Today’s note is the second part of a write-up I sent you earlier in the week titled “The MOST Important Fundamental: The Global Shortage of Safe Assets”. If you haven’t already, I suggest clicking the above link and giving the first section a read before diving into this one.

In the following collection of ordered words and well-timed punctuation marks, we’re going to lay out the second piece of the all-important global asset shortage puzzle.

By the end, you’ll know why the market is a banana (yes, you read that right, I said banana). And we’ll finish with what this means for the market on both a longer-term as well as a near-term basis.

Enough with the introduction… Let’s hop right in.

Everything in markets comes down to supply and demand. Our job as speculators is to figure out the two and see if there’s a mismatch that will lead to a change in prices (a trend). So let’s start by defining demand.

Investors can allocate their savings to three main assets: stocks, bonds, and cash. They make these allocation decisions based on desired returns and tolerance for risk to come up with a portfolio mix — the classic being 60% in stocks and 40% in bonds/cash. Recent price appreciation (not valuation or yield) and general risk appetites are the overwhelming drivers behind this allocation decision. Momentum is the bottom line. Investors are always chasing the trend — nobody likes sitting out of a rising market.

Savings — the amount of money available to invest — fluctuates according to the levels of cash + credit (money) in the system. Since credit is easier to create than cash (any two willing parties can create credit out of thin air with an IOU), credit largely drives the amount of investable money in the system.

Expanding credit equates to more savings to invest. This amount cycles up and down in accordance with our debt cycle framework.

The supply side of financial assets is comprised not just of the total amount of shares or bonds in existence, which is what many people mistakenly believe. But rather, it’s the aggregate market value — the total dollar amount in existence at current market prices — that makes up supply.

The equity market has a flexible supply. If demand for stocks goes up then equity flows will drive up prices, increasing the total market cap thus creating more supply to equilibrate to demand. It’s a self-correcting system.

The basics of our equity supply and demand model is thus:

-

- On the demand side we have:

- The amount of savings available to invest is driven by the credit cycle

- The allocation mix of investor portfolios is driven by performance chasing and general risk appetite (both work on each other in a reflexive loop)

- On the supply side we have:

- Supply consists of the total market cap of the asset and this market cap is equal to the number of shares + the price at which they trade

- Stocks have a flexible supply in that greater demand leads to a higher market cap and more supply

- On the demand side we have:

We can look back through time and see how this model correlates to market returns.

Historically, US corporate share issuance has rarely exceeded 2%. Over the last three and a half decades corporates have been reducing their share count through buybacks and M&A at an average annual rate of 2%.

While the number of shares available to trade has been steadily falling, the amount of money (cash+credit), has been steadily increasing.

Over the last 50 years, the money stock in the US has gone up at an average annual rate of 8% a year.

So…… over the last five decades, the supply of equity (available shares) has been dropping at an average rate of 1-2% a year while the total money stock has gone up at an average rate of 8% a year.

Let’s disregard the total market value and investor allocation preferences for a second. Just taking this straightforward mismatch of supply and demand alone, we get a structural supply deficit of approximately 9.5% a year.

You want to guess what the average annual return of the stock market has been over this same period?

Banana…

No, sorry, I misspoke… the banana part comes later. The correct answer is 9.5%… 9.5% is the average annual return of the S&P 500 over the last 50 years. And it’s also the average yearly deficit of equity supply in our stock market supply and demand model.

Coincidence you may ask?

Not at all. It’s just math.

If investors keep their portfolio mix (their allocation preference between stocks, bonds, and cash) relatively constant, then the market value of stocks has to rise at the same level of the supply and demand mismatch caused by share reduction and money creation — 9.5% a year.

Eye-opening stuff, isn’t it?

I hope this changes the way you view the broader market cycle. The GOAT, Stanley Druckenmiller, instinctively figured this out, even if he gets the actual mechanisms at work wrong. But it’s this phenomenon he’s referencing when he says things like:

Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.

So to sum this section up… overtime, the market has to rise because we operate in an inflationary system. A system where the quantity of money is always going up (over the long haul), and the corporate sector’s aversion to dilution keeps share growth at a minimum to a net negative.

The only way for the market to clear, for supply and demand to balance, is for the total market value to rise, increasing supply to meet demand.

If you were trading back in the early 80s and you understood this market supply and demand model, you would have known with absolute certainty that a massive secular bull was on the horizon. It was mathematically inevitable by that point… the supply/demand mismatch combined with the then-record low allocations to equity made for an unavoidable rally in stocks. And a massive rally at that, which is exactly what ended up happening.

This macro model has been a major reason behind my continued bullishness and definitely was when I first wrote the above report on the topic for members of our Collective back in mid-18’.

If you’d like to read up more on this idea, then I highly recommend checking out this 2013 blog post on Philosophical Economics, which outlines, in much greater detail, this very idea.

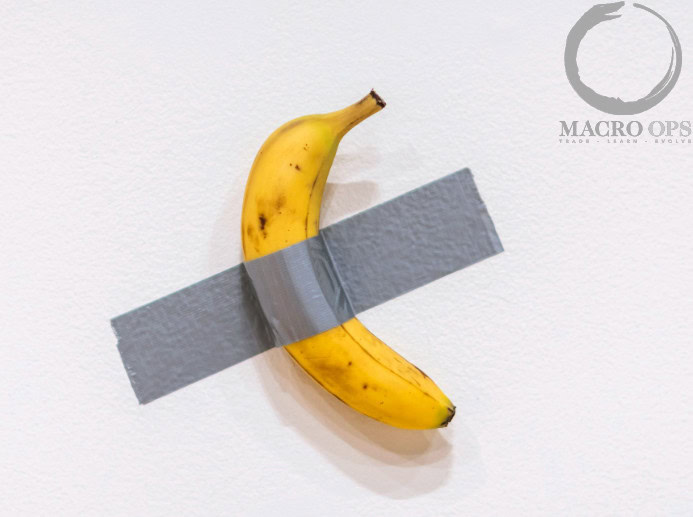

And finally, we can get to my original point, which is that the market is a banana.

Not just any banana. But this very specific banana.

Last month, some guy — who apparently refers to himself as an “artist” — duct-taped this ripening fruit to a wall at Art Basel Miami. This piece of “art” was then sold three consecutive times: first for $120,000, and finally for $150,000.

I know what you’re thinking… what a steal, right?

Old Warren would surely be proud of that final buyer — who most definitely resides in Graham-and-Doddsville.

Anywho… the banana art was shortly eaten thereafter by some other guy who also calls himself an “artist,” and said the act of eating the artful banana was actually art itself.

When I first heard this, I thought: “My God, that poor banana buyer must be devastated.”

Fortunately, I was mistaken.

I confess… I’m a total ignoramus when it comes to the highfalutin world of Produce Art.

In fact, according to the Gray Lady, the performance artist’s “stunt did not actually destroy the artwork or whatever monetary value it might have had at that moment.”

The three buyers who collectively spent about $390,000 on the taped fruit had bought the concept of the piece, which comes with a certificate of authenticity from the artist, along with installation instructions. It is up to the owners to secure their own materials from hardware and grocery stores, and to replace the banana, if they wish, whenever it rots. After Mr. Datuna consumed the banana, the gallery taped another one to the wall.

That makes perfect sense.

Glad The Times could clear that up for us.

Well, anyway, I believe I have proven my point: The market is a banana… or rather, a banana duct-taped to a wall.

What’s that? You’re not fully convinced?

Okay, let me explain this a bit more.

What I’m trying to say is that the same forces which drive the valuation of “banana stuck to wall” are the exact same ones that drive the valuation of the stock market.

“Banana on wall as a concept” sold for $150,000.

I’m not certain, but I think that’s on the higher end of valuations for a ripe banana.

It received this high valuation because there’s a low supply of concept banana art — yet tons of demand for stupid… I’m sorry… unique works of art.

Low supply. High demand. High price.

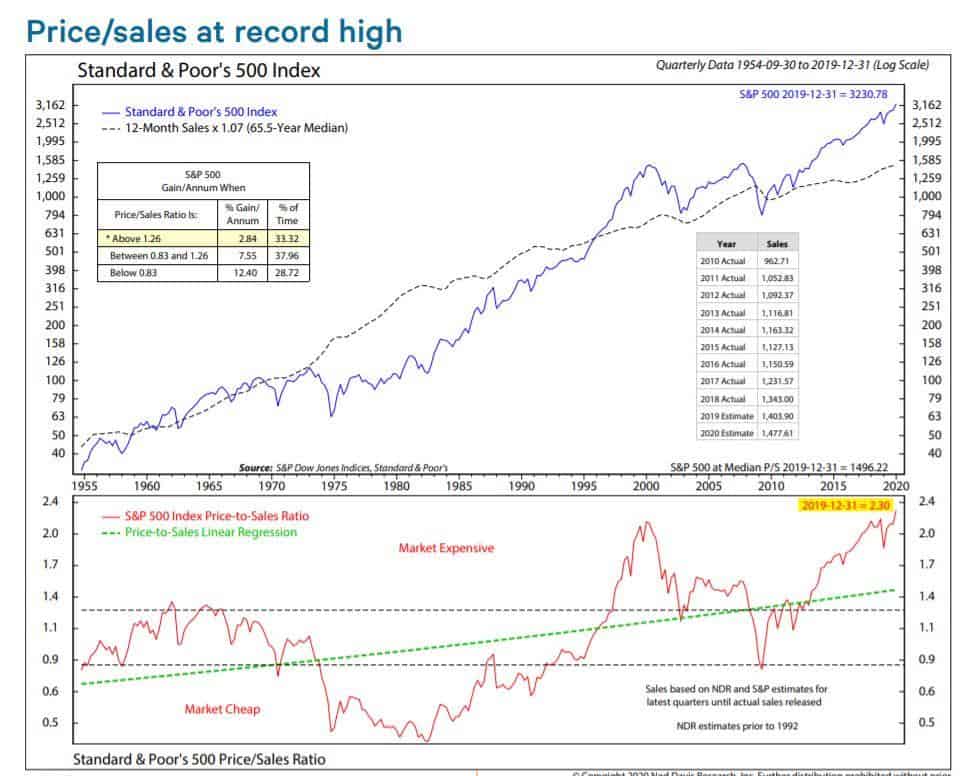

The stock market is trading at a record price-to-sales (chart via NDR).

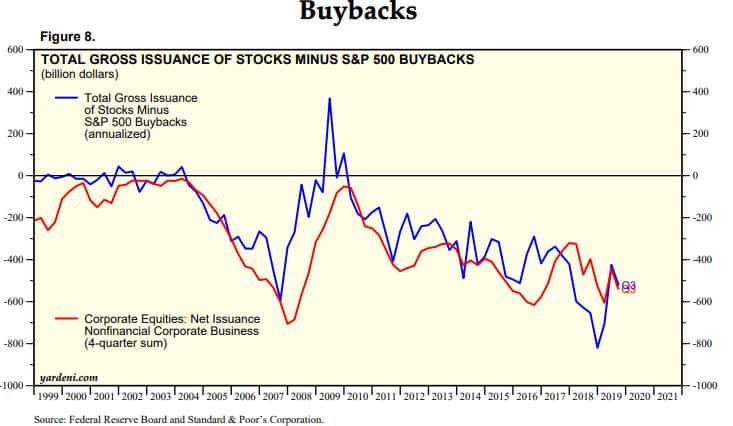

It’s trading at record valuations because like banana-as-a-concept, there’s lots of money that needs to be invested and the supply of stocks keeps falling. This chart of gross share issuance (new issues minus buybacks) shows how large the supply deficit is — and this isn’t even counting M&A which is running hot as well (Chart via Yardeni).

This is why market valuations are such a useless variable — at least in the intermediate term — when it comes to gauging the sustainability of a market trend.

Valuations can always go much higher or much lower than you think.

Because, as we discussed, multiples have nothing to do with the durability of the cycle.

Like the pricey banana, it has everything to do with your basic supply and demand — the very model I’ve laid out in these pages and in my earlier write-up.

So where does this model of supply and demand leave us today?

Well:

- With rates pinned low due to a global shortage of safe assets

- And buybacks set to continue unabated as financial conditions remain easy

We get… well, banana on wall selling for $150k —

That is, stupidly high prices for stocks.

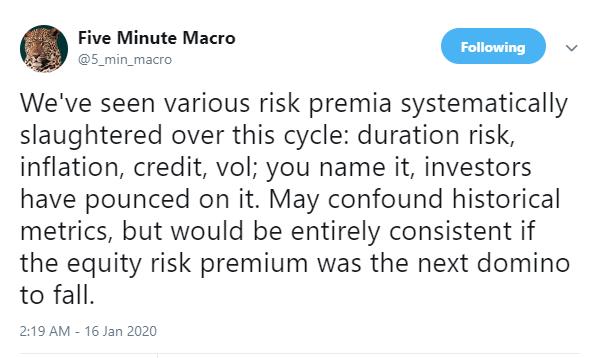

I think Five Minute Macro nailed the current zeitgeist in a recent tweet, writing:

There’s still plenty of risk premia spread to tighten should things get “fruit art as a concept” silly… which I very much believe they will.

I’m seeing a lot of opportunities in this market — on both the long and short side.

Next week, I’ll be putting out a report for Collective members, where I’ll share a handful of incredibly asymmetric plays I’ve uncovered in the small-cap space.

I expect small-caps to outperform their larger siblings by a wide margin this year.

There are two stocks in particular that I honestly believe have 10-bagger+ potential. I can’t wait to share them and am really looking forward to getting the report out to the group.

If you’d be interested in receiving this report — along with all our research and the many other benefits of being part of the Collective — go ahead and sign up for our risk-free trial by clicking the link below.

Enrollment closes this Sunday and won’t open again until next quarter, when prices will be 47% higher.

Hope to see you in there.