I will either find a way, or make one ~ Hannibal

SUBSCRIBE TO THE MONDAY DOZEN HERE

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at some underlying technicals, discuss the equity/yield relationship, look at private investor flows, review the bullish action out of Mexico, and end with some charts on Japan. Let’s dive in…

***click charts to enlarge***

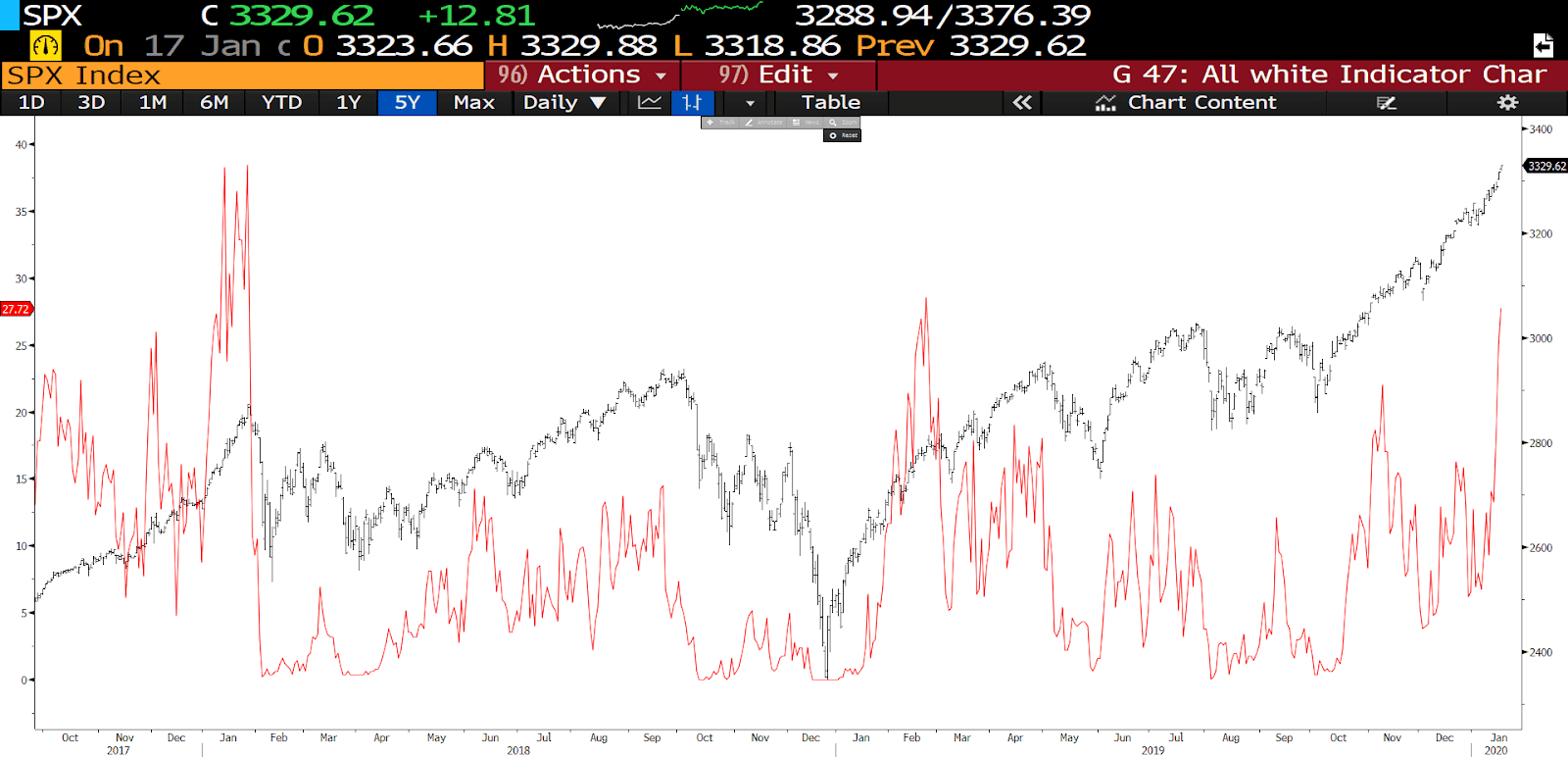

- The SPX remains in a buy climax. It is now trading above bull channels on multiple time-frames. This type of price action typically leads to some profit-taking in the follow-on weeks. The percent of SPX stocks trading above an RSI of 70 is now 37%, the third-highest reading in 3-years. The current bullish advance is stretched but buy climaxes tend to last longer than most expect.

- The strength of a bullish trend is determined by the participation in that trend. Last week we saw the highest percentage of stocks making new 52w highs since January 18′. Now, breadth like this is a tricky thing because over the long-term it’s a good sign of underlying strength. But extreme readings can also sometimes portend overdone conditions in the short-term which precede minor pullbacks.

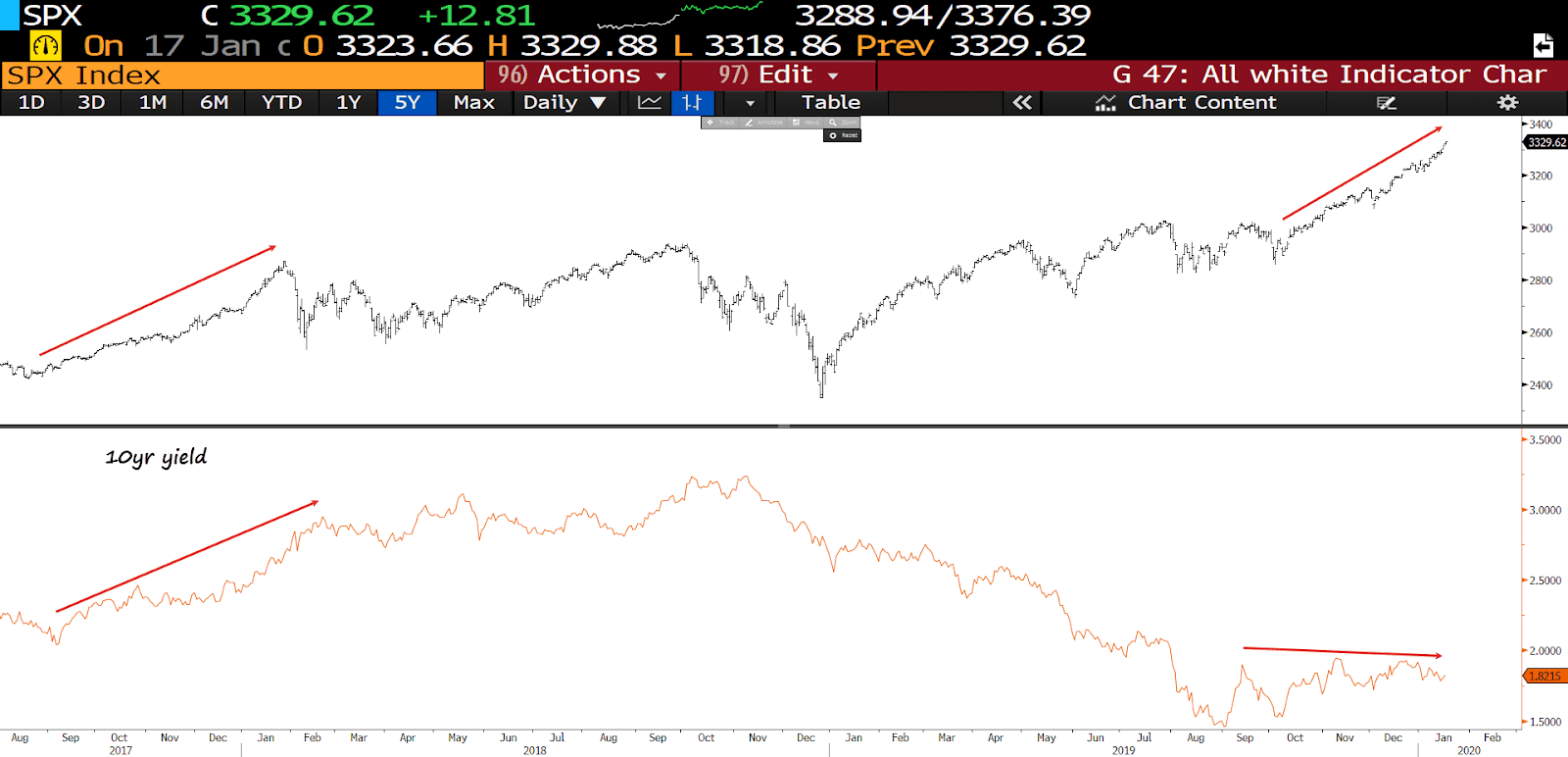

3. This is the most important chart to watch right now, in my opinion. It’s the SPX and the 10-year yield. Low yields have been an incredible tailwind for US equities, unlike in 2018 when yields rose hand-in-hand with the SPX. Bonds have been in a compressed regime (low vol). Compression leads to expansion (trends). I am directionally agnostic on which way yields will break but keep a close eye on them because where they go next will likely determine where the SPX, gold, and dollar all trade.

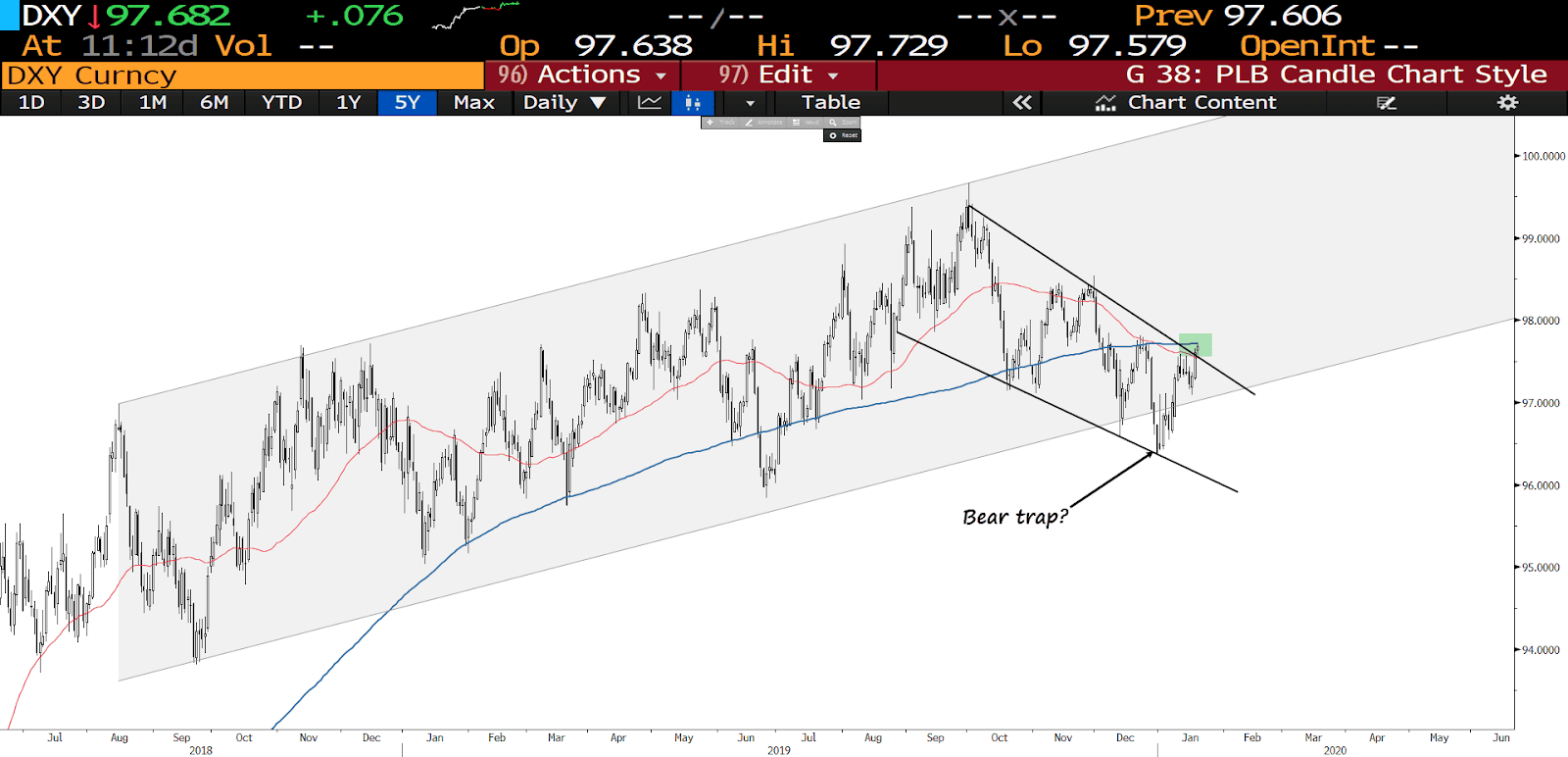

- Speaking of the dollar (DXY). It’s forming an interesting chart pattern. An argument can be made that the December breakout from its 2-year bull channel was a bear trap. If so, we’d expect higher prices from here.

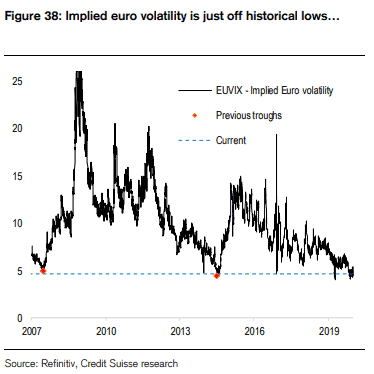

- Like bonds, I’m mostly agnostic on the direction of the dollar and major dollar pairs at the moment — except for a few idiosyncratic plays such as MXNUSD. But considering how compressed FX vol is, especially in the euro, there’s a real chance we see fireworks in the FX market this year.

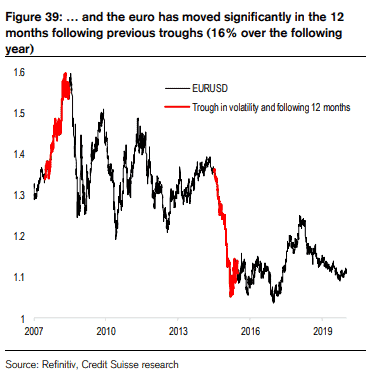

- This chart from Credit Suisse shows the follow-on moves in EURUSD after its 12-month volatility fell to similar levels.

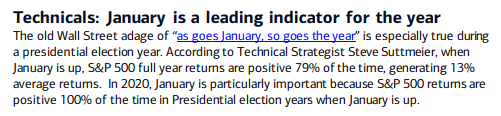

- The “January Effect” is a statistically significant phenomenon in the FX market. It’s a recurring pattern where EURUSD often makes its major high or low point for the year in the month of January. Peter Brandt has written a good overview of it here. This pattern also holds true for the equity market as BofAML explains below.

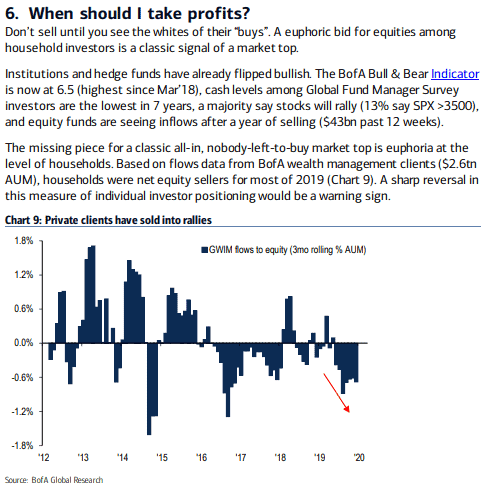

- In addition to the fact that yields have stayed pinned down during this equity rally, another significant difference between today and January 18′ is the lack of private investor / retail participation. You can see this in the data, such as BofA’s GWIM equity flows as well as TD Ameritrade’s IMX. This is important because major tops tend to occur only once retail has gone all-in.

- Mexico (EWW) continues to be one of my favorite long-term plays. The MSCI Mexico ETF broke out to new 52-week highs last week.

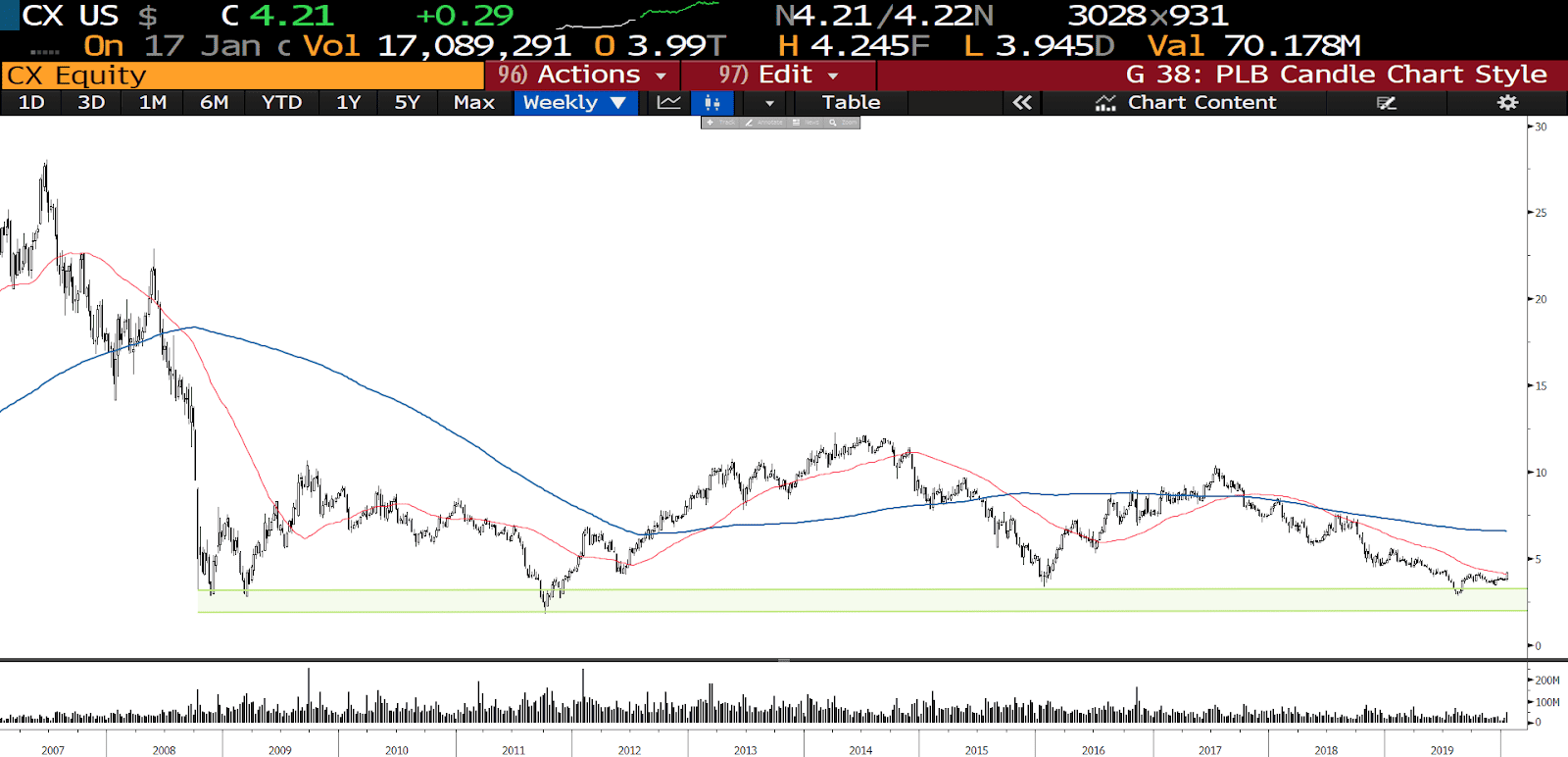

- There’s a lot of great looking charts there. This one of CEMEX (CX), a US-listed Mexican ADR, is a beaut. The stock is breaking out of a base at decade lows following a long multi-year downtrend and it’s trading on the cheap.

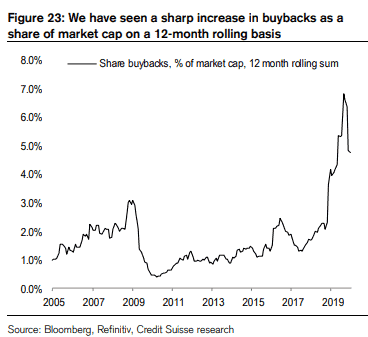

- Corporates have been a huge driver of this bull market with US companies buying back over a quarter of the entire market cap since 09′. This financial engineering is a big reason why the US market has outperformed the rest-of-the-world by so much. But now some other players are getting in on the buyback game. The chart below shows that Japan is stepping up its buybacks in a major way. I’m very bullish on Japanese equities for this very reason, as well as a few others (chart via Credit Suisse).

- And then, of course, we have the BoJ which is buying Japanese ETFs at a pace of nearly 1% of the total market cap a year (chart via Credit Suisse).

SUBSCRIBE TO THE MONDAY DOZEN HERE