Alex here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

Recent Articles/Videos —

Trade Wars — AK reviews what the trade wars mean for US and Chinese stocks.

My Notes On Druck — I talk about my favorite parts from Stanley Druckenmiller’s recent interview on Real Vision.

Articles I’m reading —

Earnings season is picking up and quarterly hedge fund ‘Investor Letters’ are starting to hit my inbox. I have a large list of funds (here’s my old list, which I plan to update very soon), mostly value-oriented ones, that I make sure to read every quarter. It’s a great way to source ideas. Here are some links to what I’m reading along with excerpts.

Arkto Capitals Q3 2018 letter with an update on one its core holdings, RSSS, which he first covered in Q3 of last year (link here).

Research Solutions (RSSS) – Our 9% of portfolio holding, which we have increased as a position size from its original 2%, in the nanocap distributor of scientific publications and a provider of a unique science publication management software platform has continued to perform strongly returning 20% for the quarter and close to 140% over the last year. The company continues to gain traction with its Article Galaxy software, introducing an upgraded version in September, as well as rolling out various pricing plans and launching new sales channels which we expect to drive significant revenue growth for the product in the future. The Platform’s business segment, which includes Article Galaxy, grew revenues over 85% for the year with a $2.1mm revenue run rate. While revenues account for only 6.5% of the overall company, with 80% gross margins, the gross profit accounts for 20% of the company’s overall gross profits. We expect that in the next three years the platform’s business will continue to grow at almost triple-digit growth rates off a low base and for the company to begin to generate significant Free Cash Flow, at $5 to $10mm by 202, and $20mm to $30mm by 2023. With the current Enterprise Value at only $50mm, we believe this investment has many years of continued high returns ahead as the market begins to appreciate the true cash flow generating power and very sticky recurring revenues. The current illiquidity of the stock continues to be prohibitive for many institutional investors, however, the company has applied to be uplisted on the Nasdaq stock exchange from its current over-the-counter trading status, which should be a positive for the stock. We have been patiently adding to our position on a regular basis for the last year as our diversified partner base and an average capital commitment of four years allows us to be patient and forward-looking with this investment.

The talented value investor, Matt Sweeney of Laughing Water Capital, put out his Q3 letter (link here). He gives updates on a number of his holdings, as well as pitches some new additions to his portfolio. His letters are always worth reading in full. Here’s him giving his thoughts on pawn shop operator, EZPW, and you can find the full EZPW pitch deck here.

EZCorp, Inc (EZPW) — In addition to a likely acquisition in the near future, the company will be releasing a new 3 year plan in the coming weeks, and following significant shareholder agitation by us and other, much larger holders, it seems likely that the new plan will include an improvement in corporate governance – specifically tying executive compensation to per share metrics, rather than just company-wide metrics. Combined with a likely pending acquisition, a lapping of last year’s hurricane season, impressive operating metrics, cyclical weakness tied to record low unemployment, and a very attractive relative and absolute valuation, the bar for success for EZPW stock is very very low from where we are today.

In Horizon Kinetics’ Q3 letter, they talk about the “cognitive limitations in investing”, structural inflation, portfolio diversification vs. concentration, and then cover the bull case for some mid-sized defense contractors. Here’s the link and some words on CACI.

CACI is a defense electronics company that provides information technology (IT) and professional services predominantly to the U.S. federal government and federal agencies. Two-thirds of sales are from the Department of Defense, which includes the various Armed Forces and classified Dept. of Defense customers. Another quarter are from Federal Civilian customers such as the Dept. of Homeland Security and the Department of Justice. CACI focuses on data integrity and information, command and control, cybersecurity, surveillance and reconnaissance, and intelligence. The demand for its services is mostly created by the increasingly complex network, systems and information environment in which governments and businesses operate, and the need to stay current with emerging technology while increasing productivity.

…If one wanted to see how a company like this might fare during a cyclical downturn, then the Credit Crisis is a handy reference. Between 2006 and 2009, the revenues of the S&P 500 declined by 4.6% on a per share basis. CACI’s revenues rose by 59%. The S&P 500 earnings declined by 42% between 2006 and 2009. For CACI, the figure was up 8%. On a longer-term basis, the 12-year revenue growth for the S&P 500, from the pre-crisis year of 2006 through 2018, was 2.7% per year, while CACI revenues expanded by 10.0% per year on a per-share basis. S&P 500 earnings were up 1.6% per year, and CACI’s by 13% per year. For all of this, the shares trade at 17x the company’s free cash flow for the year ended June 2018. That is after deducting capital expenditures, and it is a trailing figure, and is still less than the stock market’s P/E ratio, much less the market’s free cash flow multiple.

Here’s Bill Miller’s take on markets in the latest Miller Value Fund Letter (link here).

So, to reiterate some things I have been noting in these letters for the past 10 years: It’s a bull market in stocks and it will continue until it ends, and no one knows when that will be. It will end when either the economy turns down and earnings decline, or when interest rates rise to a level where bond yields provide significant competition for stocks. I have seen some folks saying that will be at 3.5% or more on the 10-year, which I find implausible as bonds will still be trading at close to 30 times a return stream that does not grow, while stocks are at just under 17x next year’s earnings, and those earnings will likely advance about 5% or a bit more over the long term. During the bull market of the 1990s, bond yields averaged 6%. Today’s rates are still among the lowest in history, and only 2 years ago they WERE the lowest in history. Valuations of stocks do not appear demanding compared to returns available in other asset classes.

I agree.

And then finally, the latest issue of Graham & Doddsville is out (link here). There’s a number of investment write-ups along with a great interview with Scott Miller who manages Greenhaven Road Capital. Here’s a section where Scott talks about his process.

The research process depends on both the source of the idea and how close it is to something we’ve done in the past – effectively how much domain knowledge I have. In general, I’m trying to get comfortable with product, market, team, and execution risk.

I look for certain attributes to filter ideas quickly. For example, I prefer high insider ownership, asset-light business models (even though Fiat Chrysler – which we own – is not asset-light) recurring revenue, expanding margins, and the potential for operating leverage. The other piece is what Murray Stahl calls invisible companies – companies that don’t screen well, aren’t necessarily telling their story well, and aren’t covered by analysts. In those cases, the research process is initiated by other people explaining the idea to me. Then it becomes, “What are the pieces I have to fill in?”

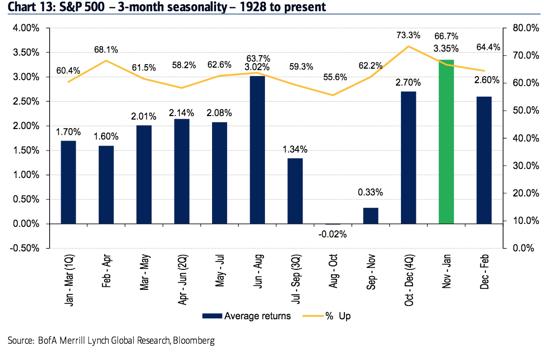

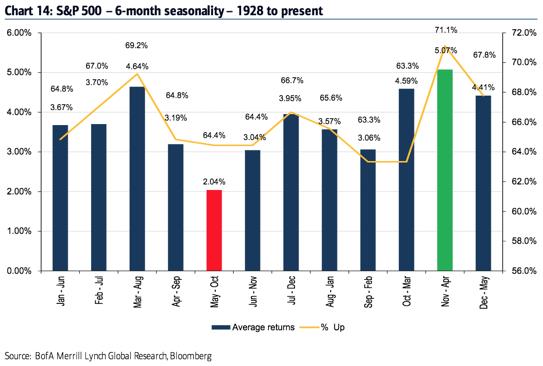

Chart I’m looking at —

The market is going through a large shakeout right now. It’s due to yields going up to fast along with slowing growth in the rest of the world beginning to hit US companies.

For what it’s worth, I’m of the opinion that this isn’t the start of a major bear market. In fact, I think this selloff will continue for another week, or two, or three… but then, eventually, it’ll rally hard into the end of the year — putting everybody on tilt.

This is my base case and I’ll be quick to flip my script if the data and price action suggest this is a cold take, but the odds of this playing out look pretty good to me. Just one of the many data points I’m looking at are the seasonal returns, and we’re about to head into the strongest 3 and 6-month return periods of the year (charts via BofAML).

Podcast I’m listening to —

Tim Ferriss’ latest podcast with Nick Kokonas is excellent and worth listening to for the full 3-hours. Nick got his start as a successful options trader on the floor of the CME back in the early 90s. He’s since then co-founded The Alinea Group of restaurants (which are considered some of the best restaurants in the world) along with a tech company called Tock, Inc. The guy is impressive…

I love how he looks at everything from a first principles perspective and questions the basic assumptions inherent to legacy systems (ie, how restaurant booking has been done for the last 50-years). It’s a fascinating listen and you’re guaranteed to learn something new. Here’s the link.

Trade I’m considering —

I’ve been bullish on the dollar (DXY) for a while now but I’m not yet buying this latest run. I think this is a false breakout and we’ll see the dollar reverse soon and trap a lot of bulls.

There’s a number of reasons for my suspicion behind this latest move. One being that positioning and consensus seem too crowded in the dollars favor right now. It’s not near the bullish consensus hit in early 17’ but still seems to easy for the dollar to make a sustained run here.

Second, I’m of the mind that EM stocks are likely to lead the US on the next major leg higher in US equities. Just look at how well EM high-yield debt has been holding up these last few weeks. And with that, we should see capital briefly flow out from the core and to the periphery which should drive down the dollar.

Then there’s Trump attacking the Fed, rising volatility in the US, and then also, definitely take a few minutes and read this great thread on the global plumbing system from Guy LeBas (link here).

I could be very wrong on this call — it wouldn’t be the first time — and I’ve hedged my ignorance with DOTM calls on the dollar but I covered my long naked position a number of weeks ago.

Quote I’m pondering —

I shared this on twitter recently but wanted to post it here in case some of you aren’t on the twitter train. It’s from Hunter S. Thompson.

Amen to that…

That’s it for this week’s Macro Musings.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. I post my mindless drivel there daily.