Smart Money and Dumb Money are two terms you often hear in the investing lexicon. Let’s break down what they mean, the indicators and tools you can use to track them, and how to turn this information into more profits in the stock market.

Smart Money Vs Dumb Money Explained

Smart Money investors are typically professionals at hedge funds, mutual funds, and pension funds. They have access to lots of information and resources and are considered rational and disciplined in their investment decisions.

Smart money investors often have teams of analysts conducting thorough due diligence on potential investments. They’re the ones buying satellite images of foot traffic at Walmart to gain an edge on next quarter’s sales figures.

They also have longer-term investment horizons. For example, a hedge fund may spend months analyzing a company’s financials, management team, and competitive landscape before investing in its stock.

Now of course just because they’re called “Smart Money”, doesn’t always mean they make smart decisions. Oftentimes they do the exact opposite. But this is just how they’re labeled.

Dumb Money on the other hand, refers to retail or individual investors who are often seen as less informed and more emotional in their investment decisions.

Most “Dumb Money” investors don’t have the same knowledge and expertise as professional investors. For example, a Dumb Money investor may see a stock mentioned on CNBC or Twitter and buy it without doing any fundamental research or analysis.

But once again, this isn’t always true. “Dumb Money” is just a classification. There are many retail investors that make far better decisions than their professional counterparts.

At the end of the day, the Smart Money vs Dumb Money concept is just a way of discerning which camps are driving stock prices higher (professionals or retail investors).

To summarize:

Smart Money = Hedge funds, pension funds, and Institutional Investors

Dumb Money = Retail or part-time investors

Why does any of this matter?

There’s a tool that tracks the flow of “Smart” and “Dumb” Money in the stock market. It helps us make better investment decisions by letting us know when to buy and sell stocks. Here’s how it works:

How To Use The Smart Money vs Dumb Money Chart & Indicator

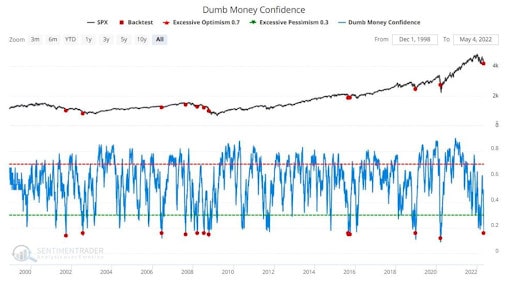

The Smart Money vs Dumb Money Indicator is a tool traders can use to analyze the sentiment and positioning of our two investing groups. The indicator, which we get from Sentiment Trader, uses data on buying and selling activity to determine the market’s overall sentiment.

Here’s a screenshot of the smart money vs dumb money indicator below:

When the blue line is above the horizontal red line, it means the Dumb Money is overly bullish.

When the blue line is below the horizontal green line, it means the Dumb Money is overly bearish.

Here’s what you need to know:

When the Dumb Money is overly bullish, you should be bearish.

When the Dumb Money is overly bearish, you should be bullish.

Here’s why…

The Importance of Sentiment and Positioning in Trading

The Smart Money vs Dumb Money Indicator shows sentiment and positioning in the market. It tells you how retail investors are feeling and how they are investing their money as a result. This is a great signal you can use to direct your own investments.

Suppose the Dumb Money indicator shows that retail investors are overly bullish in the stock market. This is a signal that the market is likely overvalued and will soon roll over. This is a good time to sell.

This happens because the retail investors who make up the Dumb Money are often influenced by emotions and can easily drive asset prices much higher than their actual value. Markets driven higher by “Dumb Money” aren’t a sign of improving fundamentals, but rather an increasing sense of FOMO and excessive risk-taking.

This is a signal that sentiment is overly optimistic and positioning is overcrowded. This is where our team at Macro Ops will start to sell a position because we don’t want to be the last pig off the Lemmings cliff when the market crashes.

This same indicator can also be used to identify a market the Dumb Money doesn’t want to touch. These are situations where Mr. Market has drained the confidence of every last investor and no one wants to invest.

A great example is the stock market in mid-2009. No one wanted to put their money into stocks after the financial crisis. Sentiment and positioning were at all time lows. This resulted in a strong signal that the crash was over and it was time to invest. And those that did buy made a killing over the next decade.

Stanley Druckenmiller is one of the most successful traders who uses sentiment and positioning to make his investment decisions. If you’re interested in learning how he’s used this technique to make billions of dollars, check out our piece on how to read market sentiment here.

Hopefully you now have a solid understanding of Smart Money vs Dumb Money and how it affects your investments.