Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Latest Articles/Podcasts/Videos —

Your Monday Dirty Dozen [CHART PACK] — I look at some underlying technicals, discuss the equity/yield relationship, look at private investor flows, review the bullish action out of Mexico, and end with some charts on Japan.

Markets as a Banana: The MOST Important Fundamental Part 2: I lay out the second piece of the all-important global asset shortage puzzle and conclude with why the market is a banana.

Articles I’m reading —

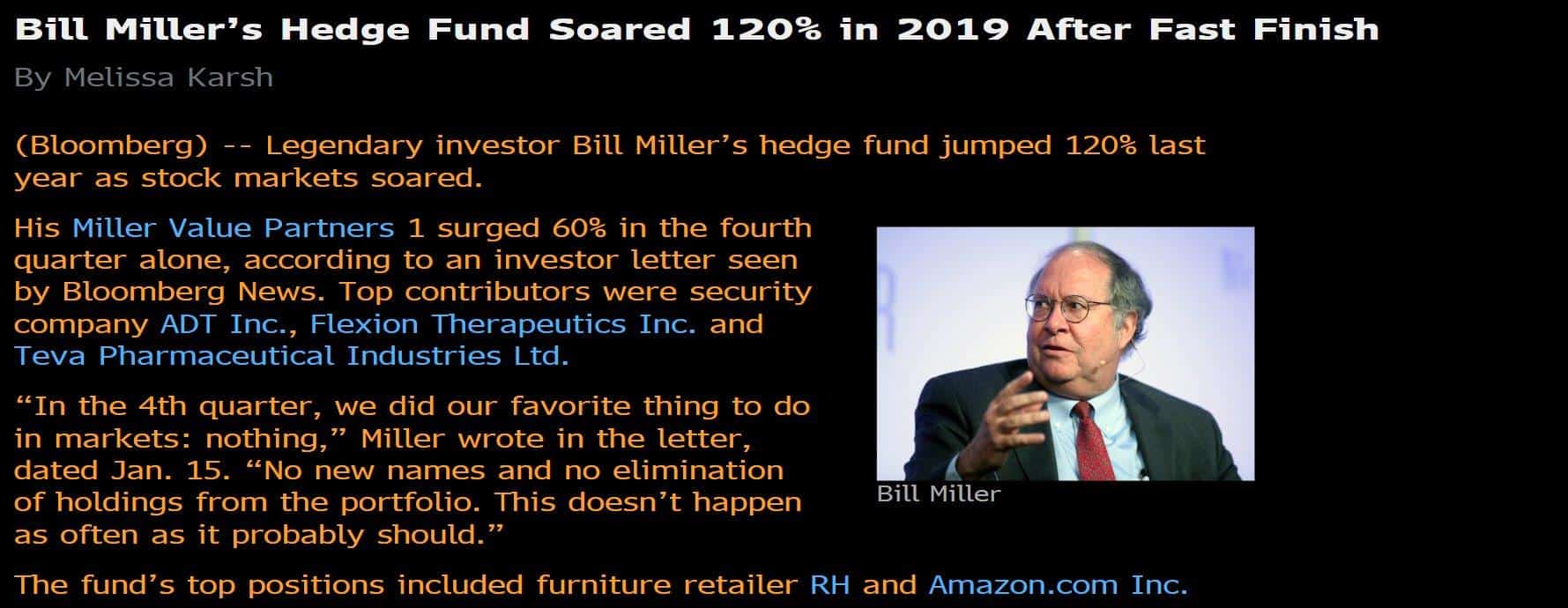

I love comeback stories. That’s why I was pumped to see this title scroll across the news feed on my terminal this week.

For those of you who aren’t familiar with Bill give this short piece by Jason Zweig a read (link here). Zweig details the fund managers meteoric rise along with his equally impressive fall, writing “In a business that thrived for decades by nurturing the cult of the star stock picker, no star had sparkled more brightly than Mr. Miller’s — or fell to earth with such a thud. Each year from 1991 through 2005, Mr. Miller’s fund outperformed the S&P 500 — a streak of 15 consecutive calendar years, unmatched by any other manager, even the great Peter Lynch…”

Bill’s fund lost over 50% in the financial crises which subsequently led to death-by-redemption where he was eventually forced to walk away from his firm, Legg Mason.

So nice to see you back in full swing Bill!

Following this news, I gave his most recent Investor Letter a read which you can find here. There’s some good stuff in it. I particularly like his take on general investor sentiment and the leftover trauma from the GFC that’s keeping most people from going full-throttle long like in cycles past. Here’s a couple of clips from the letter.

“As 2019 drew to a close, the mood was quite different with stocks posting record high after record high. Still, the so-called “chattering classes,” those who make their living talking or writing about stocks but not by actually owning or managing them, evinced little enthusiasm… I would characterize the mood as that favorite term of pundits, including those who actually do manage money: “cautiously optimistic.”… The forecaster always sounds more serious and smarter if he or she is cautious and expresses concerns about the risks that are always lurking about, especially when stocks are at an all-time high.”

And…

“Barron’s 2020 outlook issue a few weeks ago surveyed market strategists and typified the cautiously optimistic view: a “more muted” 2020, with stocks rising 4% on average. Add in a 2% dividend yield and the expectation was for a 6% return. That is about as cautious as can be since, after an above-average return in stocks one year, there is about an 80% probability they are higher the next year.”

Lastly…

“The shock and trauma of the 2008 financial crisis were so scarring that people have been and remain risk and volatility-phobic and see every negative event as presaging a serious correction or perhaps a recession and bear market.”

I agree on all points and have written as much over the last year. And that last line really gets at the heart of the matter, saying that investors “remain risk and volatility-phobic and see every negative event as presaging a serious correction or perhaps a recession and bear market.”

Last year it was yield curve inversion, then repo rates, and now I’m seeing the same “chattering masses” wail about coronavirus. Absolutely ridiculous…. Only Shiva knows what doom and gloom narrative the Zero Hedge crew will attach themselves to next. I just hope it’s a convincing one because my money is betting on that this market will rise until this bear cult begins losing followers en masse.

Charts I’m looking at—

Short-term indicators of sentiment and positioning are stretched. This is a known-known and it seems like everybody I follow on the twitters is talking about. It’s odds on we see a 5%+ selloff in the coming weeks but we need to wait for the tape to confirm the bears have control before we do much about it.

I’m not expecting too large of a pullback though. The reason? Financial conditions are as flush as can be… The St. Louis Financial Stress index just hit cycle lows, Kansas is low and trending lower, rates remain a tailwind, and the BAA/BBB is moving in the right direction.

Liquidity is loose.

Book I’m reading —

I’ve been reading Gerd Gigerenzer’s book “Gut Feelings” off and on for about the last month or so. I’ve actually been really enjoying it and would have finished it already — it’s a small book at a short 225pgs — but I’ve got a handful of others that I’m reading concurrently, so I’m making slow progress on all of them.

Gerd is a psychology researcher at the Max Planck Institute for Human Development. I first heard of him while listening to his, quite excellent, interview with Russ Roberts on the Econ Talk podcast (link here). Which is what convinced me to buy his book.

Gut Feelings is the counter-argument to the famous work done by Tversky and Kahneman into human bias — which has become so popular that seeing biases everywhere is becoming a bias itself!

Gerd convincingly takes the other side of the argument. Not to try and convince people that biases don’t exist but rather that human intuition can sometimes be extremely powerful and should not be dismissed outright. I’m about two-thirds of the way through it and have read enough to recommend to anybody interested in learning how and when one’s intuition can effectively be utilized.

Trade I’m looking at —

Just for kicks, I’m looking into Tutor Perini (TPC) after reading about it in Miller’s Deep Value Q3 letter (link here).

Here’s the section on TPC from the note.

“During the quarter, we increased our weighting in Tutor Perini (TPC) in our Deep Value Strategy as the stock price fell below $10 and initiated a position in our Concentrated Strategy. Tutor Perini is a leading global civil, building, and specialty construction company that provides general contracting and design-build services for some of the largest and most complex public/private projects. Tutor Perini share price has been recently under pressure due to a soft patch in business operations as older projects came to completion and new projects start dates were delayed.”

“In our opinion, near-term results are well-below normalized levels, as the company has had great success in winning new contracts, growing its backlog to nearly $11.5B versus their current $4.5B annual revenue run rate. Their civil segment has been the largest beneficiary of new contract wins with greater than $6B in back-log. As the civil segment carries the highest company margins, in excess of 10%, we believe this new business wins with supported normalized earnings in excess of $3/share over the next couple of years.”

“The company also anticipates the resolution of sizable outstanding receivables over the next couple of quarters. With a successful resolution on the outstanding receivables, Tutor Perini has the potential to generate more than $500M in free cash flow by 2021, allowing for significant debt reduction. At the end of the quarter, the company’s valuation multiples approached historical lows, EV/Revenue of .3x and 60% discount to book value. In our opinion, Tutor Perini’s share price looks significantly mispriced, providing a very attractive reward/risk opportunity.”

On the surface, this isn’t the kind of company I’d want to buy and plan to hold for the long-term. Its revenues and earnings have been stagnant for the last decade and that’s unlikely to change much. But… It’s bounced off the decade-long support level a number of other times and probably will this time too. In which case, it could be good for a quick mean reversion pop and run up gain.

Quote I’m pondering —

The securities we typically analyze are those that reflect the behavioral anomalies arising from largely emotional reactions to events. In the broadest sense, those securities reflect low expectations of future value creation, usually arising from either macroeconomic or microeconomic events or fears. Our research efforts are oriented toward determining whether a large gap exists between those low embedded expectations and the likely intrinsic value of the security. The ideal security is one that exhibits what Sir John Templeton referred to as “the point of maximum pessimism.” – Bill Miller

Are you seeing any “points of maximum pessimism” in this market?

Shoot me your thoughts, if so.

That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.