve, and people get on and you see the momentum start to change in your favor, then you really go for it. You pile into the trade. It’s what my former partner George Soros was so good at. We call it– if you follow baseball, it’s a slugging percentage, as opposed to batting average.

Well, a lot of these algos apparently are based on standard deviation models. So just when you would think you’re supposed to pile on and lift off, their models must tell them, because you’re three standard deviations from where you’re supposed to be, they come in with these massive programs that go against the beginning of the trend. And if you really believe in yourself, it’s an opportunity. But if you’re a guy that uses price signals and price action versus news, it makes you question your scenario.

So they all have many, many different schemes they use, and different factors that go in. And if there’s one thing I’ve learned, currencies probably being the most obvious, every 15 or 20 years, there is regime change. So currency is traded on current account until Reagan came in and then they traded on interest differentials. And about five years, 10 years ago, they started trading on risk-on, risk-off. And a lot of these algos are built on historical models. And I think a lot of their factors are inappropriate because they’re missing– they’re in an old regime as opposed to a new regime, and the world keeps changing. But they’re very disruptive if price action versus news is a big part of your process, like it is for me.

If you’ve been trading for any significant amount of time then you’ve certainly noticed the change in market action and tone due to the rise of algorithmic trading over the last decade. There’s often little rhyme or reason behind large inter-market moves anymore. Moves can simply happen because, as Druck said, algos that run on standard deviation models determine one sector has advanced too much relative to another, so the computers start buying one and sell another.

What we can do as traders now is to evolve and adapt. Work to understand what the popular models are that drive these algos so we can understand when they’re likely to buy and sell.

Also, I love his line about how he works to build a thesis and a position when he says:

A lot of my style is you build a thesis. Hopefully, one that no one else has built; you sort of put some positions on; and then when the thesis starts to evolve, and people get on and you see the momentum start to change in your favor, then you really go for it. You pile into the trade.

This a great lesson in trade management and how to build into a position using the market as a signal.

Druck also talked about Google (one of our largest positions) and reveals how he looks at some of the tech stocks that are popularly thought of as “overvalued” by the market.

I guess, let’s just take Google, OK, which is the new bad boy, and they’re really a bad boy because they didn’t show up at the hearing. They had an empty chair because they only wanted to send their lawyer.

But it’s 20 times earnings. It’s probably 15 times earnings after cash, but let’s just say it’s 20 times. Let’s forget all that other stuff. And they’re under earning in all these areas, and losing money they could turn it off. And then I look at Campbell’s Soup and this stuff selling at 20 times earnings.

And they’re the leaders in AI– unquestioned leaders in AI. There’s no one close. They look like they’re the leaders in driverless car. And then they just have this unbelievable search machine. And one gets emotional when they own stocks, when they keep hearing about how horrible they are for consumers.

I wish everyone that says that would have to use a Yahoo search engine. I’m 65, and I’m not too clever, and every once in a while, I hit the wrong button and my PC moves me into Yahoo. And Jerry Yang’s a close friend so I hate to say this, but these things are so bad.

And to hear the woman from Denmark say that the proof that Google is a monopoly and that iPhones don’t compete with Android is that everyone uses the Google search engine is just nonsense. You’re one click away from any other search engine.

I just I wish that woman would have to use a non-Google search engine for a year– just, OK, fine, you hate Google? Don’t use their product, because it’s a wonderful product. But clearly, they are monopolies. Clearly, there should be some regulation. But at 20 times earnings and a lot of bright prospects, I can’t make myself sell them yet.

Kiril then asks Druck about portfolio construction and how he builds positions, which was one of my favorite parts of the interview.

Kiril: When you worked with Soros for 12 years, one of the things that you said you learned was to focus on capital preservation and taking a really big bet, and that many money managers make all their money on two or three ideas and they have 40 stocks or 40 assets in their portfolio.

And it’s that concentration that has worked. Maybe you could go into that a bit more, how that works, how many of those concentrated bets did work, when you decided to get out if it didn’t work, do you add when the momentum goes up assuming the algos don’t interfere with it?

Druck: As the disclaimer, if you’re going to make a bet like that, it has to be in a very liquid market, even better if it’s a liquid market that trades 24 hours a day. So most of those bets, for me, invariably would end up being in the bond and currency markets because I could change my mind. But I’ve seen guys like Buffett and Carl Icahn do it in the equity markets. I’ve just never had the trust in my own analytical ability to go in an illiquid instrument, which in equity is if you’re going to bet that kind of size on– you just have to be right.

But to answer your question, I’ll get a thesis. And I don’t really– I like to buy not in the zero inning and maybe not in the first inning, but no later than the second inning. And I don’t really want to pile on in the third or fourth or fifth inning.

But even against the dollar, it’s not all-in right away. Normally, I’ll wait for– I’ll go in with, say, a third of a position and then wait for price confirmation. And when I get that, when I get a technical signal, I go.

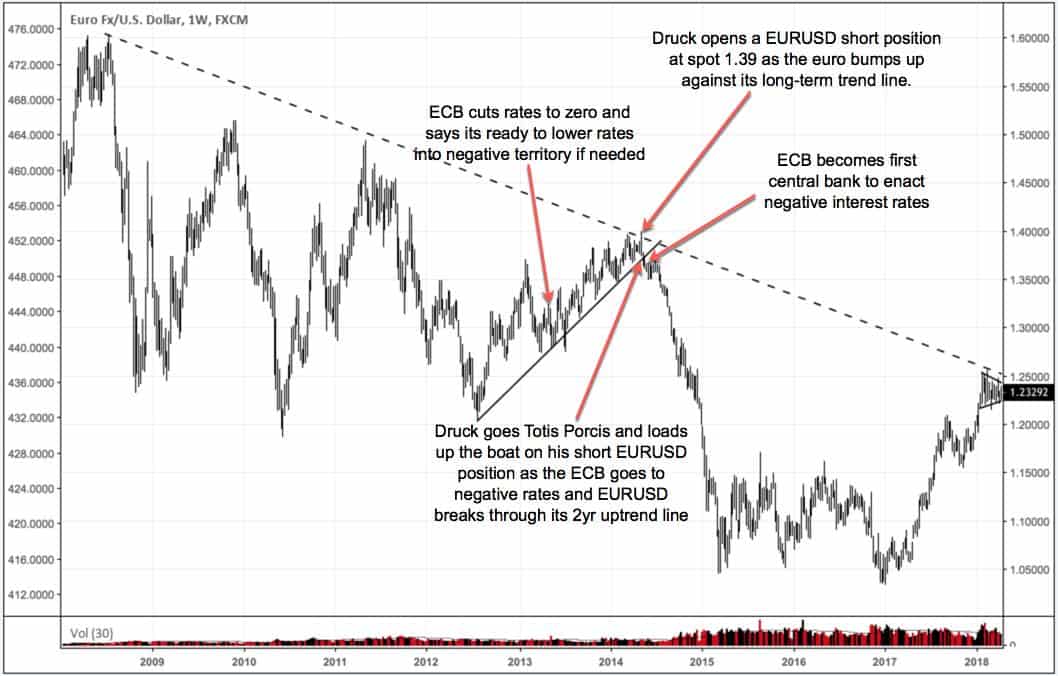

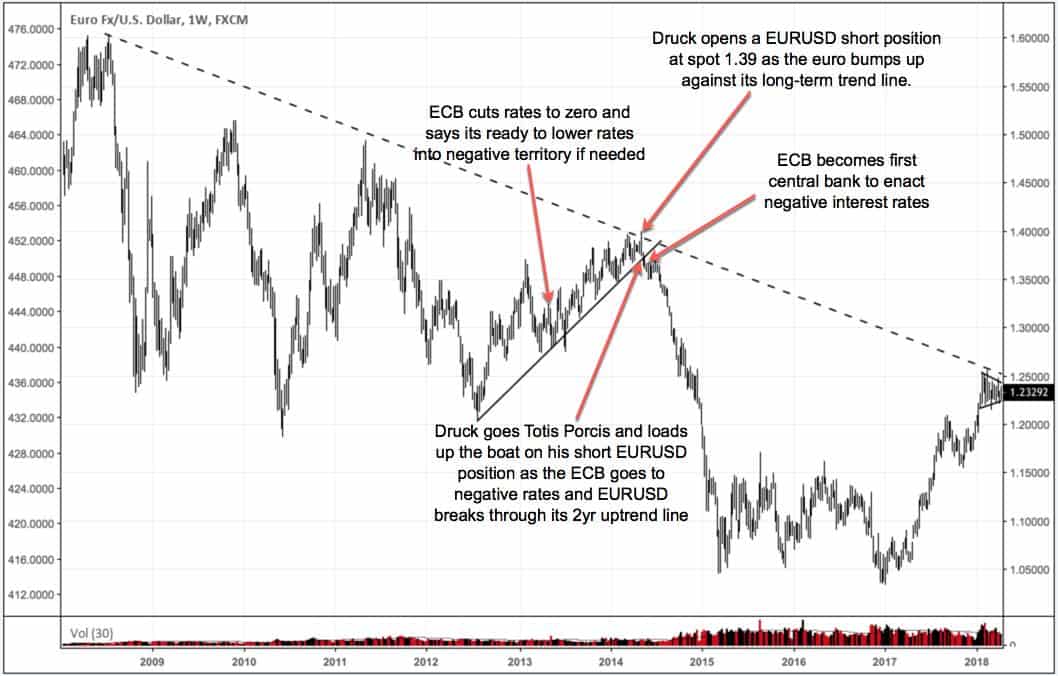

I had another very close experience with the success of the Deutschmark, which was the euro. I can’t remember– I think it was 2014 when the thing was at 140, and they went to negative interest rates. It was very clear they were going to trash that currency, and the whole world was long the euro. And it would go on for years. I’d like to say I did it all at 139, and I did a whole lot, but I got a lot more brave when it went through to 135. And that’s a more normal pattern for me.

We write a lot about the importance of concentrating your bets due to the natural power law distribution of returns (here’s a link).

This part of the interview was great because it shows how Druck uses a confluence of factors to leg into a trade. He says he develops a theory then waits for the market to begin to validate that theory and he puts a small (usually ⅓ position on). He then waits for further market confirmation that he’s correct (he calls this point the second inning) at which time he piles in and goes for the jugular.

The chart below illustrates perfectly his short EURUSD trade.

Here’s Druck talking about the 2000 tech bubble and what made him turn bearish.

Then there would be this strange case of 2000, which is kind of my favorite, and involves some kind of luck. I had quit Quantum, and Duquesne was down 15%. And I had given up on the year and I went away for four months, and I didn’t see a financial newspaper. I didn’t see anything.

So I come back, and to my astonishment, the NASDAQ has rallied back almost to the high, but some other things have happened– the price of oil is going up, the dollar is going way up, and interest rates were going up— since I was on my sabbatical. And I knew that, normally, this particular cocktail had always been negative for earnings in the US economy. So I then went about calling 50 of my clients– they stayed with me during my sabbatical– who are all small businessmen. I didn’t really have institutional clients. I had all these little businessmen. And every one of them said their business was terrible.

So I’m thinking, this is interesting. And the two-year is yielding 6.04, not that I would remember, and Fed funds were 6 and 1/2. So I start buying very large positions in two and five-year US treasuries. Then, I explained my thesis to Ed Hyman, and I thought that was the end of it. And three days later, he’s run regression analysis– with the dollar interest rates and oil, what happens to S&P earnings? And it spit out, a year later, S&P earnings should be down 25%, and the street had them up 18.

So I keep buying these treasuries, and Greenspan keeps giving these hawkish speeches, and they have a bias to tighten. And I’m almost getting angry. And every time, he gives a speech, I keep buying more and more and more. And that turned out to be one of the best bets I ever made. And again, there was no price movement, I just had such a fundamental belief. So sometimes it’s price, sometimes it’s just such a belief in the fundamentals.

Higher oil, higher dollar, and higher interest rates is likely to eventually lead to a negative earnings surprise for us as well; though that’s probably at least a few quarters if not further away.

Kiril then asks Druck about how he manages a drawdown. What he does emotionally and practically to stage a comeback.

Kiril: One of the great things I understand you do is when you’ve had a down year, normally a fund manager would want to get aggressive to win it back. And what you’ve told me you do, you take a lot of little bets that won’t hurt you until you get back to breakeven. It makes a tremendous amount of sense. Maybe you could just explore that a little bit with me.

Druck: Yeah, one of the lucky things was the way my industry prices is you price– at the end of the year, you take a percentage of whatever profit you made for that year. So at the end of the year, psychologically and financially, you reset to zero. Last year’s profits are yesterday’s news.

So I would always be a crazy person when I was down end of the year, but I know, because I like to gamble, that in Las Vegas, 90% of the people that go there lose. And the odds are only 33 to 32 against you in most of the big games, so how can 90% lose? It’s because they want to go home and brag that they won money. So when they’re winning and they’re hot, they’re very, very cautious. And when they’re cold and losing money, they’re betting big because they want to go home and tell their wife or their friends they made money, which is completely irrational.

And this is important, because I don’t think anyone has ever said it before. One of my most important jobs as a money manager was to understand whether I was hot or cold. Life goes in streaks. And like a hitter in baseball, sometimes a money manager is seeing the ball, and sometimes they’re not. And if you’re managing money, you must know whether you’re cold or hot. And in my opinion, when you’re cold, you should be trying for bunts. You shouldn’t be swinging for the fences. You’ve got to get back into a rhythm.

So that’s pretty much how I operated. If I was down, I had not earned the right to play big. And the little bets you’re talking about were simply on to tell me, had I re-established the rhythm and was I starting to make hits again? The example I gave you of the Treasury bet in 2000 is a total violation of that, which shows you how much conviction I had. So this dominates my thinking, but if a once-in-a-lifetime opportunity comes along, you can’t sit there and go, oh well, I have not earned the right.

Now, I will also say that was after a four-month break. My mind was fresh. My mind was clean. And I will go to my grave believing if I hadn’t taken that sabbatical, I would have never seen that in September, and I would have never made that bet. It’s because I had been freed up and I didn’t need to be hitting singles because I came back, and it was clear, and I was fresh, and so it was like the beginning of the season. So I wasn’t hitting bad yet. I had flushed that all out. But it is really, really important if you’re a money manager to know when you’re seeing the ball. It’s a huge function of success or failure. Huge.

This is perhaps the most important section of the interview. So much of being a great trader is learning to arbitrage time and I mean that in a number of different ways.

First, it means to analyze things on a longer timescale, to be able to pull back and look at the bigger picture, the broader trends, and not get hung up on a missed earnings or the latest news cycle. And secondly, it’s to have enough experience to be able to trust your process to the point that you know returns will eventually come to you if you just stick to your game. This form of time arbitrage means that you’re focusing on having a good return record over a 3, 5, and 10 year time period and you won’t go full-tilt if you’re down for a quarter.

Capital preservation always comes first and a strict adherence to a solid process produces good outcomes over the long pull.

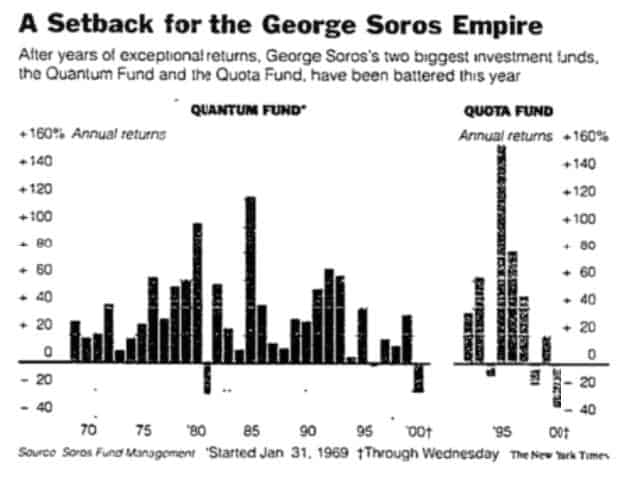

That’s it for my notes. I tried to include all the sections that I thought were worth sharing though I’m sure I missed some stuff. Watch the interview yourself if you can. Here’s a snapshot of Quantum Funds returns; Druck took over in 88’.