To others, being wrong is a source of shame; to me, recognizing my mistakes is a source of pride. Once we realize that imperfect understanding is the human condition, there is no shame in being wrong, only in failing to correct our mistakes. ~ George Soros

I learned that everyone makes mistakes and has weaknesses and that one of the most important things that differentiates people is their approach to handling them. I learned that there is an incredible beauty to mistakes, because embedded in each mistake is a puzzle, and a gem that I could get if I solved it, i.e. a principle that I could use to reduce my mistakes in the future. ~ Ray Dalio

Alex here.

Every two quarters the Macro Ops team spends a week poring over our last six months of trading. We comb through our winners, losers, and the trades we almost pulled the trigger on, but didn’t take.

We keep detailed records of our reasoning for taking trades and our thoughts on the market at the time (running a newsletter helps). When reviewing, we compare these notes to how things actually played out. Our goal is to see what we got right, what we got wrong, and where we completely screwed the pooch.

This is the most valuable exercise we do. Nothing pays us higher returns than taking a step back and ruthlessly dissecting our process and execution. I’ve learned more from studying my trading journal than I have from reading any trading book…

Like Dalio says, “embedded in each mistake is a puzzle, and a gem”.

Pain + Reflection = Progress.

One of the great things about trading is that mistakes are inevitable and constant. This game is dynamic and complex and we’re all limited in our ability to understand the system of which we’re all an integral part — like the fish who know little of the ocean in which they swim. We all get things wrong. That’s the cost of doing business. This gives us plenty of puzzles to solve, gems to uncover, and truths to realize.

The Palindrome (George Soros), one of the best speculators to have played the game, had a win rate in the mid-30s. On average, 2 out of every 3 trades he made were losers. Yet, the guy was a perpetual money machine over three decades. He knew how to lose and still win. Being good at being wrong is the most important skill set a trader can develop.

One of my favorite market technicians, Ned Davis, put it like this,

We are in the business of making mistakes. The only difference between the winners and the losers is that the winners make small mistakes, while the losers make big mistakes.

Much of our job then, as speculators, is to learn how to make smaller and smaller mistakes by ruthlessly studying our big ones. This is how we uncover first principles that comprise the foundation from which the entirety of our process is built upon.

This is akin to Josh Waitzkin’s concept of “making smaller and smaller circles”.

He notes,

It’s rarely a mysterious technique that drives us to the top, but rather a profound mastery of what may well be a basic skill set.

I’ve spent years dissecting the habits and practices of the greatest traders. And I can tell you that there’s no secret to anything they do.

They are just incredibly efficient at executing the basics:

- Cutting losses short / protecting capital

- Sitting on hands / letting winners run

- Mental flexibility / strong opinions weakly held

- Knowing their edge / efficiently executing that edge

This is what we’ll be going over today. We will revisit the first principles of trading and see where we can make smaller circles and refine our thinking and process with the hopes of improving our performance going forward.

In this review, we will:

- Review our full-year 2020 performance

- Dissect our biggest winners and losers (focusing primarily on the losers)

- Cover lessons learned, the gems we can glean from the mistakes we’ve made

- And finally, we’ll talk about where we are as a trading Collective and where we’re headed over the coming year

Enough with the fluff, let’s get to the goods.

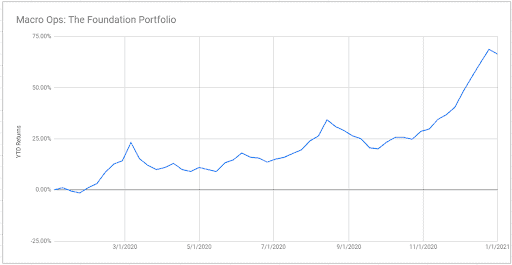

Below are the performance metrics for the Macro Ops (MO) Portfolio:

Macro Ops Portfolio 2020 Return Metrics

Annual Return: 66.40%

Max Peak-to-Trough Drawdown: -14.13%

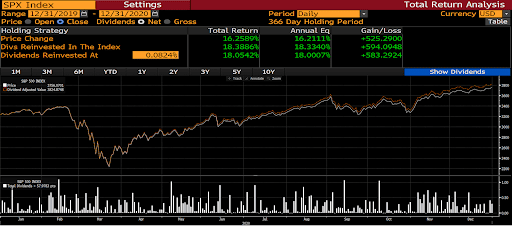

We evaluate ourselves on an absolute basis and don’t compete against any particular index. But for comparison, the S&P over the same timeframe returned 18.38% on the year including dividends reinvested. And had a max peak-to-trough drawdown of -35.42%.

We more than 3.6x’d the S&P’s returns with significantly less volatility.

By any objective measure, these are solid returns. Especially for the MO Foundation Portfolio which we aim to run as a conservative and only mildly active port, where we don’t trade in and out of the market too frequently and take relatively small amounts of risk on trades.

Our long term returns will always directly reflect our ability to execute our process.

It has nothing to do with our brilliance or occasional moments of genius. (We lack the former and are only occasionally deluded by the latter.)

We should emphasize a few keywords here, these being long-term returns.

I often see many traders fall into the trap of doing what we poker players call resulting. Which is assigning meaning to statistical noise (aka randomness). It’s dangerous to make broad assumptions about skill and strategy based on a few hands instead of many cycles at the table. And so it is for traders and investors, where perfectly effective strategies can hit bad streaks that last weeks and months.

Determining what time frame is appropriate for teasing out signal, depends on one’s strategy, trade frequency, and a host of other variables. And even then, the downside of being a discretionary trader/investor is that you never truly know what’s due to skill or to luck — or bad luck.

That’s why we have to rely on logic and a certain amount of faith until we can compile enough data — experience enough cycles — to be able to pull valuable lessons from our results.

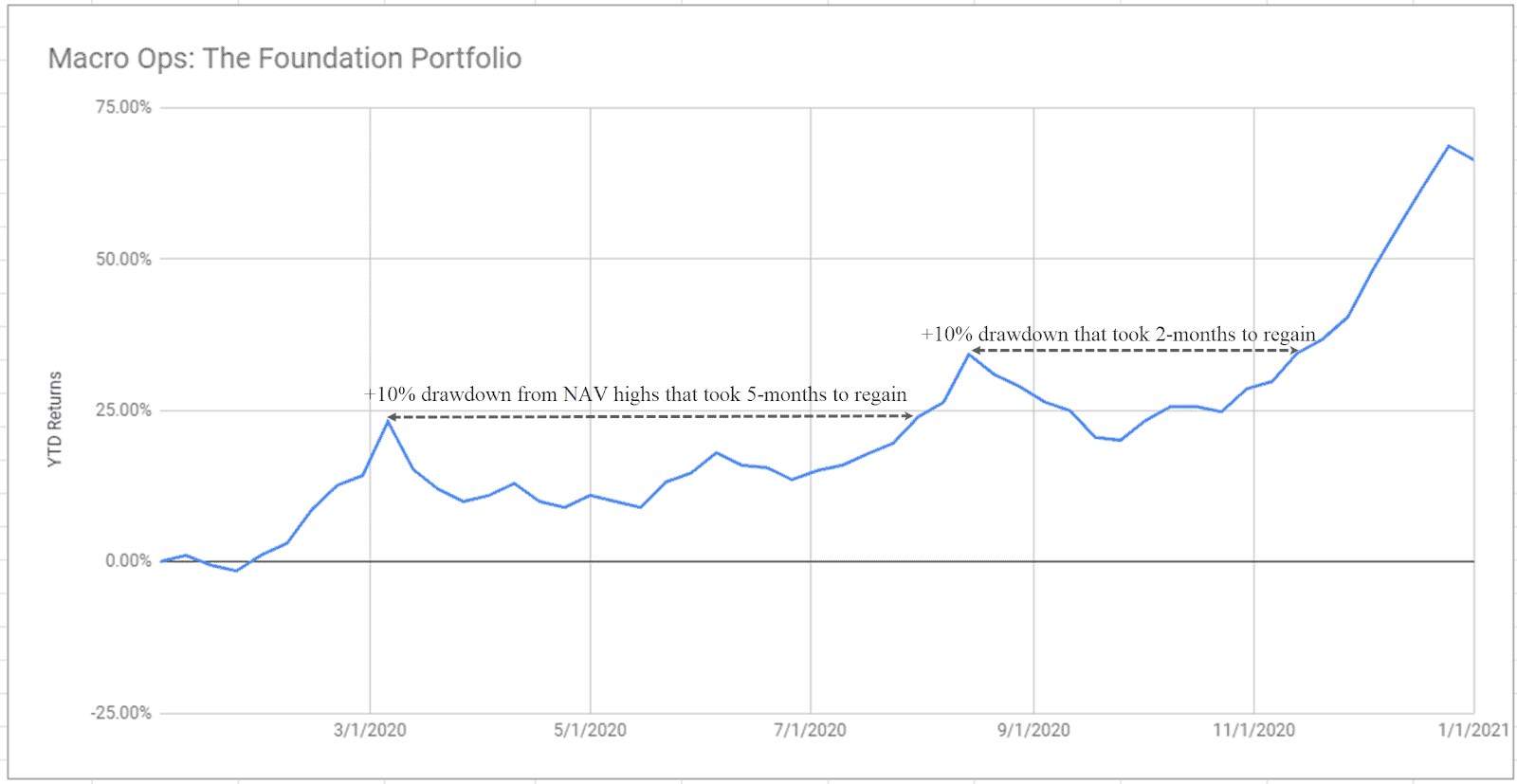

This brings us to an important point. And that’s that as a speculator, you will spend the vast majority of your time in a drawdown from NAV highs. This is a reality of all trading strategies that look to exploit convex opportunities.

The returns for these strategies are inherently bunchy. They follow natural power laws, like Pareto’s 80/20 distribution, or really it’s something closer to 90/10 in markets.

This means we should expect 90% of our profits to come from 10% or fewer of our trades, with the rest canceling each other out. We never know where or when these bottom-line trades are going to come and so we must accept the fact that we’ll spend most of our time just grinding away; taking scratches and small losses and drawing down from equity highs. Until we catch a fat pitch.

Our performance this year serves as a perfect example of these truths: that returns are bunchy and follow power laws, that traders live in near-constant drawdown, and that the merits of a strategy must be evaluated over the long-term.

This year we experienced two 10%+ drawdowns from NAV highs. One took 5-months to get back to new equity highs, the other 2-months.

This seesawing equity path is a feature and not a bug. Our process is built around trying to exploit the 90/10 nature of market returns. The equity paths of the greatest traders follow a similar pattern for the same reasons.

Our job as traders then is to tirelessly work to reduce the amount we drawdown and extend our thrusts up to new NAV highs.

There’s no secret to how to do this. It all goes back to the four basics we talked about at the beginning…

- Cutting losses short / protecting capital

- Sitting on hands / letting winners run

- Mental flexibility / strong opinions weakly held

- Knowing their edge / efficiently executing that edge

Let’s review our trading for the year and see what we could have done better, starting with our mistakes.

To be successful you have to love to lose. ~ Everett Klipp, “The Dao of Capital”

Our biggest errors this year were not in any major losers or bad analytical judgments that we failed to quickly correct, but rather in not fully exploiting our analysis and the rich opportunity set we were presented with.

So while a +66.4% return on the year is good. I give our overall execution a grade of B-.

This is because with our trading style, the gift of volatility we were given, and how correctly we called the market for most of the year, we should have returned double if not more than we did.

In combing through our trading log and journal for 2020 and the last few years, I’ve uncovered the following recurring mistakes in process and execution.

- Too slow to act on a high conviction thesis/setup

- Overly constrictive trade management of highly asymmetric opportunities

- Not sizing up (within limits) on higher conviction opportunities

Let’s walk through each one using some trades this year as examples.

Too slow to act on a high conviction thesis/setup…

Here’s how this one manifests in our trading of the MO Portfolio. We come across an incredibly bullish setup that has a Trifecta of tailwinds (sentiment, fundamental, technical) behind it. We pitch it, write it up for the group. And then don’t take the first entry and watch as our thesis plays out to the T.

Here’s an example.

Bitcoin.

On April 7th, I wrote, “Bitcoin is rising from its basing pattern off of its 200-week moving average (white line), a level which has acted as long-term support a number of times over the years.”

We didn’t buy here and I don’t consider this an error as the technical setup and volatility at the time made appropriate sizing near impossible. But the trade was firmly on our radar.

Where I did make a major error though was on July 27th, when bitcoin was trading under 10,000 and I wrote:

Bitcoin (BTCUSD) just broke out of one of its tightest coils in a long while. Compression regimes such as these tend to lead to powerful expansionary ones (big trends). There’s a host of fundamental reasons to like the play right now, as well. The second round of $1,200 stimulus checks to fund retail speculation is one of them. Now is a good time to load the boat if you don’t already have a position on…

We ended up buying 2 ½ months later and at a 26% premium to what should have been an original entry (using GBTC as the vehicle to express the trade).

While our long bitcoin trade has been a bottom-line winner for us this year and still is as we still have a sizable position on. It was poorly executed relative to the setup and our conviction levels. We left plenty of profits on the table as a result.

I have countless examples of this in my trading journal. My bullish pitch on SNAP in Sep when it was trading around $25 a share. Loved the company, had done due diligence, the technical setup was there… but didn’t pull the trigger in the MO port.

Pitching the bull case for the Nikkei over and over again from June through November but never getting a position on in the port, even though this was one of my favorite plays.

Anyways, it’s a long list and the returns we left on the table are high because of my failure to pull the trigger and properly execute on our analysis the way we should have.

The reason behind this error of execution is also what’s behind our other notable mistakes this year, so we’ll save that discussion until the end of this section.

Overly constrictive trade management of highly asymmetric opportunities…

This is a big one and manifests in a number of ways.

For example, say we have a position that we really like and believe to be highly convex but we either (1) nest our risk-point in way too tight, at a price level that does not invalidate the trade (2) take profits or partial profits way too soon before the technicals or fundamentals have done anything to invalidate the thesis or (3) we don’t give the trade the time it needs to play out and exit the trade without a proper qualifying reason.

Take the small-cap Home Depot of the weed world that I wrote up back in January of 2020. We spent a couple of weeks digging into this company and loved what we found. Was there some hair on trade? Sure, of course, no good opportunity doesn’t have at least some dirt you have to put up with. But the upside potential was obvious to us. Here’s a snippet from our report:

Grow Generation (GRWG) is a fast-growing hydroponic and organic gardening retailer. Yes, it’s a weed play… But unlike the crowded market of branded weed companies that are burning money like it’s 4/20 24/7. GRWG actually has a defensible business, economies of scale, a rock-star management team, and it already produces positive EBITDA…. GRWG looks like it has multi-bagger — or dare I say, dime bag’er… potential? Okay… I know, I know, I’ll show myself out…

We bought a position at $4.90. Got stopped out at $4.20. The stock now trades for close to $50… That’s a 1,000% return in 12-months.

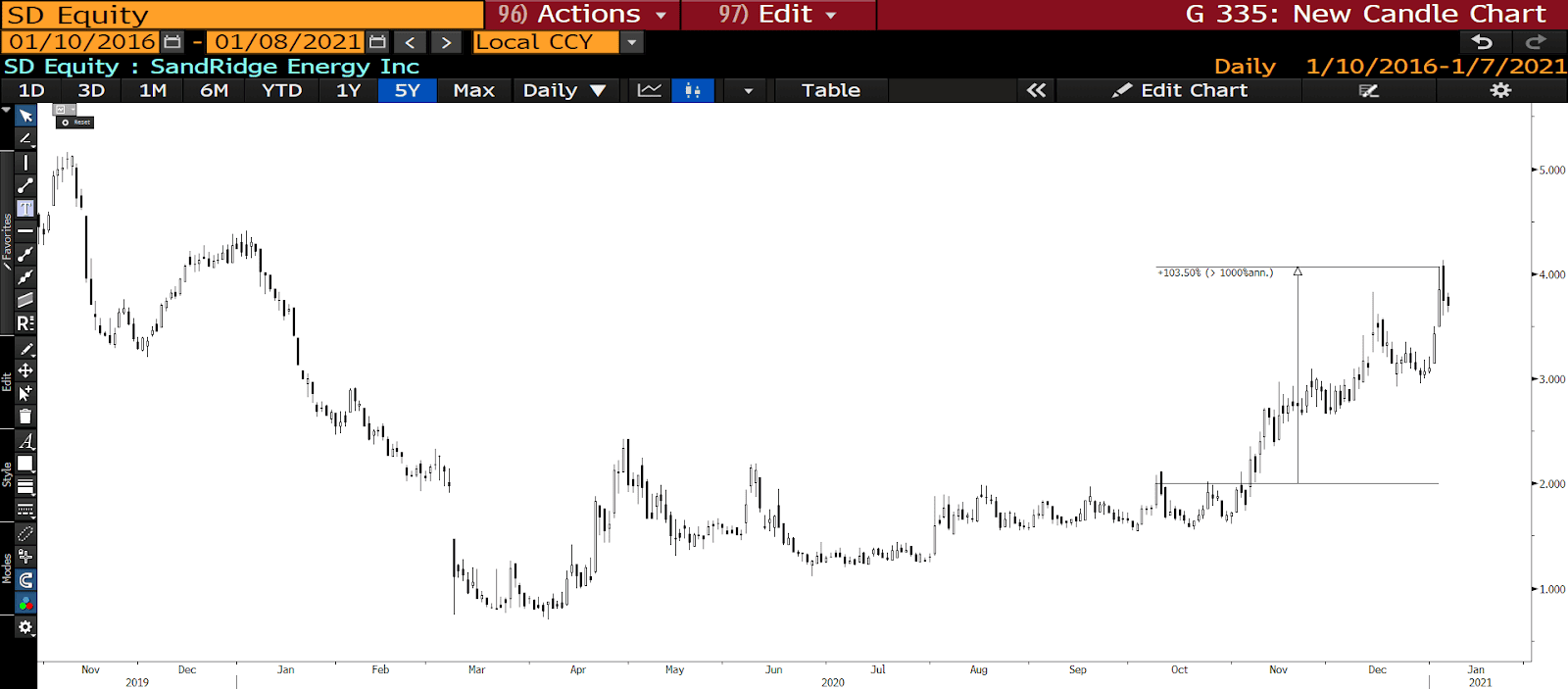

Sandridge is another immediate one that comes to mind. We bought it for $2 a share in October. Cut the position for no good reason a month later, even though our bullish NG thesis was still intact. The stock quickly traded up to $4 over the following 2-months…

There’s a long list of other examples: our exit out of IBKR, taking partial profits on GBTC too soon, not giving our first position in LEU nearly enough room to run…

Now, we have to be careful with resulting… you can exit a trade for the right reasons and yet still lose money or not make as much as you would have if you’d done otherwise. We had a number of those too. But we certainly had our fair share of just piss-poor execution errors and those cost us a good deal of money.

80% of trading and investing is position sizing and exits (trade management). That’s where the money is made over the long-haul.

We have a LOT of work to do on this front and it’s going to be a primary focus of ours going forward.

Not sizing up (within limits) on higher conviction opportunities…

This is similar to the above two. It’s just the process error of not fully exploiting fat pitches. It’s always going to be the case that you have too much size on in your losers and not enough on in your winners… that’s just the reality of this game.

With that said, there is a sweet spot that we have to continuously strive for. Going over our results from the year, it became very clear to Brandon and me that we failed massively on this front and there is a ton of room for improvement.

The above three weaknesses in our trading over this past year all spring from a base of fear. This is an incredibly powerful realization for me personally. It’s one that I’ve thought about in the past but I’ve never given it the needed time for proper reflection until now.

The hesitation to put on trades I really like… the overly constrictive management… not sizing up on high conviction setups, etc… all stem from my fear of being wrong, my fear of losing, and my fear of giving back profits…

Fear is the mind-killer… ~ Frank Herbert, “Dune”

This becomes quite evident when comparing the way I manage my personal fund to that of MO’s. Now, there are some clear style differences; I’m much more active and more aggressive by choice in my PA. But even accounting for that it’s obvious that my fear of being wrong in managing a portfolio publicly is holding me back from efficiently executing on our process.

This is something I’ve been thinking a lot about and discussing with Brandon. As a result, there’s a number of process changes we’re going to be hard-coding in this year in an effort to circumvent and mitigate this hesitancy and timidity from affecting our trading results.

We’ll be discussing these changes in the coming weeks in a series of reports. Process and execution will be a driving focus of ours in 2021. There’s a lot of work to be done, a lot of self-evaluation, and gems to uncover… Brandon and I are looking forward to getting after it.

Now here’s Brandon to discuss some of our equity trades.

Major Equity Calls

Alright, onto the equity book!

We ended the year with twenty (20) positions in our portfolio: 17 longs and 3 shorts.

Our top five positions going into 2021 are as follows:

- Ammo, Inc. (POWW): 12%

- Red Violet (RDVT): 10%

- Grayscale Bitcoin Trust (GBTC): 10%

- Nintendo, Inc. (NTDOY): 9.68%

- Frontdoor, inc. (FTDR): 8%

Let’s dive into each thesis to see how we’re thinking about each position going forward.

Ammo, Inc. (POWW)

POWW is a leading ammunition manufacturer creating a product unlike anything on the market. It has a patented non-incendiary tracer technology. This allows the shooter to see the bullet’s travel path without notifying the recipient.

This is a big deal in warfare. Traditional tracer bullets give away the shooter’s position and everyone can see which direction the bullet traveled.

POWW’s STREAK ammo only allows the shooter (and those behind him/her) to see the path of the bullet through the night.

Another benefit to POWW’s STREAK ammo is its non-incendiary properties. Normal tracer bullets produce heat to create the tracing phenomenon we see. Not POWW. Since POWW’s ammo is non-incendiary, indoor firing ranges allow shooters to use it in their facilities. This is a big deal because it reduces the potential for massive fires that normally coincide with shooting tracer rounds (here’s just one example).

POWW’s done nothing but grow sales like wildfire since our initial investment. Our original thesis estimated $70M in revenue by 2024. At the current pace, POWW should generate >$100M in revenue by 2024 (a 42% increase on estimates). They also just turned EBITDA profitable last quarter while paying off their Jagemann acquisition loan 9-months early.

The stock had a great 2020 rising >200%. But this is just the beginning of POWW’s share price ascension.

POWW can hit $100M in sales by 2024. At a modest 5x 2024 EV/Sales you get a $500M business that’s EBIT profitable. That’s ~$11/share in shareholder value.

You can read our original thesis here.

Red Violet, Inc. (RDVT)

RDVT is a fast-growing, highly scalable data fusion company delivering 1+ trillion points of data to its customers at lightning speed. Their platform allows customers to assess risk and achieve a full-scale picture of any individual and business before meeting/conducting a deal. The company sports a fixed-cost model with 90% incremental gross margins. Management has a history of building similar companies, with two sales totaling $1B in the same industry.

This company is a great example of why current financials mean nothing to a company’s future value. RDVT sports 90% incremental gross margins with a fixed-cost expense model. This means they build the platform and pay for the data once. Then each additional person they bring onto the platform is ~100% gross margin.

We’ve seen this over the last few years as the company’s expanded GM % from 6% in 2016 to 65% LTM 2020.

Over the next five years, we should see GM% hit ~90% on a run-rate basis. Given their fixed-cost operating model, most of the gains will flow through to increased EBIT margins. We estimate RDVT can generate ~39% EBIT margins by 2025.

RDVT’s grown revenues 87%, 90%, and 85% over the past three years, respectively. At a 44% 5YR revenue CAGR we estimate the company generates ~$190M in revenue by 2025. Given its GM% leverage we get 39% EBIT margins, or $75M in EBIT.

That means you can buy this business for 4.2x our 2025 EBIT estimates, or <2x revenues.

We started buying around $17/share. You can read our original write-up here.

Grayscale Bitcoin Trust (GBTC)

GBTC is not a long-term conviction bet for the portfolio. We wanted exposure to BTC and used GBTC as the most logical way to express it. We leveraged technical analysis for entries and exits on this trade.

We started buying GBTC after it broke out of a bullish wedge around $12/share (see below):

The stock entered our portfolio outside the top five. Yet as you know, BTC went on a tear. We held our original position as the stock rocketed over $20/share.

We took half our position off the table around $21/share to lock-in ~75% gains in early December.

A week later the tape gave us another buy signal and we added back the ½ position we sold. Our average cost basis for re-entry was $23.21.

Two days later (12/18) we took profits on that half position at $29/share.

Since then we’ve left a ½ position in the fund and watched it appreciate to $40+/share. The stock remains in our top five due to sheer price gains.

We will likely trade in and out of this name during the year as the tape indicates.

Nintendo, Inc. (NTDOY)

NTDOY is one of the most iconic brands of all time. It dominates the video game space. 20/25 best-selling video games of all time are NTDOY games. Their Intellectual Property rivals that of Disney (DIS).

We first published our NTDOY thesis mid-August (08/18). At that time we were buying shares around $63, or <11x EBIT.

Our NTDOY revolved around one claim: Mr. Market assumed NTDOY followed the traditional boom/bust video game cycle. While that was true on a backward-looking basis, it wouldn’t be the case going forward.

The bull case rested on a three-pronged attack to drive sales:

- Nintendo Switch hardware sales

- Online Subscription model

- Mobile gaming

NTDOY continues to crush Switch sales. They were one of the hottest Christmas items of 2020. Here’s the crazy. The Switch remains the best-selling console of the year despite Xbox and Sony releasing their new consoles.

In 2018 NTDOY released its online subscription gaming service. Subscriptions ranged from $3.99 (1-month membership) to $19.99 (1-year). The subscription offered users many classic Nintendo games. And like Netflix, new games were promised each month. How popular is Nintendo’s new online service? According to daily esports.gg, the company surpassed 15 million paid subscribers in January of 2020. They started the subscription in 2018. That’s impressive growth. Around 27% of Nintendo Switch subscribe — so there’s plenty of room for growth.

NTDOY’s biggest market isn’t hardware sales, it’s mobile gaming. Almost everyone has a smartphone. We all remember Pokemon Go. Some of my friends still play the game today. Pokemon Go generated over $2B in sales. Granted, only 13% of that revenue went to NTDOY (due to third-party developers, etc.). But they learned a lesson: mobile gaming is very profitable.

While we’re up 22% on our position, the stock still trades ~15x NTM EBIT. We continue to look for pullbacks to add to our position. If we’re lucky we’ll get NTDOY to 15% of the portfolio.

frontdoor, inc. (FTDR)

frontdoor, inc. provides home service plans in the United States. The company’s home service plans cover the repair or replacement of components of up to 21 household systems and appliances, including electrical, plumbing, water heaters, refrigerators, dishwashers, and ranges/ovens/cooktops, as well as electronics, pools, and spas and pumps; and central heating, ventilation, and air conditioning systems.

FTDR is run by Rex Tibbens, the former COO of Lyft, Inc. Tibbens brings a technology-first mindset to an otherwise non-tech business (home warranties).

We love where he’s taking the company and Mr. Market doesn’t see the technological advantages in a boring home warranty business.

We bought our initial stake at around $44/share. While the stock returned 17% in 2020, we believe the actual business intrinsic value increased >17%.

The stock trades ~11x our 2024 EBITDA estimates and 2.30x 2024 EV/Sales estimates.

We will likely add to this position getting it to 10-12% of the portfolio. You can read our original thesis here.

What We Did Right: Risk Management

We nailed risk management this year. The steepest peak-to-trough drawdown was 14.35%. Risk management comes in a couple of flavors. First, there’s intrinsic value management. Where you buy assets at prices so low you have a built-in margin of safety.

Then there’s active risk management. This includes placing stop-losses at critical support/resistance levels which, if triggered, allow you to exit with a small loss.

Combined, these two risk management practices create an impenetrable defense against permanent loss of capital.

The “Kicking Ourselves” Bucket

While it looks like we didn’t miss this year, the truth is less forgiving.

The fact is we should’ve had a stronger year than we did. We categorize these mistakes in the “Kicking Ourselves” bucket. One major mistake stands out to me: position sizing.

Take POWW for example. The stock is one of our top-five positions. But it started as a ~3% notional position. This was a clear mistake. We were buying around $2/share when we thought the stock was worth $10-$12/share.

Instead of a 3% position, we should’ve made it an 8-10% notional position immediately. That’s alpha left on the table on a high-conviction bet.

Another example is Roku, Inc. (ROKU). We first bought ROKU on its breakout of the weekly inverse H&S pattern (see below):

ROKU was another high-conviction bet based on our research report released on 09/30 (read here). Unfortunately, we only made it a ~2% position at cost.

We added another 2% to our position in mid-November around $248/share. Still, that only gave us a ~4% position in what should’ve been an 8-10% position.

Conclusion

Alex here.

MO is on a path of continuous evolution and the only way to walk this path is by continuously and ruthlessly studying our failures. This is our highest returning exercise. We look forward to dissecting our future mistakes again six months from now. We hope to be making tighter circles by then.

We’re now in our 5th year as a business which is just wild to me… I wake up every day excited to get to work. I love what we’re creating here and I can’t imagine doing anything else.

The community we’re building is just awesome. We have hands-down the best Collective of hard-charging maniacally obsessed traders/investors anywhere on the web. We’re extremely humbled to serve you guys and gals, and we’re eternally grateful for the opportunity to do so.

While we’ve come a long way in the last four years, we’re only getting started in my mind. Today is Day 1 for us. We have a big vision that we fully aim to execute on. Our mission statement today is the same as when we first started:

- Build the best community of like-minded traders/investors from around the world

- Continuously study markets / theory and share this knowledge with the group

- Create a flywheel of growth where we teach members, they teach us, and on and on

- Use the expanse of the Collective to scour the globe for trades and make lots of money

- Provide the most valuable and highest signal-to-noise research out there

- Develop and share effective quantitative tools to more effectively play the game

- Have a hell of a lot of fun doing all the above…

Over the next few months we’ll be making the following big changes/improvements:

- We’re going to be adding 1-2 quants/coders to our team. I want to build out a small high-speed version of Ned Davis Research. I’m a long-time fan of Garry Kasparov’s (the chess grandmaster) concept of the Centaur approach. This is the idea that by melding unique human intelligence and AI brute force you can arrive at superior outcomes than using just one or the other. There are a few good purely quant research firms out there but even the best ones tend to produce a lot of noise and quant-o-tainment versus actionable data. I’m more interested in building highly tested +EV tools that can be used within an effective framework. We’re in the very early stages of this with the TL Score dashboard, but this is just the very start of what we want to build.

- We’re in the process of setting up a separate legal entity which we will then capitalize and hook up to Fund Seeder and use as a tracking account for the MO portfolio. This will be done by mid-February at the latest and will allow us to provide real-time 3rd party verified performance results. We want to be 100% transparent in everything we do and this is a critical step towards that.

- We’re going to be hooking this account up to a trading journal software where we’ll house our extensive internal notes and reviews on each trade, which we’ll give viewing access to Collective members. Brandon and I also aim to start doing monthly performance / portfolio reviews each month, likely through a webinar for the Collective.

2021 is going to be a great year…

Thanks for being on this journey with us. We’re looking forward to a lot of fun, growth, and profits in the years ahead.

Your Macro Operator,

Alex

There are two mistakes one can make along the road to truth… not going all the way, and not starting. ~ Siddhartha Gautama (Buddha)

***Note: For those of you who would also like to eschew bold prediction making and instead focus on making money. Might I suggest you join our Collective… we just kicked off our annual enrollment and our doors are open. So ponder joining our team.

We do unique research, provide unparalleled training, and have the best group of fun-loving ruthless profiteers on these here interwebs. Our community consists of big-name investors, up and coming fund managers, and die-hard retailers… We share ideas, revel in our shared victories, and commiserate our botched trades. I think it’s the best thing since sliced bread and I’m completely objective in that assessment 😎. Click the button below to join, level up your game in markets, and eat more bacon at your table! ***