Alright, it’s that time of year where we review our winners, losers, mistakes, and misses. Regular reviews of performance are a trader’s shita-kitae. Just as a master swordmaker continually pounds, folds, and heats a block of steel in his efforts to forge the perfect blade. We traders and investors, need to routinely pore over our trade logs, with a ruthless eye for honest clarity, and correct the weaknesses in our game.

This is how we remove impurities, sharpen our blade, and forge an enduring and profitable trading business.

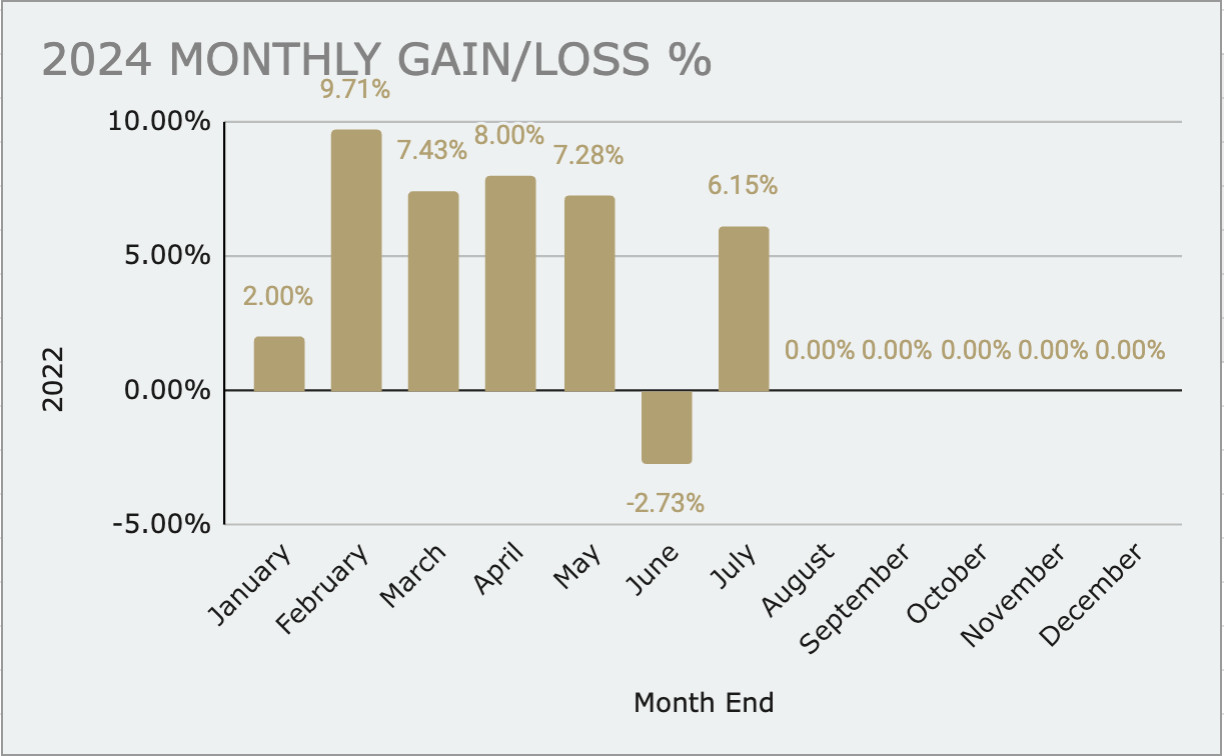

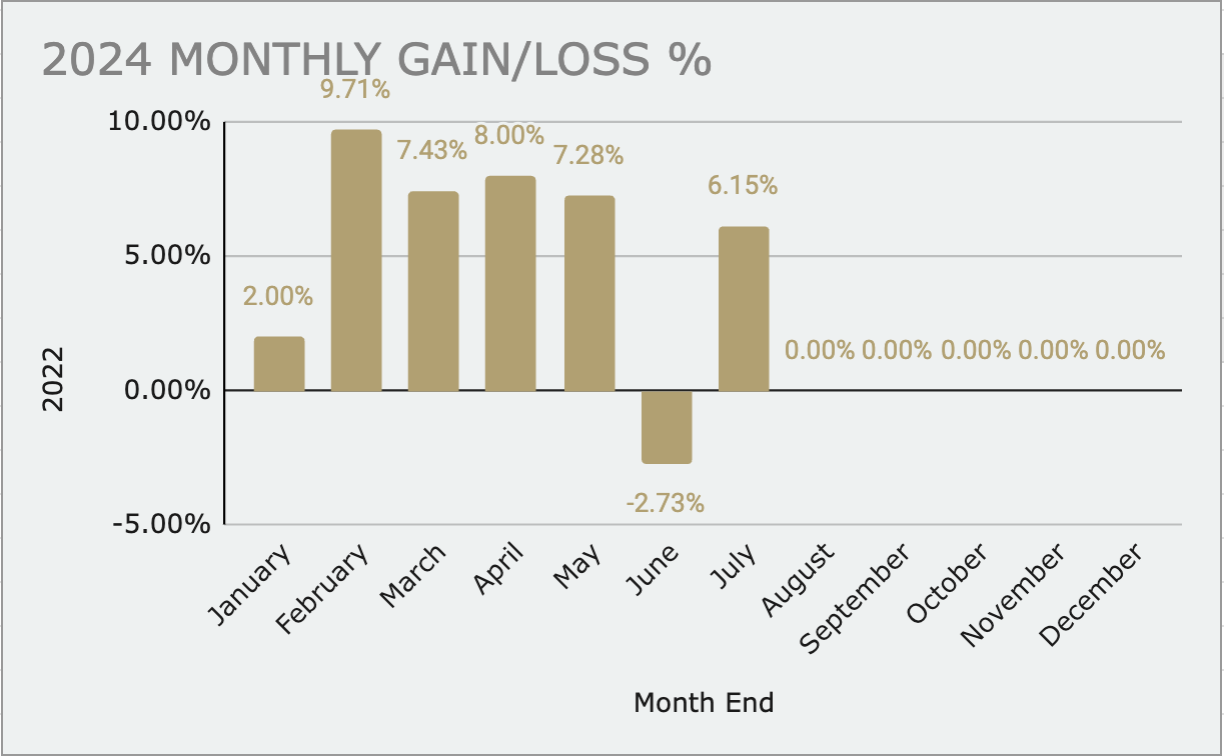

To start, here’s our portfolio numbers for the first six months of the year.

1H 2024 Return Metrics

- 1H 2024 Return: +31.69%

- Strongest Month: February (+9.71%)

- Worst Month: June (-2.73%)

- Gain-To-Pain: 11.61x

My partner Brandon wrote up a review of our equity trading performance yesterday, which you can find here.

These are okay year-to-date returns. For context, our average risk per trade over the past 6 months was roughly 55bps. We use fractional betting so our total risk simply measures the distance between our entry and our stop relative to the size of our total position.

This means we can take, say, a 50bps loss on a position should we get stopped out. But the nominal size of our position can be 10-20% or more, depending on how tight we’re able to nestle in our risk point.

As the graph above shows, we had five positive months and one down month since the start of the year. Our single negative month was a loss of -2.73%.

But these are just numbers. And numbers can mask quite a bit. They don’t tell the full story. And truth be told, I give our year-to-date performance a B-. It was decent. But it should have been so much better, considering the available opportunity set.

(Housekeeping note: Enrollment into our Collective closes tonight at midnight and won’t open again for a good while. So if you’re interested in joining our team, click this link here to learn more. Don’t hesitate to shoot me any questions you may have.)

Let’s dig in and review why that is and see where we can tighten things up.

In trading, we can make errors of omission, where we fail to do something that we should have done. And then there are errors of commission, where we take action but we flub it, get sloppy, and screw the pooch, so to speak.

Now the team and I made plenty of both this year. But the one that really gets me is not fully exploiting the biggest thematic winner of the year, which was again AI.

I’m fine missing trades. It happens all the time. Doesn’t bother me one bit. But missing a major thematic that I’d been bulled up on and writing about since 2018 and before (example: Underwriting The Future). Well, that’s a good kick in the shins.

The little solace we gave ourselves was that we were hitting the Qs hard to the long side throughout the year. So we were still benefiting from the trend, sure. But honestly, that’s loser talk. We flubbed this one badly. It stings.

And while the AI trade started at the end of 2022 (and yeah, we sat on the sidelines then too), NVDA gave us a cherried Trifecta setup at the start of the year. I was tracking it too. But didn’t pull the trigger. Why? No good reason. I was too busy looking at obscure secondary and tertiary plays on this thematic, like tin miners in the DRC that have gone nowhere for two years.

I chalk it up to my masochistic side that comes out every now and then.

Honestly, my biggest failures this year have almost entirely been ones of omission. There are so many examples of me pitching a trade, planning to put it on, not putting it on because <shrug emoji>, and then watching it Falcon V it all the way to Valhalla.

This reminds me. You know what’s a super important but underserved topic in this game?

Table selection.

Table selection is an old poker term. It means what you think it means. The idea is that if given a choice, you’re better off playing at a table full of loose deep-pocketed fish versus one filled with tight-fisted salty types.

The pokerbank puts it this way, “To win money from poker, you can either develop a better strategy than your opponents, or play against worse players than you. Why not do both?”

We agree.

Table selection is just as important in trading and investing.

And the process for picking the best table to play at is actually quite similar. We want to play at the tables with the most action. The ones packed with drunk weekenders betting on every preflop and routinely going on tilt.

How do we identify these tables/markets?

Easy. Where’s the action at? Where’s the most volatility and the biggest trends? What’s the emotional retail crowd gambling in?

The answer to that question has been, for the most part over the past number of years at least, the crypto market. Particularly altcoins. This year it’s also been semiconductors.

The point is that it’s important to play where the action is, where the biggest trends are. I’ve never understood it, but many players tend to treat all markets as equal. But that’s never the case. At any given time, there’s always 1 or 2 markets that are moving like a bull hit with lightning. We want to be sitting down at those tables. Makes this game a hell of a lot easier.

Our table selection could have been better over the last six months. We’re working on creating better processes to make sure we’re more often than not, playing with the drunks in the future.

But I digress…

On the macro side, our biggest profit centers this year have been repeatedly hitting NQ on the long side. Along with running bull campaigns in gold and silver, as well as BTCUSD. Oh, and the Nikkei to the long side at the start of the year. That was one of our bigger winners ytd.

We made a little money in Ags (long wheat). And about broke even in currencies — though I think FX will be one of our big profit centers in the second half of this year.

Something we’ve done well this year was simply cutting out the noise and executing our process. So much of trading is just getting the Risk Cycle right. Both the larger cyclical one and the smaller sentiment/positioning shifts.

This reminds me of a quote from Bessent (a protege of both Soros and Druckenmiller) who put it like this:

I was at a money manager roundtable dinner where everyone was talking about “my stock this” and “my stock that”. Their attitude was that it doesn’t matter what is going to happen in the world because their favorite stock is generating free cash flow, buying back shares, and doing XYZ.

People always forget that 50% of a stock’s move is the overall market, 30% is the industry group, and then maybe 20% is the extra alpha from stock picking. And stock picking is full of macro bets. When an equity guy is playing airlines, he’s making an embedded macro call on oil.

50% of a stock’s move is the overall market… And in my humble opinion, it’s closer to 60-70% for many stocks. So, sure, you can build a fancy earnings model for so and so company. But if you’re buying when population diversity is falling (ie, punters are crowded long the broader market) then you’re likely to end up in the red. No matter how right you’re on the fundies.

That’s why we prioritize the Hierarchy of Technicals in our Trifecta process. We let the tape, internals, and positioning data tell us what’s what. This doesn’t mean we always get it right. But it does mean that we’re right more often than not. And more importantly, it ensures we get it right when it really counts (ie, avoid big drawdowns and catch most big trends).

Using tools like our Trend Fragility Score, our Market Internals Aggregator, and others… helped us to stay on the right side of the trend for most of this year. And that more than anything (outside of ruthlessly sticking to our trade and risk management systems) is what’s allowed us to put up the numbers we have.

Not to mention it allows us to stay above the fray and exit the constant narrative chatter about market crashes and imminent recession dangers, that somehow pass as intelligent market analysis these days.

Looking ahead…

I expect the second half of the year to be more entertaining than the first. If albeit, a bit more challenging. I’m most excited to see how the number of major compression regimes we’ve been talking about for the past two months, resolve themselves.

It seems to me that we have some big moves coming in the major USD pairs.

China is the white dragon in the room. The 3rd Plenum disappointed markets in a major way. This is why we’ve seen the recent fire sale in things like copper and AUDUSD. The CCP is a black box and all. But if China aims to hit its coveted growth target, then they’re going to have to stimulate in a big way sometime in the third quarter. Only Confucious knows… but more plugged in China watchers than I believe stimmy is coming.

And watch out if so, because the market is not positioned at all for that.

From a trading and investing standpoint we’re going to work on creating better airtight processes for executing on our analysis. And not letting as much performance slip through the cracks due to plain sloppy execution. That’s unsat. So we’re going to knuckle down on that and get better as a team.

Speaking of team… We’ll have some news to share with the Collective in the coming weeks. We’re making some big changes on all fronts here in an effort to provide more value to the group and evolve into our next iteration as a company.

That more than anything, has me excited.

I’ll be out with a Market Note this afternoon updating our thoughts on the recent volatility, market rotation, and some FX setups. So keep an eye out for that.

Until then, stay frosty and keep your head on a swivel.

Enrollment into our Collective is open until the end of this week. The Collective includes all of our research, a full library of reports and videos on theory and strategy, our proprietary market dashboard, plus our internal slack where the team and I, plus fund managers and die-hards from around the world talk shop, exchange ideas, and shoot the shit. Our book is up +40% ytd and if you’re interested in joining our crew, just click the link below. Looking forward to seeing you in the group.