On being a contrarian from Michael Lewis’ Liar’s Poker:

Everyone wants to be, but no one is, for the sad reason that most investors are scared of looking foolish. Investors do not fear losing money as much as they fear solitude, by which I mean taking risks that others avoid. When they are caught losing money alone, they have no excuse for their mistake, and most investors, like most people, need excuses. They are, strangely enough, happy to stand on the edge of a precipice as long as they are joined by a few thousand others…

Contrarianism is the most abused and empty platitude in trading and investing. Everybody thinks they’re one, but few are.

And that, by its very nature, has to be the case. Because to be a contrarian is to go against the herd, the majority.

Hedge-fund legend Ray Dalio puts it like this, “You can’t make money agreeing with the consensus view, which is already embedded in the price.”

In case you don’t have twitter (good on you, you’re a better person than I!) or missed my recent thread on the subject of “How To Read Market Sentiment”. You can find the entire thread here. Let me know if you have any thoughts or comments.

2. Speros Drelles was teaching the young Druckenmiller about the wisdom of the market, which is based on the idea that the crowd is collectively smarter than any one individual. This collective intelligence was first stumbled upon by the late great statistician, Francis Galton, who…

3. …in 1906 observed a competition at a local fair where approx. 800 people tried to guess the weight of an ox. To his surprise, the avg of all the guesses was 1,197lbs. The real weight… 1,198lbs. Countless studies have been done since. All show similar results…

4. Crowd > any individual. Scott Page, in his book “The Difference”, lays out the “diversity prediction theorem” to explain how this works and what variables are needed to make a crowd wise. The theorem states that: Collective error = avg individual error – prediction diversity.

5. The implications of this are 3-fold:

-

- A diverse crowd will always predict more accurately than the avg individual

- A crowd is often smarter than even the best of its individuals

- Collective predictive ability is equal parts accuracy & diversity.

6. Takeaway: Crowds are smarter than any single person, as long as there’s a diversity of opinion. This theorem is based on math and is always true. @mjmauboussin has a great paper on this for those of you who want to explore more (link here).

7. To take this back to markets. Here’s Soros explaining why it’s KEY to know when to be a part of the “herd” (ie, follow the trend) and when to disengage & be a contrarian:

Being so critical, I am often considered a contrarian. But I am very cautious about going against the herd; I am liable to be trampled on… Most of the time I am a trend follower, but all the time I am aware that I am a member of the herd and I am on the lookout for inflection points… I watch out for telltale signs that a trend may be exhausted. Then I disengage from the herd and look for a different investment thesis. Or, if I think the trend has been carried to excess, I may probe going against it. ~ George Soros

8. You want to be a trend follower when there’s a lot of people saying “this move makes NO SENSE” and a contrarian when people are saying “this makes so much sense”. This is why a bull climbs a wall of worry & a bear falls down the stairs of hope. Trends are driven by (dis)belief

9. But… and this is important. You ONLY want to be a contrarian once the tape STOPS confirming the consensus narrative. Reading the sentiment tea leaves is as much an art as it is a science. And when in doubt, defer to the market.

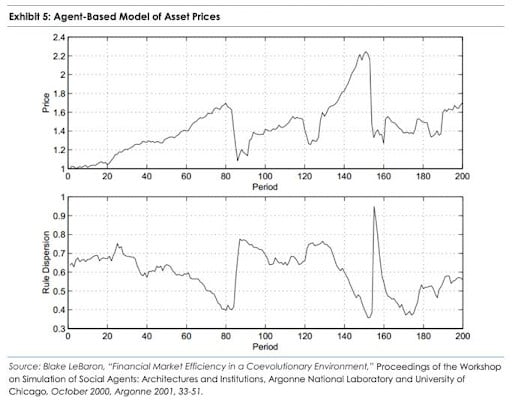

10. Blake LeBaron, an economist, modeled how this diverse opinion/wise crowd & consensus/dumb crowd works in markets to create trends and crashes. Here’s his paper

11. He built a computer model and imbued “agents” with decision-making rules such as: make money, try not to lose money, don’t underperform the average for long periods etc…

12. What he found was that “During the run-up to a crash, population diversity falls. Agents begin to use very similar trading strategies as their common good performance begins to reinforce… This makes the population brittle…Traders have a hard time finding…

13. …anyone to sell to in a falling market since everyone else is following very similar strategies.” This confirms Page’s “diversity…” theorem and explains the mechanics of why markets trend and revert, or move in sine waves.

14. Trends that “make no sense” = robust. Trends that become consensus = fragile. Soros thought of this phenomenon as high and low “distortion regimes”. High distortion regimes = when price & sentiment form a reflexive loop, which then creates a budding consensus.

15. Low distortion = diverse opinion. This price/sentiment loop, or what I call the “Narrative Pendulum” becomes obvious once you learn to look for it.

16. For example, watch this video I clipped together last year that shows the dramatic shift in the dominant narrative that occurred in just two-weeks time (link here).

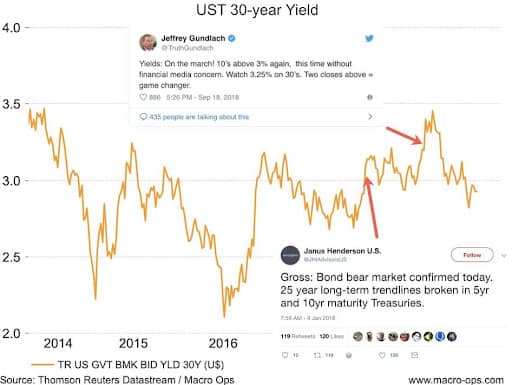

17. Price drives sentiment which drives price, ad Infinium. And THERE IS NO “SMART-MONEY” other than the mrkt itself.

All of us are part of the “DUMB MONEY” crowd. The 2 “Bond Kings” calling the end of the bond bull at the exact bottom in 18′ is case in point. THIS GAME IS HARD

18. So that’s what Drelles meant & also what makes Druckenmiller so good. He learned early on to listen and respect the market, to harness the wisdom of the crowds, and to only step in to fade a trend once a consensus was clear & the tape no longer confirmed it.

One of my strengths over the years was having deep respect for the markets and using the markets to predict the economy, and particularly using internal groups within the market to make predictions. And I think I was always open-minded enough and had enough humility that if those signals challenged my opinion, I went back to the drawing board and made sure things weren’t changing. ~ Stanley Druckenmiller

Fin/

Whether one knows it or not, we’re all playing Keynes’s Beauty Contest. Most dither at the first level completely unawares. Hopefully, this thread helps you see the market for what it really is so you can begin playing the game at the second, third levels, and beyond…

We’re currently working on a report about where we see the MOST one-sided positioning and consensus out of any market around the world. This consensus has created what we believe is an extraordinarily asymmetric opportunity.

Jim Rogers, the famed partner to George Soros during the ole’ Quantum days, likes to say:

The way of the successful investor is normally to do nothing — not until you see money lying there, somewhere over in the corner, and all that is left for you to do is go over and pick it up.

Well, suffice to say, we at MO see a disgustingly large pile of money just sitting over in the corner right now… just waiting for some free-thinking investors to come and scoop it up.