Let’s talk about this tweet from the very astute Mark Dow.

Asset shortages are something I’ve been writing about for the past 3-years now (Collective members can find a report I put together on it back in early 2018 titled “A Persistent Bid”).

They’ve been the primary driver of this bull market, which is now the longest in history. And they’re going to keep driving this market much higher — likely until the perma-bears have ripped the last strands of their hair out.

That’s why it’s important to understand the dynamics behind what I refer to as “the real fundamentals of the market”. It’s a key concept that very few pay attention to let alone understand.

There are two components to this asset shortage bit (1) which has to do with “safe assets” such as developed market government bonds and (2) other financial assets such as equity and credit. In today’s post, we’re going to talk about the former and in a future post, we’ll cover the latter.

So what does a shortage of safe assets mean?

Well, in its most basic sense it refers to an imbalance between supply and demand. Supply and demand are, after all, what drives the market over the long-term.

And a “safe asset shortage” just means that there is more demand for safe assets (ie, government bonds) than there is a supply of them.

Here’s why that is and what it means for both safe and risk assets going forward.

Classic economic theory states that capital should flow from rich countries to poor countries. But, like much of economic theory, this isn’t how things actually work.

What we mostly see is the reverse. Capital flowing from less well off countries into richer one — the US being a primary recipient of these flows.

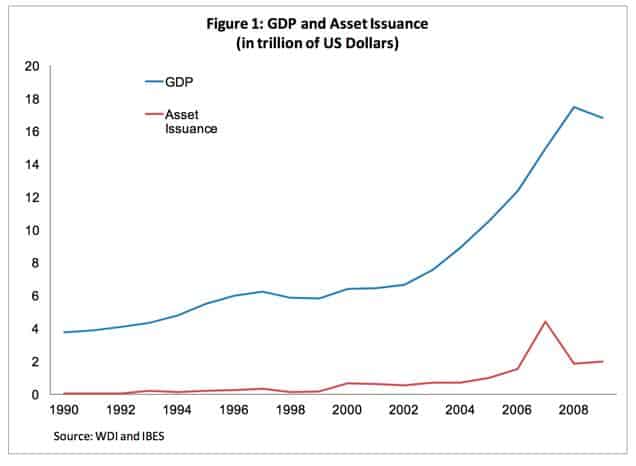

The IMF noted why this is in a recent paper writing that an “economy’s ability to produce output is only imperfectly linked to its ability to generate financial assets.” This means that most countries grow faster than they financially deepen (ie, increase their ability to absorb that growing wealth/money).

The chart below illustrates the point.

As emerging markets increase in size, their domestic financial markets lag behind — their financial assets grow at roughly half the rate of GDP. With a limited domestic pool of securities, EM savers end up having to invest the majority of their wealth abroad.

From that same report, the IMF writes that “improved macroeconomic fundamentals have raised the demand for financial assets. Rising income per capita in EMs, pension reforms in Latin America, increasing commodity prices in the Middle East and Africa, and limited consumption growth in East Asia have contributed to an increasing supply of domestic savings in EMs that needs to be invested.”

Let me translate. As emerging markets mature, their ability to generate credit and grow their money stock rises exponentially. Since EM financial markets can’t soak up this ballooning money stock, it means that an increasing amount of it has to flow to the US; which has the deepest financial markets in the world.

This raises the demand for US assets.

Here’s what a current real-world example of this looks like.

A few months ago, the Financial Times published an article this week titled “Why Taiwan poses a threat to the US bond market”. Here’s a few excerpts from the piece with emphasis by me:

Taiwan may be small, but the island has emerged as a financial superpower thanks to the thriftiness of local savers and an eye-watering current account surplus of about 15 percent of gross domestic product. The country now has the second-largest financial system in the world, relative to gross domestic product. And its life insurance industry is the biggest, with assets-to-GDP of 145 per cent, according to JPMorgan.

The local economy is not big enough to accommodate these enormous sums, so Taiwanese financial institutions have funneled a whopping $1.2tn abroad. Other countries have large overseas stashes of money, but largely in the form of central bank reserves or sovereign wealth funds. Taiwan is anomalous both in terms of the size relative to its economy, and that this pool of money consists of private, rather than public savings.

The money has been invested conservatively, largely in US government and corporate bonds with high credit ratings.

Apparently, Taiwanese insurers hold over 14% of US corporate debt… That. is. absolutely. insane. Not to mention, a large portion of these holdings are unhedged — meaning, their insurers are taking on large amounts of FX risk. Brad Sester, from the Council of Foreign Relations, has written extensively on this topic for those of you interested in really diving in, it’s fascinating stuff (here’s a link). But I digress…

Taiwan is just one example amongst many.

Rick Rieder, the CIO of Blackrock, pointed out in a recent twitter thread (link here) that “Due to the demographic revolution in pension, insurance, and central bank assets, there is roughly 3x as much capital that needs to be invested today as was the case in the early-2000s”.

Rieder goes on to note that though the widening US budget deficit (read, rising Treasury issuance) has helped meet some of this increased demand, it’s still not enough. He concludes by saying “This dynamic has resulted in a dramatic supply/demand imbalance for yielding assets, which is likely to persist for many years, and can be clearly witnessed in the impressive capital flows into income in recent years”.

Another Financial Times article cited a study done by Oxford Economics who calculates that “the supply of these assets [safe DM government debt] will grow by $1.7tn annually over the coming five years — with a $1.2tn issuance of bonds to fund the US budget deficit the largest driver. But demand for these assets is estimated to grow more rapidly, creating a $400bn annual shortfall and indicating that government bond yields are set to remain low.”

Due to regulations and asset matching needs from insurers and banks, the large buyers of these safe assets are mostly price-insensitive. They have to buy US Treasuries and other DM government debt. And with QE over the last number of years and tight fiscal spending out of Europe (read: low issuance) there’s just not much of the stuff to buy… which is one reason why global yields are so low.

And though the rising US deficit is helping somewhat to fix this imbalance, it’s still far from being enough.

What does this all mean from a practical standpoint to us traders and investors?

Everything.

The safe asset shortage is helping to keep yields pinned low. Low yields are good for risk assets and the economy in general. They help ease financial conditions and keep the gears of the economy and financial markets well oiled — not to mention they’re a critical input to DCF calculations and perhaps even more importantly, investor psychology.

Stocks and bonds compete for capital. Higher yields attract flows which then puts the pinch on stocks. Stocks sell-off, bonds get bid, yields fall, and capital eventually flows back to stocks until bonds sell-off to the point where bonds once again become more attractive on a relative basis and the process repeats, ad Infinium.

The global shortage in safe assets is hamstringing this back and forth process somewhat. It’s putting a lid on yields which just makes risk assets, such as stocks, that much more attractive.

That is what Mark is talking about when he says “the valuation metrics everyone has been harping on for the past 10 years are totally and utterly irrelevant”.

Fundamentals matter but people are focusing on the wrong ones.

It’s the supply and demand for assets that drive the long-term cycles in financial markets. Today we talked about the safe asset component of this equation. In a follow-up piece, we’ll discuss net share issuance relative to the global money stock, and what this means for the market.

Stay tuned.