Remember these headlines from a few months ago? This was the consensus hot-take following the March 23rd bottom in the market in response to its rip-roaring recovery. There was an audible “huh…” with plenty of head-scratching from the punditry and investor class. Why would “stocks soar despite coronavirus and a recession”? Clearly, it “didn’t make sense” and would “end in tears”.

Not only did the market bottom fit the bill of our “No-Sense Algorithm” but it actually made perfect sense. Why?

One word: fiscal.

On the day the market bottomed it became clear that the government was going to pass a massive fiscal package, one of its largest in history.

A few days later the CARES Act passed. $2.2trn in aid was earmarked to go out to the public. The market went vertical over the following 9-months, completely retracing its earlier losses and then some. All despite rising case counts and an incredibly bleak health and economic outlook.

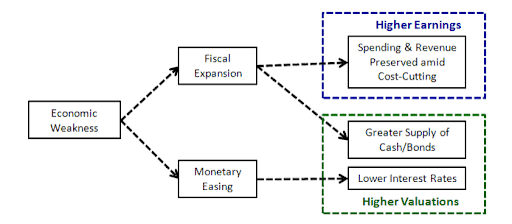

Here’s the thing… Fiscal is the ultimate cheat code. It has the ability to boost earnings, jack up asset prices, and hit a set nominal growth target at will. And with the long-term Kuhn Cycle paradigm shift that has taken place amongst policymakers throughout developed markets, fiscal is going to become an ever-increasing driver of the economic, financial, and risk cycle.

This is a shift no less significant than the one we’ve seen from our Game Masters, at the Fed. The two working in tandem provides an ever potent cocktail that will have dramatic and lasting effects on the speculative game we play.

In this piece, the third installment of our understanding of initial conditions so we don’t make predictions 2021 series. We’re going to layout the mechanism of how fiscal works and what that means for markets going forward. This subject is ever more important now that we’ve got a Dem sweep in Georgia, giving the Democrats carte blanche to run their own fiscal policy.

Most of what’s to follow is a summary of what I consider to be the most important market/econ related piece I read in 2020. It’s titled “Upside-Down Markets: Profits, Inflation and Equity Valuation in Fiscal Policy Regimes”. It was written by the anonymous twitterer @Jesse_Livermore for O’Shaugnessy Asset Management.

I highly recommend you read the piece in full. Probably 2-3 times. And take a LOT of notes. It’s that important of a framework to understand where we’re going. At over 40,000 words it’s basically a book. It covers a wide range of topics; from the Levy-Kalecki equation to financial flows and portfolio preferences, and inflation. All of which are key to understand the driving dynamics of this market going forward.

For today’s piece, we’re sticking to the fiscal discussion. We’ll be saving the inflation topic — a critical variable to the fiscal policy space — for another day.

First, a brief definition.

An “upside-down” market is one that reacts positively to bad economic news and negatively to positive news. The reason is policy… This concept should be familiar to most as we’ve spent the last decade in a kind of upside-down market where bad news meant a more dovish Fed, which was good for asset prices. This is the result of a heavily financialized slow-growth economy that’s become dependent on policy “innovations”, both monetary and fiscal, to keep the game going.

With that, let’s begin with this hypothetical virus scenario from Livermore’s paper (emphasis by me):

…monetary policy is limited in what it can accomplish as a form of stimulus. It, therefore, offers a weak foundation for upside-down markets. We can celebrate economic problems as catalysts for interest rate cuts, but the cuts won’t usually avert the problems, at least not in full. They may buoy stock prices through portfolio preference channels, but the damage to fundamentals will tend to outweigh the buoyancy.

Fiscal policy is an entirely different matter. If deployed in sufficient quantities, it can achieve any nominal level of spending or income that it wants. When policymakers commit to using it alongside monetary policy to achieve desired economic outcomes, markets have solid reasons to turn upside-down.

To illustrate with a concrete example, imagine a policy regime in which U.S. congressional lawmakers, acting with the support of the Federal Reserve (“Fed”), set a 5% nominal growth target for the U.S. economy. They pledge to do “whatever it takes” from a fiscal perspective to reach that target, including driving up the inflation rate, if the economy’s real growth rate fails to keep up. Suppose that under this policy regime, the economy gets hit with a contagious, lethal, incurable virus that forces everyone to aggressively socially distance, not just for several months, but forever. The emergence of such a virus would obviously be terrible news for humanity. But would it be terrible news for stock prices?

The virus would force the economy to undertake a permanent reorganization away from activities that involve close human contact and towards activities that are compatible with social distancing. Economically, the reorganization would be excruciating, bringing about enormous levels of unemployment and bankruptcy. But remember that Congress is in-play. To reach its promised 5% nominal growth target, it would inject massive amounts of fiscal stimulus into the economy—whatever amount is needed to ensure that this year’s spending exceeds last year’s spending by the targeted 5%. To support the effort, the Fed would cut interest rates to zero, or maybe even below zero, provoking a buying frenzy among investors seeking to escape the guaranteed losses of cash positions.

The interest rate cuts, possibly into negative territory, would make stocks more attractive relative to cash and bonds. Additionally, the massive issuance of new government securities to fund the spending would shrink the relative supply of equity in the system, making stocks more scarce as growth-linked assets. Finally, the virus would give corporations financial cover to cut unnecessary labor expenses, allowing them to capitalize on any untapped sources of productivity that might be embedded in their operations. This action, which takes income away from households, would normally come back to hurt the corporate sector in the form of declining demand and declining revenue. But if the government is using fiscal policy to achieve a nominal growth target, then there won’t be any income or revenue declines in aggregate. The government will inject whatever amount of fiscal stimulus it needs to inject in order to keep aggregate incomes and revenues growing on target, accepting inflation as a substitute for real growth where necessary.

If you are a diversified equity investor in this scenario, you will end up with a windfall on all fronts. Your equity holdings will be more attractive from a relative yield perspective, more scarce from a supply perspective, and more profitable from an earnings perspective. The bad news won’t just be good news, it will be fantastic news, as twisted as that might sound.

This hypothetical is just that, a hypothetical… Thankfully as serious as COVID it’s not as dire as the scenario outlined above. Nor has the Fed hasn’t set negative nominal rates and Congress hasn’t (yet) enacted a nominal growth target. But, our current environment isn’t too dissimilar and is inching its way towards a more fiscally dominated one. Hopefully, sans the virus.

The market collectively is waking up to this fact which is partly why we can have seemingly insane things happen such as the violent takeover of our Capitol building and a real threat of a non-peaceful transfer of power, and yet SPX catches a strong bid.

The soon-to-be Senate majority leader Chuck Schumer is saying they aim to move on another round of $2,000 stimulus checks asap. Again… Fiscal is a cheat code. If applied in sufficient amounts it can and will override all other concerns.

Here’s a brief summary of how this works.

Think of a simplified macro model of the economy that consists of Households, Corporations, and Government. This system is circular in that one entity’s spending is another’s income. Thus, the saving and spending decisions of each entity affect the system as a whole.

For instance, households collectively have a propensity to save because naturally, they want to increase their wealth over-time. In this model, saving is equative to running a surplus. And for one entity to run a surplus it means by a matter of accounting identify that another (either corporations or government) has to run a deficit.

This holds true for all so that if corporations or the government want to save (ie, run a surplus) then households will have to dissave an equal amount. The government runs a persistent deficit because of households’ propensity for saving.

An important distinction though is that households and corporations are constrained in the levels of deficit spending they can maintain, due to solvency constraints. Sovereign governments on the other hand are not. They can have their central banks set the rate at which they borrow artificially low or even have them directly buy government debt with newly printed money through quantitative easing, which is what we’re seeing now. A form of partial MMT that’s becoming more acceptable amongst mainstream policymakers.

When a government runs a large deficit it’s essentially adding financial wealth to the private sector, both corporations and households are then forced to “withhold” that wealth. On an individual level, the private sector can choose to consume (ie, spend the wealth), invest in the creation of a new asset (ie, build a new home), or save (ie, invest in financial assets). The mix of these decisions determines the Keynesian multiplier that results, which is the additional dollars in spending/income created by every dollar of fiscal.

But, at the aggregate level, there’s going to be an amount of withholding in the private sector that’s equal to that of the government’s deficit. And that withholding is going to eventually find its way into financial assets. Here’s Livermore explaining why:

To summarize the point, fiscal injections are market injections. Over time, they send financial wealth “into” financial markets, where it can bid on assets. This point holds true even when the injections are spent, because spending tends to migrate into savings over time, particularly in economies such as our own that exhibit high levels of income inequality and that offer limited opportunities for profitable new investment.

The higher the level of fiscal spending the greater the level of income/savings in the private sector. This drives corporate profits up as one person’s spending is another’s income. And it forces increasing amounts of wealth into financial assets.

This is just one significant way in which fiscal spending drives markets. Another is through the portfolio preference channel.

Over time, the government’s fiscal spending accumulates on the balance sheets of savers/investors in the form of cash and treasury bonds. This raises the level of cash and bonds investors hold relative to their level of equities. So if investors receive a 5% increase in cash/bonds in their portfolios through fiscal injections, their 60-40 asset mix then becomes 55% equities and 45% cash/bonds.

This means that investors will be forced to buy 5% more stocks just to maintain their desired asset mix. This point is significant. Investors have to buy risk assets — no matter if cities are burning or COVID is forcing wide-scale lockdowns — if they want to simply maintain their original market exposure.

Now consider that with real yields on UTS’s deeply negative in combination with a Fed that is determined to keep rates low and lean into reflation. Investors are almost certainly going to want to increase their allocation to stocks since cash and bonds return less than nothing. And knowing that there’s some level of fiscal spending at which inflation eventually rises, equities become even more attractive on a relative basis, despite their heady valuations. This is TINA write large.

I’ve been writing for months about how bearish investors were too focused on the rampant speculation and high sentiment/positioning metrics. These of course aren’t things you’d like to see when long a bunch of risk. But they’re only one piece of the puzzle.

What bears had failed to see was twofold (1) the new wealth that was being injected into markets due to rising fiscal spending and (2) a lack of a “normal” response from yields in light of the rise in stocks… the effective governor on the market was broken and there’s been no alternative for that new wealth to flow into other than stocks.

So that’s where we currently are… In an environment that’s ripe for rampant speculation… where we have all the ingredients to make the wild days of the dot-com bubble look like a modest snooze fest…

And putting personal politics aside, the Dem win in Georgia is literally the best thing that could have happened for markets when viewed in this fiscal framework.

Biden has just enough of a majority to pass large stimulative measures but he’s working with thin enough margins in both the House and Senate that aggressive changes to tax policy are unlikely, especially when we’re still under the weight of COVID and fighting off very high unemployment.

Of course, something will eventually kill this goldilocks for bullish speculation. That something is inflation.

At some level of fiscal spending (no one knows exactly what level that is), we’ll see consumption outpace the economy’s ability to meet that level of spending. As a result, prices will rise. This will further be exacerbated by the cyclical effects that a falling US dollar, being driven lower by our fiscal policy, will have on the prices of inputs (commodities).

That’s unlikely to become a problem until at least the 2nd half of this year and probably not until 2022. I’ ’ll be writing about inflation and how we should think about it going forward in a follow-up piece.

Until then, keep your head on a swivel….

Your Macro Operator,

Alex