Alex here with your latest Friday Macro Musings…

As always, if you come across something cool during the week, shoot an email to alex@macro-ops.com and we’ll share it with the group.

Articles I’m reading —

Jason Zweig writing for the WSJ published an article (link here) highlighting what I think is an important and often misunderstood fact, which is that high GDP growth doesn’t necessarily entail high stock market returns; in fact, it’s often quite the opposite. Zweig writes:

History shows that countries with faster-growing economies often produce lower—not higher—stock-market returns.

“If you told most investment professionals that you would give them future dividend yields, inflation and economic growth rates, they would probably believe they could rank the future stock returns across countries very well,” Mr. L’Her says in an interview. “That has not been the case in the past 20 years—not by far.”

He adds, “Even if you’d had perfect foresight into such factors, you would have done a very poor job forecasting the differences in returns across stock markets.”

One component of return swamped all others in predicting returns: whether the total supply of shares was contracting or expanding. That alone, says Mr. L’Her, explains more than 80% of the extent to which returns have diverged across stock markets over the past 20 years.

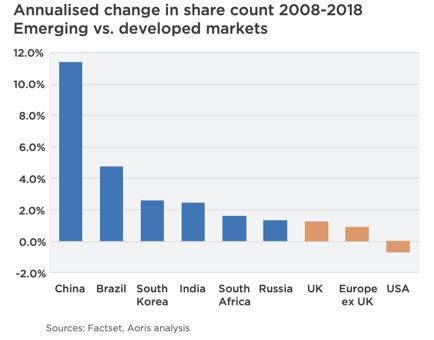

EM companies are notorious for fleecing shareholders. Their dependency on investor capital, despite being situated in high-growth economies, is why “over the last decade real EPS at an index level has more than halved in three of the five largest emerging markets” as Aoris Investment Management points out in this piece (link here) that dives deeper into the subject.

The chart below from Aoris shows that China is by far the worst offender.

Give this profile from Forbes titled The Oracle Of Apopka: Meet Eddie Brown, One Of Wall Street’s Greatest Untold Stories a read (link here). Brown has such an impressive and inspiring origin story. I love learning about investors like this who have a solid record of trouncing the market but are relative unknowns.

Lastly, here’s a short write up (link here) from Kuppy over at the Adventures in Capitalism blog pitching a long Greece (GREK) trade. I like the thesis as well as the technicals.

Charts I’m looking at—

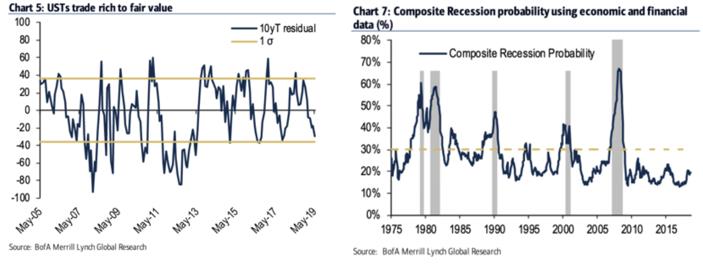

10-year US Treasuries are trading a bit rich on a technical, sentiment/positioning, and valuation standpoint. $ZN_F is now knocking on its monthly upper Bollinger Band; a level that more often than not acts as a significant price repellent.

This move only makes sense if you think a recession is right around the corner. I view that as a low probability event at the moment and am willing to take the other side of the trade. Just need to wait for momentum to wane and a bearish setup to occur, which may be a week or two off but I think we’re getting close. Keep an eye on ‘em.

Podcast I’m listening to —

Patrick O’Shaugnessy’s latest podcast with science writer David Epstein is killer. David is the author of the book The Sports Gene, as well as the newly released Range: Why Generalists Triumph in a Specialized World, which they spend a good deal of the interview discussing.

They cover everything from how Gladwell’s 10,000-hour theory is based on faulty science to how the first Nintendo Gameboy was dreamed up using “lateral thinking with withered technology” to the best learning hacks that few practice. I already bought the book (Collective members, I’m thinking this is our book for the June read. What do you think?). Go and give it a listen. You won’t be disappointed (link here).

Book I’m reading —

This week I found myself revisiting sections of Adam Grime’s book The Art and Science of Technical Analysis. It’s one of my favorite comprehensive books on technical analysis and at the top of my list of books I recommend to traders looking to learn more on the topic.

One of the reasons I appreciate Grime’s work is that he takes a very logical and thoughtful approach to technical analysis. Unlike many tech traders who practice something more akin to reading chicken bones and pattern confirmation bias. Adam lays out when, why, and how technical analysis can provide an edge and more importantly when it doesn’t. Here’s a section from the book (emphasis mine).

“This is important. In fact, it is the single most important point in technical analysis — the holy grail, if you will. Every edge we have, as technical traders, comes from an imbalance of buying and selling pressure. That’s it, pure and simple. If we realize this and if we limit our involvement in the market to those points where there is an actual imbalance, then there is the possibility of making profits. We can sometimes identify these imbalances through the patterns they create in prices, and these patterns can provide actual points around which to structure and execute trades. Be clear on this point: we do not trade patterns in markets — we trade underlying imbalances that create those patterns.”

Quote I’m pondering —

Remember that big stack poker is a game of patience. You don’t have to make a big play in every marginal situation that comes along, just as a good hitter in baseball doesn’t have to swing at balls outside the strike zone. Wait for good solid situations before making big plays. ~ Dan Harrington

That’s it for this week’s macro musings.

If you’re not already, be sure to follow me on Twitter: @MacroOps. I post my mindless drivel there daily.

Have a great weekend.