We hope you and your family are safe and healthy during this COVID-19 season. Many states are opening up their economies, neighborhoods and beaches in the coming weeks. Stay healthy, remain cautious and keep your head on a swivel.

The markets etched higher since last week and the Russell 2000 broke out of a symmetrical triangle on the daily chart (see below):

There’s the argument that this is merely a bear market rally — and a face-ripping sell-off is around the corner. Continue to invest and trade with caution.

In times like these, it’s survival that matters.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Greenhaven Road Capital Q1 Letter

- Maran Capital Q1 Letter

- RF Capital Q1 Letter

Let’s get to it!

—

April 29, 2020

Perspectives & Opportunities: If you haven’t already, give Elliott Management’s Perspectives piece a read. It’s 14 pages of gold. Where does Elliott see the most opportunity right now? Credit. Here’s a snippet from the letter (emphasis mine):

“The potential opportunity set is primarily in credit. Of course,equities that have fallen 20%, 30%or50% in a very short time can provide substantial upside, but in periods like this one, we prefer the additional downside protection of carefully researched debt. The Holy Grail (which presented itself in size in 2008 )is to have credit positions in which we have so much confidence and which have so much convexity (asymmetric return profiles; much more upside than downside) that hedges are either not needed or can be relatively small.”

I’m itching to learn more about the credit space. If anyone has book recommendations on credit/bond investing, please email me or shoot me a Twitter DM.

__________________________________________________________________________

Investor Spotlight: Keep On Rolling With Q1 Letters

GIFs by tenor

GIFs by tenor

Greenhaven Road Capital: -32% Q1 2020

Scott Miller is one of my favorite investors, and yes, I get excited when he releases his quarterly letter. The reason is simple. Scott is a dynamic value investor. He doesn’t confine himself to the traditional value box. He’s not afraid to invest in companies that don’t screen well, nor garner much credibility with a Graham & Dodd disciple.

And his Q1 letter showed that.

Before diving into the names mentioned, I want to highlight this portion from Miller’s letter (emphasis mine):

“There is a greater focus on balance sheets because the duration of the pandemic and timing to recovery could be quite extended. Therefore, to own a company today, we have to believe they will very likely ride this out and make it to the other side. Sufficient company cash and liquid assets provide invaluable insurance.”

Alright, onto the names.

SharpSpring, Inc. (SHSP)

Miller’s Take: “SharpSpring sells software that enables marketing automation, primarily to digital marketing agencies for small and medium-sized businesses. Fortunately, SharpSpring does not have large exposure to travel, retail, or restaurants. However, if a business stops all marketing or ceases to operate, they will cancel their SharpSpring contract. Marketing budgets are some of the first to be cut during difficult times. On the more positive side, SharpSpring pricing compares very favorably to competitors, so they may be more likely to win new business for those seeking a high-quality, lower-cost marketing automation solution.”

What’s It Worth: “SHSP shares ended the quarter trading at an EV/Sales of less than 2. Absent a multi-year depression, the opportunity exists to see very substantial returns from here.”

SHSP is losing money on a GAAP basis. This makes sense though as they’re aggressively spending to grow their market and reach new customers. At some point, the profit nozzle should turn on. Until then, the company needs to finance operations externally — namely via share issuances.

The company issued $16M worth of shares last year.

Let’s take a look at the chart …

SHSP looks like it wants to break out above $7.20. You might get away with calling this an inverse head and shoulders as well. Regardless, it’s a bottoming pattern.

Digital Turbine (APPS)

Miller’s Take: “Digital Turbine serves as a neutral third party that works with wireless carriers to preinstall apps on new cell phones, then sells the slots to app-driven companies like Uber, Amazon, and Netflix. In the long term, Digital Turbine’s success will be driven by the number of Android phones it controls (carrier/manufacturer partnerships) and the revenue per device it receives.”

What It’s Worth: “APPS ended the quarter with a market capitalization of approximately $400M, which is less than 2X estimates for FY2021 revenue and 6X adjusted EBITDA. Thanks to the Mobile Posse acquisition (done without issuing shares) and gains in the core business, revenue will likely grow at a rate of 35% or higher.”

Sub-2x revenues for a company growing its top-line 35% doesn’t sound like a bad deal. But Miller notes a few issues with APPS path forward, such as:

-

- Recession extends upgrade cycles

- People locked in their houses are unlikely to activate new phones.

- Lower sales volumes

Here’s the chart …

PAR Technology (PAR)

Miller’s Take: “They own a defense contracting business, not impacted by Covid-19, which is worth approximately $100M and will likely be sold in the next year. The company also has a hardware business that sells $100M+ of equipment to large chains like McDonalds and Taco Bell, plus the Brink software business. Brink should end the year with 12,000 locations paying in excess of $2,000 per year”

What’s It Worth: “PAR may well see a share price significantly below $13, but in the long term, people will return to fast food restaurants for eat in, take out, drive thru, and delivery, and a share of PAR will no longer be available for the price of a couple of happy meals.”

The bet here appears to be that PAR’s Brink technology is vital to a QSR (quick-service-restaurant) daily operations. If these restaurants remain open (in any capacity), PAR gets paid. The shorter the shutdown lasts, the quicker PAR gets back on the growth path.

Delayed revenue, not lost revenue is the hope.

KKR & Co., Inc. (KKR)

Miller’s Take: “KKR is well positioned to benefit from the pandemic in the longer term. The firm has in excess of $160B of fee-paying capital that is “locked up” and will continue to pay fees through the slow down. KKR can also call an additional $60B of capital (dry powder) from LPs to further increase management fee income, and the pandemic will likely improve the returns for capital deployed during this period.”

What’s To Like:

-

- Strong balance sheet

- High insider ownership

- 40-year track record

- Investing mountains of capital at distressed prices

KKR’s Drivers of Growth:

-

- Balance sheet investments

- Management fees

- Incentive fees

- Capital market fees

Here’s the chart …

If we get a breakout above the horizontal boundary we could see prices retest the February highs.

Rope Out: Optiva, Inc. (OPT)

Miller’s Take: “Optiva is investing in building the next generation of cloud-hosted billing solutions for telecom companies. The cost savings for the telecom companies can be significant because they do not have to build data centers for maximum capacity as public cloud allows for dialing capacity up and down. Optiva estimates their customers will receive an 80% cost savings and a 10X improvement in performance.”

What’s It Worth: “In the last 12 months, they generated USD $14.5M in EBITDA while investing USD $11M in their cloud product, implying a valuation of a little more than 1X revenue, 9X EBITDA or 5X EBITDA ex cloud investment.”

OPT is a highly illiquid business. Miller notes that shares often go hours without exchanging hands — even post-earnings announcements. Alex and I worked on this name a couple years ago. It’s about time to dust off the old research deck and look with fresh eyes.

Here’s the chart …

Miller’s New Basket: Roku, Pinterest & Carvana

Here’s why I love Miller’s investment style. He added Roku (ROKU), Pinterest (PINS) and Carvana (CVNA) to his portfolio. These are not traditional value investments. But that’s the beauty of value investing. It’s not low P/E or low P/B. It’s buying something today whose cash flows are worth more in the future discounted back at an appropriate rate.

_________________

Maran Capital: -17.50% Q1 2020

Dan Roller is the portfolio manager of Maran Capital. He’s wicked smart and remains (brutally) underfollowed on Twitter. The fund returned -17.50% during Q1. Dan starts the letter by reminding readers what really matters (emphasis mine):

“I am sticking to our fundamental guiding principles: margin of safety, conservative underwriting, alignment of interests, a long time horizon, and investment as ownership in a piece of a business.”

This is a value investor’s “true north”. Stick to those above principles and you should do okay.

Roller mentions three of his top-five portfolio companies:

-

- Clarus Corporation (CLAR)

- Scott’s Liquid Gold (SLGD)

- Standard Diversified (SDI)

Let’s take a look.

Clarus Corporation (CLAR)

Business Description: Clarus Corporation focuses on the outdoor and consumer industries in the United States, Canada, Europe, the Middle East, Asia, Australia, New Zealand, Africa, and South America. The company develops, manufactures, and distributes outdoor equipment and lifestyle products focusing on the climb, ski, mountain, sport, and skincare markets. – TIKR.com

What’s To Like:

-

- Growing top-line revenue 10%+ on average last three years

- P/E shrunk from 164x to 15x in three years on increased earnings

- Cash from operations grew from $3.7M in 2015 to $9.5M in 2019

- Market cap only $60M higher than 2015 despite massive earnings growth

What’s Not To Like:

-

- It’s a retailer

- Increased debt while reducing cash (Quick ratio from 5x in 2015 to 1.8x in 2019)

- Increase in Average Cash Conversion Cycle (173x in 2015 vs. 198x in 2019)

- Isn’t crazy cheap

Here’s the chart …

That’s a beautiful breakout from a tight consolidation range. If the stock holds the breakout price it would signal a close above the 50MA, another bullish indicator.

Scott’s Liquid Gold (SLGD)

Business Description: Scott’s Liquid Gold-Inc. and its subsidiaries develop, market, and sell household and personal care products in the United States and internationally. The company operates in two segments, Household Products and Personal Care Products. – TIKR.com

What’s To Like:

-

- High insider ownership (CEO owns 24% of the company)

- Trading at 0.53x EV/Sales

- Zero long-term debt and $24M in Net Asset Value ($20M market cap)

- Highly illiquid

What’s Not To Like:

-

- Consistent revenue and margin decline

- Negative cash flow from operations over last two years

- Increase in Average Cash Conversion Cycle from 75 in 2015 to 161 in 2019

- Increase in Days Sales Outstanding from 12.85 in 2015 to 36.83 in 2019

SLGD’s negative cash from operations looks bad at first glance. Looking deeper, it appears transitory. The company increased inventory each of the last two years, potentially in anticipation of higher product sales. Interested investors should watch that closely.

Here’s the weekly chart …

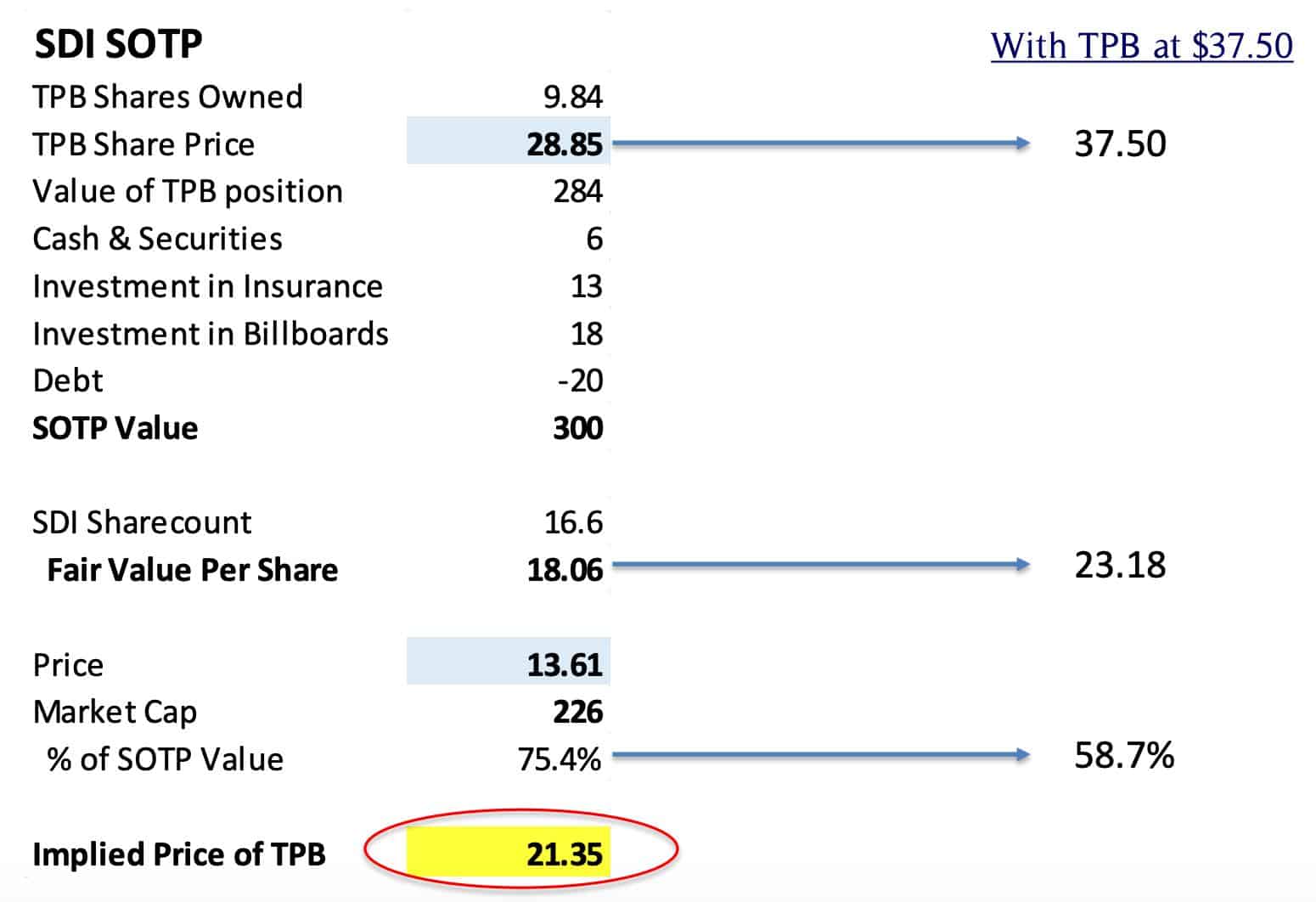

Standard Diversified (SDI)

Business Description: Standard Diversified Inc., a diversified holding company, through its subsidiaries, engages in the other tobacco products and outdoor advertising activities in the United States. Its Smokeless Products segment manufactures and markets moist snuff and contracts for and markets chewing tobacco products. – TIKR.com

What’s To Like:

-

- Holding company whose primary asset is Turning Points Brand (TPB)

- Insiders own 90% of the company

- Compound mis-pricing

- Smart and talented management

- Consistent cash-flow from operations

What’s Not To Like:

-

- Increase debt burden by $100M (from $202M – $334M)

- Bet on tobacco industry staying solvent

- Recent decline in revenues, margins and earnings

What’s It Worth:

Here’s a screenshot from Dan’s 2018 presentation on TPB and SDI outlining the value proposition:

For what it’s worth, SDI still trades around $13/share today. TPB, however, trades near $24/share.

_________________

RF Capital: -27.13% Q1 2020

Roger Fan runs RF Capital. I’ll leave it to you to figure out the inspiration behind the Fund’s naming. Roger returned -27.13% during Q1. Here’s his Q1 letter.

Roger disclosed his top holdings as of the end of Q1:

-

- GrafTech International (EAF)

- Aimia, Inc, (AIM.TO)

- Foot Locker (FL)

Let’s break down Roger’s views on each position.

GrafTech International (EAF)

Roger’s Take: “[W]e believe Graftech is well-positioned to handle this difficult environment. Not only is Graftech the only company in the industry that employs LTAs, but they also produce ~70% of the required needle coke through Seadrift, their subsidiary. Graftech’s competitors have to buy all of their needle coke on the spot market, thus creating greater variability in input costs. Given its vertical integration with needle coke, Graftech provides more earnings visibility and stability than its competitors.”

What’s To Like:

-

- Long-term take-or-pay contracts

- Vertical integration with needle coke supply

- Locked in contracts at high spot and market prices

- Clear path towards substantial cash flow generation

What’s Not To Like:

-

- Commodity-dependent company

- Performance linked to steel industry

- Renegotiation (or default) of long-term contracts with customers

Here’s the chart …

Aimia, Inc, (AIM.TO)

Business Description: Aimia Inc., together with its subsidiaries, engages in loyalty solution business in Canada, the United Kingdom, the United Arab Emirates, the United States, Australia, and others. – TIKR.com

Roger’s Take: “Although the cash burn continues, management expects positive adjusted EBITDA and breakeven FCF in 2020. If the company achieves those targets, it would certainly help move the stock price. However, the value in Aimia continues to be its cash and assets. The company still trades at a large discount to NAV.”

What’s To Like:

-

- Crazy cheap based on NAV and net cash

- Decent business providing a needed service to airlines and customers

- Positive changes on the board

What’s Not To Like:

-

- Cash burn creates melting ice cube

- Long-standing distrust in management’s ability to unlock value

AIM is basically a box of cash with the potential to have a decent, cash-flowing operating business attached. Shareholders of AIM don’t need the company to generate a ton of free cash to win. They can simply see their shares trade on par with net cash in the bank.

Here’s the chart …

Foot Locker, Inc. (FL)

Business Description: “Foot Locker, Inc., through its subsidiaries, operates as an athletic shoes and apparel retailer. The company operates in two segments, North America and International.” – TIKR.com

Roger’s Take: “Fortunately for the company, they have a strong balance sheet and are in a better position than most other retailers to weather the storm. The company ended 2019 with $907 million in cash versus $122 million of debt on the balance sheet. When stores reopen for business, the share price is likely to recover.”

FL churns out roughly $480M in annual free cash flow. The company sports a strong balance sheet and generates enough EBIT to cover interest expense 71x over.

FL’s also reduced its Average Cash Conversion cycle from 87 days to 75 days — almost two full weeks of improved cash conversion.

Here’s the chart …

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!