Dusk Group (DSK) is Australia’s leading home fragrance retailer, with 128 retail stores selling candles, diffusers, and essential oils to customers in-person and online.

DSK has many characteristics of a great business. The company sells an Un-Amazonable product (olfactory sensation cannot be replicated online). DSK also boasts an industry-leading position with a 25% market share with high barriers to entry/scale. Finally, the company’s four-wall unit economics allow it to profitably increase store count while generating a 10x ROCE over the lifetime of each new store build.

We believe that DSK can generate between $30-$50M in annual FCF by 2026 with modest store count/revenue growth (~5% annually). Thanks to the company’s superior four-wall economics, we believe management will pay ~80% of its future free cash flow to shareholders.

The result is ~65% of the current market cap returned to investors through dividends. At the same time, shareholders maintain ownership of a robust, industry-leading, Amazon-resistant business generating $30M+ in annual FCF.

A business we believe private buyers would value at ~8x net profits, or $400M by 2026, representing a 200% upside from current prices.

Time to wake up and smell the profits! Let’s dive in.

Candles: Un-Amazonable w/ Recurring Revenue Revenue Characteristics

Un-Amazonable products are one of my favorite investing models. I first heard the phrase from Cliff Sosin, founder of CAS Investment Partners. You can check out the podcast where he outlined his “Un-Amazonable” thesis here.

Two main characteristics make candles (and diffusers/essential oils) Un-Amazonable. First, customers cannot smell fragrances over the internet (not yet, at least!).

This makes it difficult to buy a candle through the internet. Purchasing one requires olfactory-heavy decision-making.

A scent’s description might read well (who wouldn’t love smelling ‘A Warm Summer Blanket’), but smell awful. Might as well visit the store just to be sure.

The second reason why candles are Un-Amazonable is due to the nature of the purchase. DSK notes that ~30-40% of its sales come from gift-giving events like Mother’s Day or Christmas.

As Cliff mentioned in the podcast (and I’m paraphrasing):

“It doesn’t matter if the toy comes tomorrow from one state over or in five years from Mars. You need a gift today!.”

In other words, gift-givers aren’t always planners and often resort to last-minute trips on the way to birthdays or Holiday parties. This makes DSK’s 128 retail locations highly valuable to candle consumers.

Finally, candles are like SaaS subscriptions. The more a consumer uses candles, the more frequently she needs to buy more. This creates an otherwise unknown, highly recurring revenue stream.

Dominant Market Position w/ High Barriers To Entry

DSK has ~25% market share in Australia’s Home Fragrance industry, which grew at an 8% CAGR from 2017 – 2021.

There are a few catalysts for DSK’s market share dominance.

First, DSK benefits from economies of scale that allow it to profitably operate its 128 retail stores. For example, in 2017, the company had 89 stores and generated a ~2% operating margin. A year later, DSK generated 5% margins with 96 stores.

Today, DSK operates 128 stores and generates ~15% operating margins.

Second, the economies of scale that DSK now enjoys make it difficult for new entrants to compete profitably. Competitors need ~100 retail stores to generate positive economics in an industry that only supports ~$500M in annual revenues.

Third, DSK benefits from strong brand recognition with consumers. Brand recognition matters in an industry dominated by gift-giving revenue generation. Remember, 35% of DSK’s sales are bought as gifts.

Nobody’s Instagramming their shitty $5 Target candle Christmas gift. A Dusk candle feels more personal than a Target candle, which allows DSK to capture more substantial margins on roughly equivalent products.

DSK achieves its brick-and-mortar advantages due to its industry-leading four-wall unit economics.

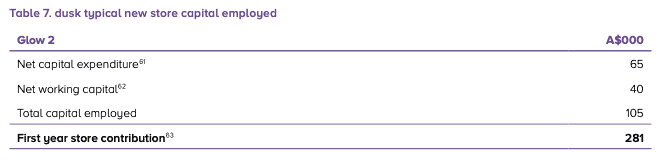

Unit Economics Create Cumulative 10x ROCE

DSK has fantastic unit economics, which you can see below.

The company spends ~$105K to build a new store. That new store then generates ~$280K in first-year revenue. Remove company-wide SG&A costs and each new store generates between 35-40% profit margins.

In other words, DSK spends ~$105K to generate $100K+ in first year operating profits.

But that’s just year one. Mature DSK stores generate ~$900K in annual revenue. That’s ~$350K+ in annual operating profits assuming store-level margins (backing out corporate SG&A, etc.).

In other words, each new DSK store generates a cumulative ~$1.1M in EBIT by the end of its first lease term on $105K of invested capital. That’s a 10x ROCE.

DSK’s unit economic dominance reinforces its brick-and-mortar advantage over its competition. New entrants generate losses to reach a profitable scale (i.e., 100 stores), while DSK prints cash with each new store opening.

This allows DSK to open more stores, refurbish more of its aging storefronts, and return capital to shareholders all without draining the company’s cash reserves. Speaking of shareholder returns.

DSK Is Wildly Mispriced

DSK will generate ~$138M in revenue and nearly $30M in free cash flow by the end of the year. At a ~$130M market cap, the company trades at <5x year-end FCF.

Let’s assume DSK grows store counts by ~5% per year and operates 163 stores by 2026. We’ll also assume the company generates over $1M in per-store sales, accounting for online sales growth (versus $900K in mature store revenue).

That gets us $187M in 2026 revenue.

Next, suppose DSK maintains ~66% gross margins, which aligns with historical norms. That gets us $127M in 2026 Gross Profit.

Finally, we subtract SG&A ($290K/store), cash taxes (~$73K/store), and depreciation (~10% of revenues) to get ~$310K in FCF/store or nearly $50M by 2026.

DSK benefited from COVID-19, and our model shows that. Yet, the company is wildly mispriced regardless if it prints >$30M in annual free cash flow.

For example, DSK will likely generate ~$30M in average annual FCF if women keep buying candles and prefer the in-store experience of smelling the product before purchasing.

The cumulative value of DSK’s future cash flows (assuming a 10% discount rate) is ~$107M or 80% of the current market cap.

However, this doesn’t account for the ~80% dividend payouts DSK will likely pay shareholders over the next five years. Those dividends would be worth nearly $85M assuming a 10% discount rate.

In other words, shareholders receive 64% of their investment back within five years through dividends and get to keep their ownership in a business generating $50M+ in annual FCF.

Finally, let’s conservatively assume that a private buyer would pay ~8x FCF for this business. That gets us ~$400M in shareholder value or $6.45/share (200% upside).