Last we discussed Accounts Payable and the role they play in cash flow efficiency. We learned that one company’s A/R is another company’s A/P. This week we’re analyzing one of the more complex accounting problems: capitalizing research & development (R&D) costs.

We’ll learn the difference between capitalizing vs. expensing, why it matters and how it changes margins, profits and returns.

Why We Should Capitalize R&D Costs

US GAAP accounting requires companies to treat R&D as expenses on the income statement (P&L). That biotech company spending $1M developing a new drug? Under GAAP that’s a $1M expense, not an asset.

This distorts profits, margins and ROA calculations for many tech/R&D heavy firms. That’s not ideal. Think about it. Companies that leverage R&D to generate revenue and cash have periods of massive R&D investment.

If you don’t adjust for R&D, the income statement looks like a bouncy ball on cocaine.

Investments in R&D support the long-term cash-flow generation of a company. They’re operating assets. As such, we should capitalize them on the balance sheet.

Capitalizing R&D is also a more conservative estimation of a company’s returns and profitability for two reasons:

-

- Capitalizing increases a company’s total assets (which could reduce ROA/ROE)

- Capitalizing keeps an amortization expense on the income statement

Let’s learn how to do that.

Capitalizing R&D Investments (Step-By-Step): Boeing, Inc. (BA)

We’re using Boeing (BA) as our example. Remember, we’re keeping things simple with this example. You can get more complex (see here), but that’s not our goal.

Step 1: Find Amortization Duration

The first step in capitalizing R&D is to determine the useful life of a company’s R&D assets. The longer the usefulness, the longer the amortization period (i.e., how many years we expense). High-tech companies in ever-changing industries have low amortization periods.

BA makes airplanes that have long lifespans. We’ll use ten years.

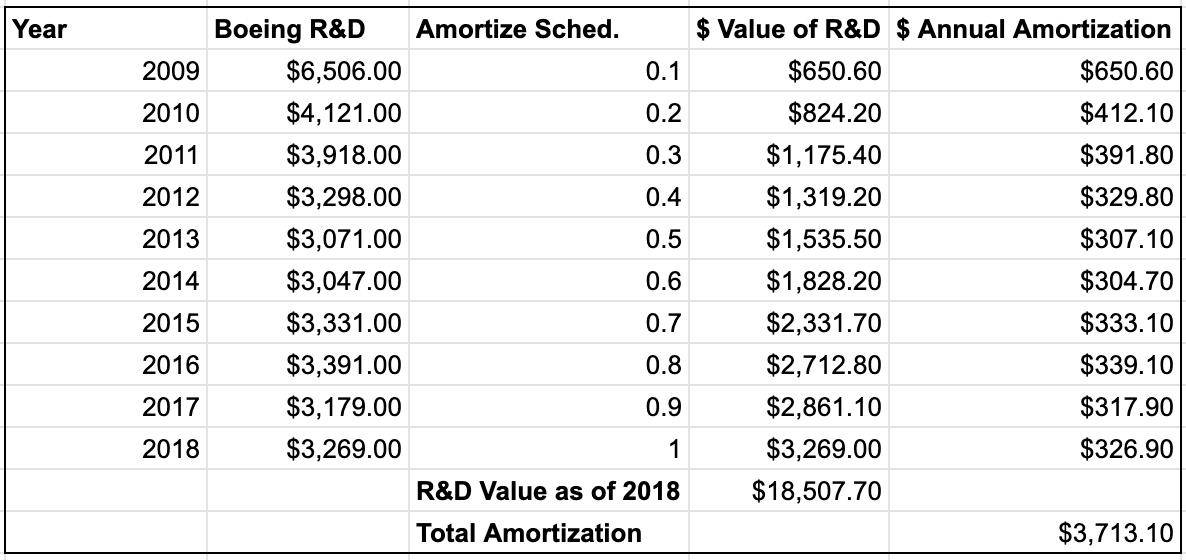

Step 2: Calculate Value of Amortized R&D Asset

We calculate the amortized value of the R&D asset by using the straight-line amortization method. This means we amortize 1/10th of the total sum of the last ten years’ R&D expense. If we chose 7 years, we’d amortize 1/7th of the total sum of the last seven years’ R&D expense.

Then we calculate the annual amortization expense by dividing that year’s R&D by 1/10th (0.1).

Here’s what that looks like:

Step 3: Recalculate Book Value of Equity

We need to add our capitalized R&D value to tangible book value to get a better picture of the company. This is simple. Take Tangible Book Value and add R&D value.

Here’s what that looks like in 2018:

$339M (BV) + $3.27B (R&D value) = $4.059B

Step 4: Recalculate EBIT

Next we adjust EBIT to reflect our capitalized R&D investments. To do this, we take our current year EBIT, add current year R&D expense and subtract total amortization of R&D.

Here’s what that looks for BA in 2018:

$11.6B (EBIT) + $3.27B (R&D) – $3.71B (Amortization) = $11.16B Adjusted EBIT

Why does EBIT drop after adjusting for R&D investment? BA’s decreasing R&D investment (see above).

To Be Continued …

I know, capitalizing R&D is confusing. But it’s important if we want to understand the true economics of an investment-heavy business.

We’ll review this concept in more detail next week, don’t worry.

If you have any questions feel free to reach out.