“I view monetary policy as being modestly restrictive, although somewhat less so than before our recent actions… The labor market remains solid overall, but we’ve seen some signs of cooling in recent indicators.” ~ John Williams, FOMC

Summary: The primary trend in equities remainsup, but the short-term picture continues to deteriorate, warranting a cautious stance as further risk-off is expected. The Dec FOMC will be a make-or-break moment for the market, with a hawkish surprise likely driving a more significant selloff in risk assets. While we’re keeping the book light on risk, we’re willing to play for tactical swing longs in oversold names, such as BTC.

***The MO port is up +32% ytd, and we’re not seeing a shortage of great opportunities in this market. If you’d like to join me, the MO team, and our Collective of sharp, supportive investors and traders as we navigate these markets, then click the link below. I look forward to seeing you in the group.***

Join The Collective

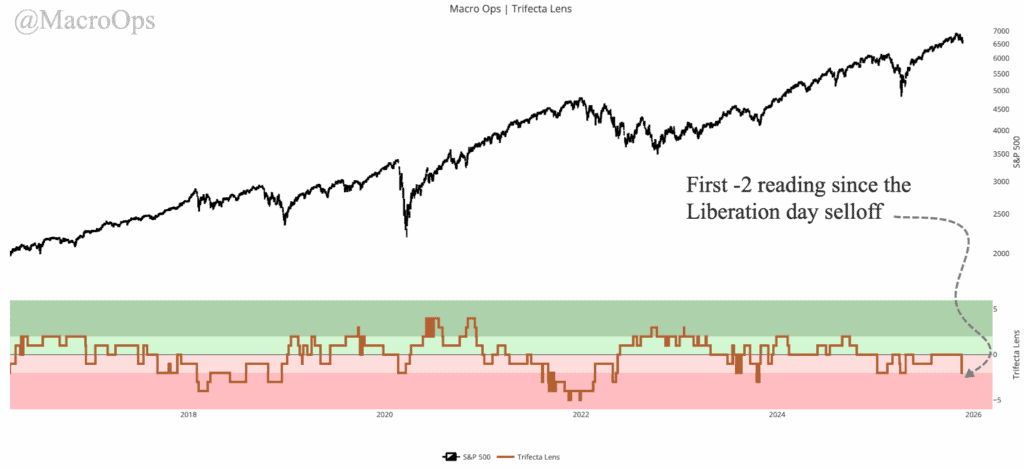

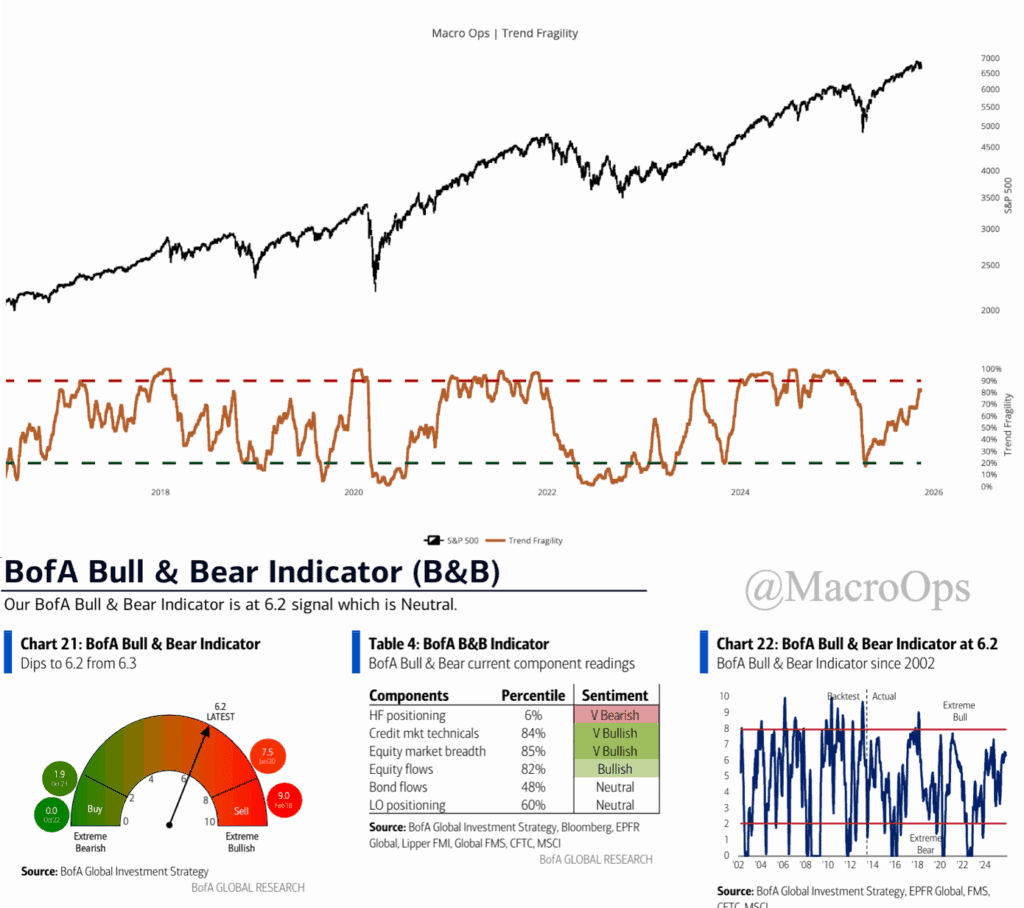

1. Our Trifecta Lens Indicator, a composite of technicals, breadth, internals, sentiment/positioning, and liquidity, fell to -2 last week. Anything below zero points to a bearish regime, with continued chop and volatility and downside risk.

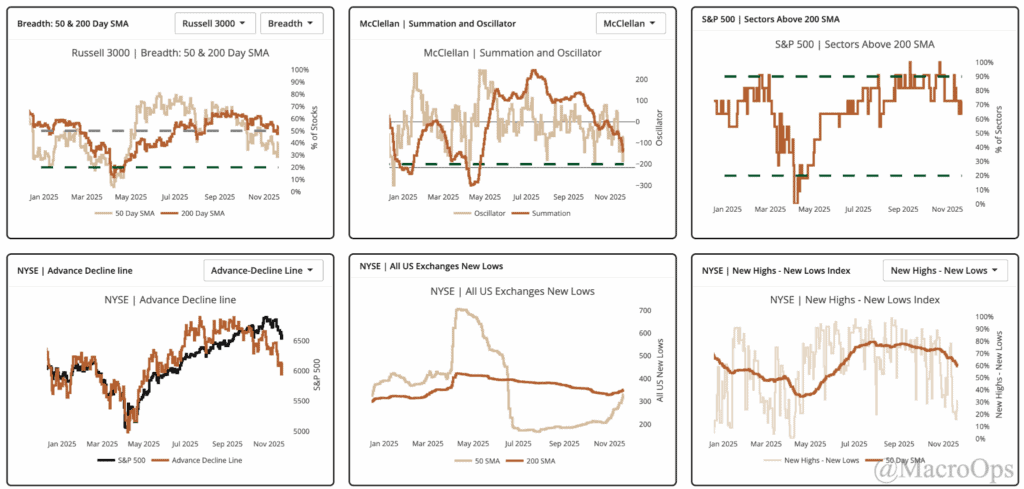

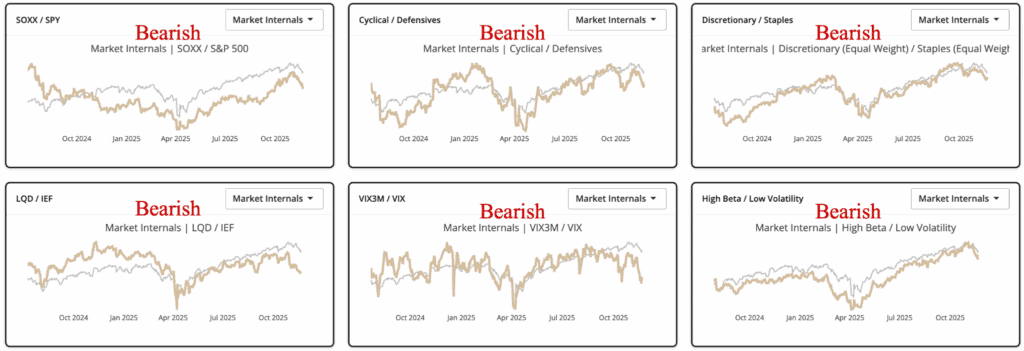

2. The most immediate reason to remain cautious of this market is breadth, which continues to deteriorate but remains above contra deeply oversold levels.

3. Internals confirm this picture as well. Each of our key internals continues to trend lower.

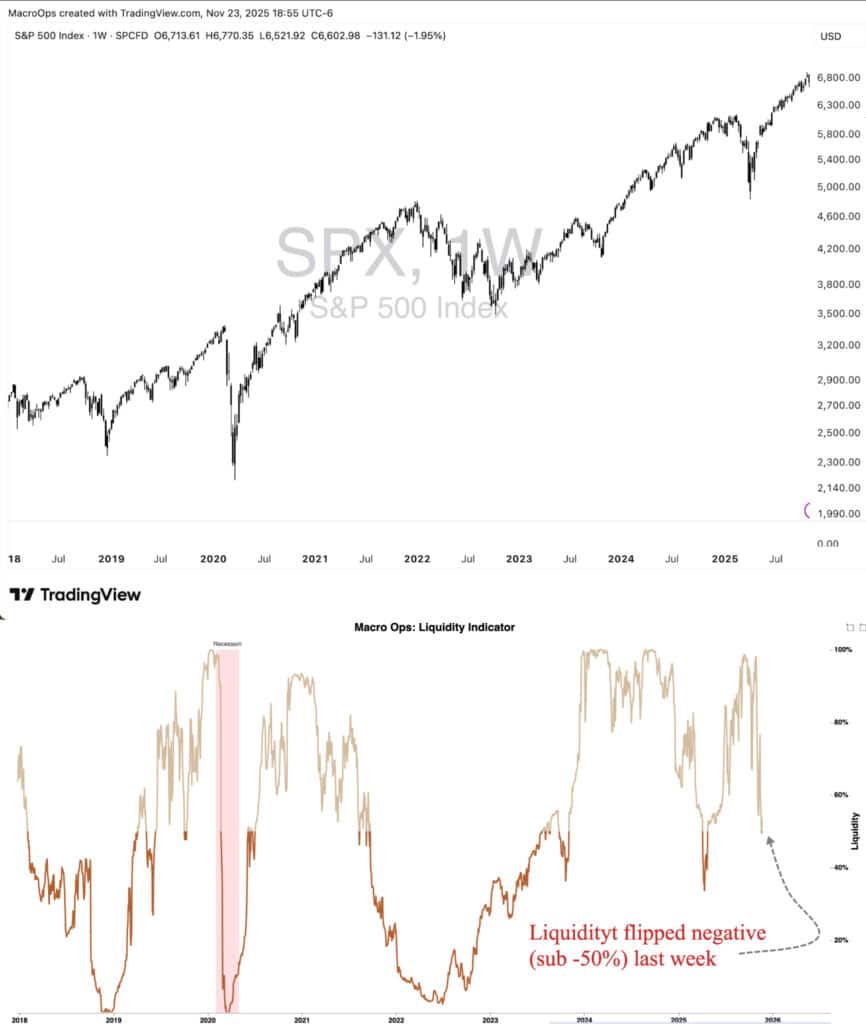

4. While liquidity continues to weaken… Our liquidity indicator flipped negative last week for the first time since the Liberation Day selloff.

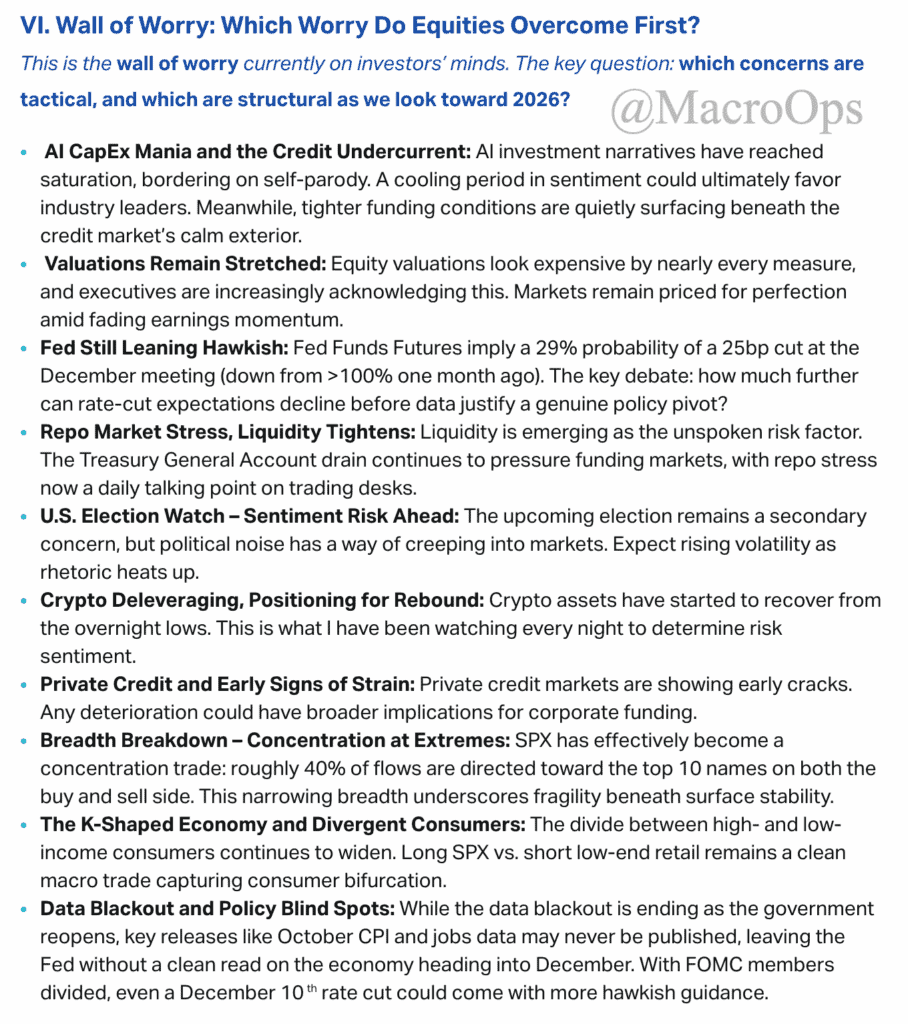

5. Citadel laid out what they see as the primary concerns amongst investors today. The short- to intermediate-term picture has become increasingly muddied over the past month, in large part due to the government shutdown-induced stress in funding markets, the subsequent data blackout, and, more recently, a number of FOMC members coming out surprisingly hawkish over the past two weeks, putting a Dec rate cut in question.

6. Meanwhile, the broad sentiment/positioning picture remains too optimistic considering the recent weakness in the tape. This tells me there’s a real risk of a Dec FOMC upset and a more material selloff should the Fed not deliver.

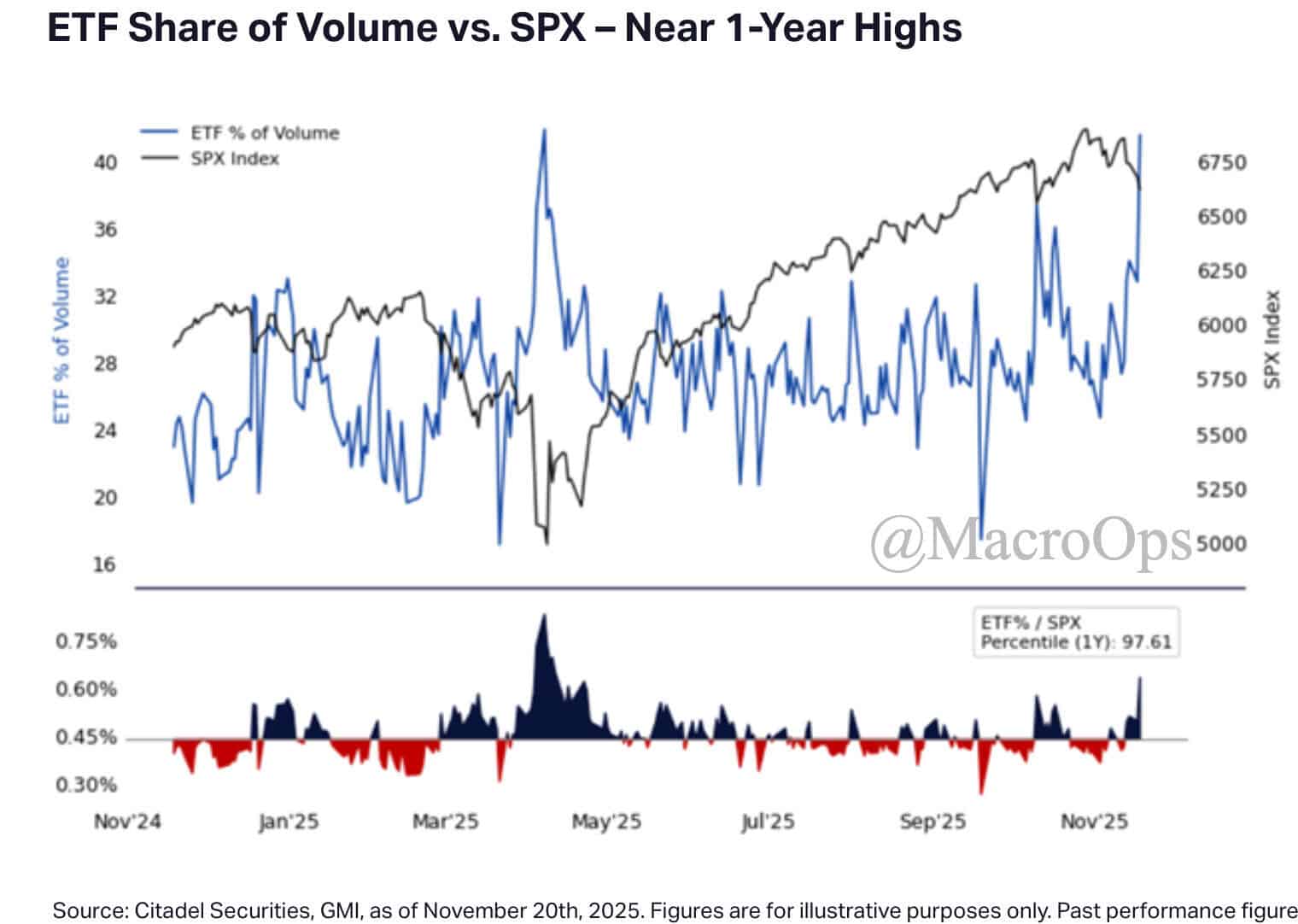

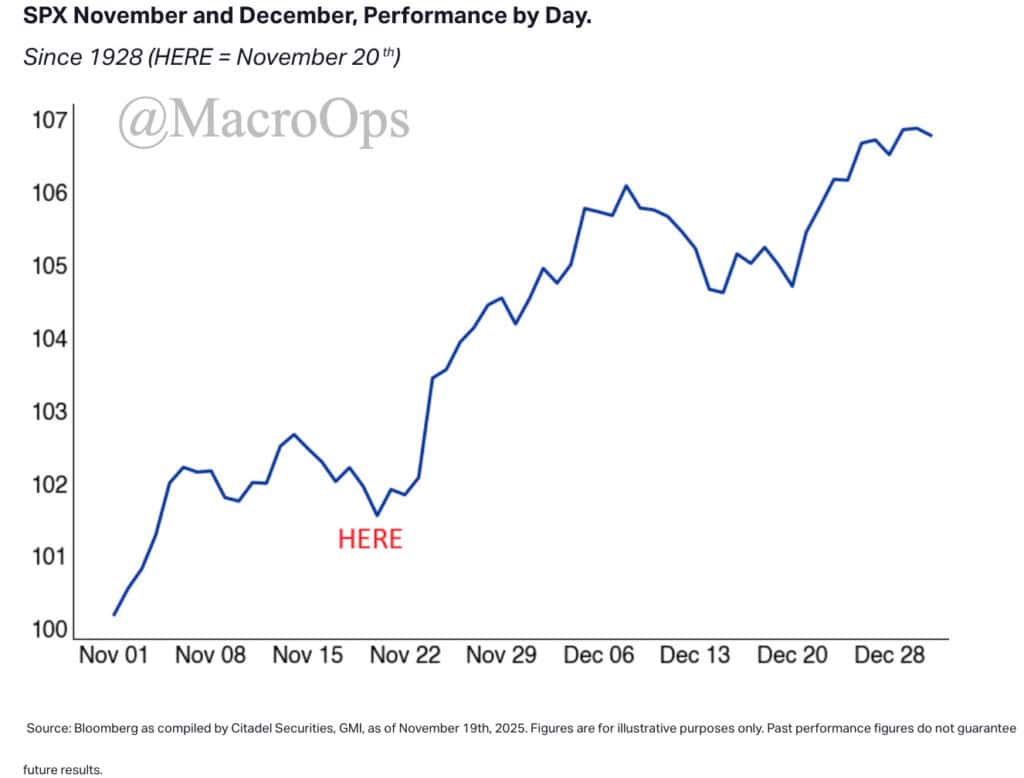

7. On the positive side of the ledger, we’re in a very strong seasonal window over the next two weeks. And with markets oversold, we could see some strong short-term rallies (chart via Citadel).

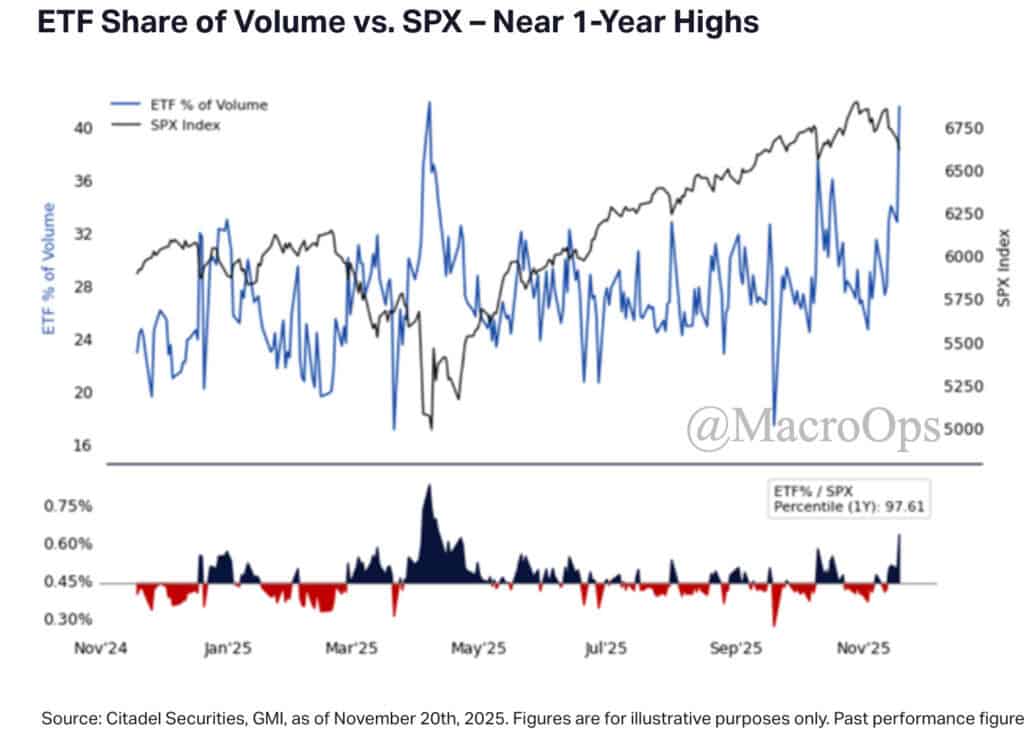

8. This from Citadel also gives weight to the potential for a short-term bottom. They write:

“ETF Trading given our market execution presence: On Tuesday, ETFs represented 41% of total equity volumes — well above the 28% YTD daily average and approaching levels last seen on April 7th (~42%). Elevated ETF activity suggests active hedging of both gross and net exposures. This ranks in the 98th percentile over the past 1-year.

“While gross exposure remains near all-time highs, net exposure has been meaningfully reduced through these hedges — positioning that could unwind quickly if markets stabilize this morning.”

9. Our plan is to keep the book light on risk as we wait for indications of a durable bottom (capitulation triggers, breadth thrusts, a rebound in liquidity, etc…), while playing tactical swing longs when given setups. The BTCUSD daily chart is an example. It’s deeply oversold, with its RSI sub 30%, while it saw a strong reversal off the key 80k support level (grey zone).

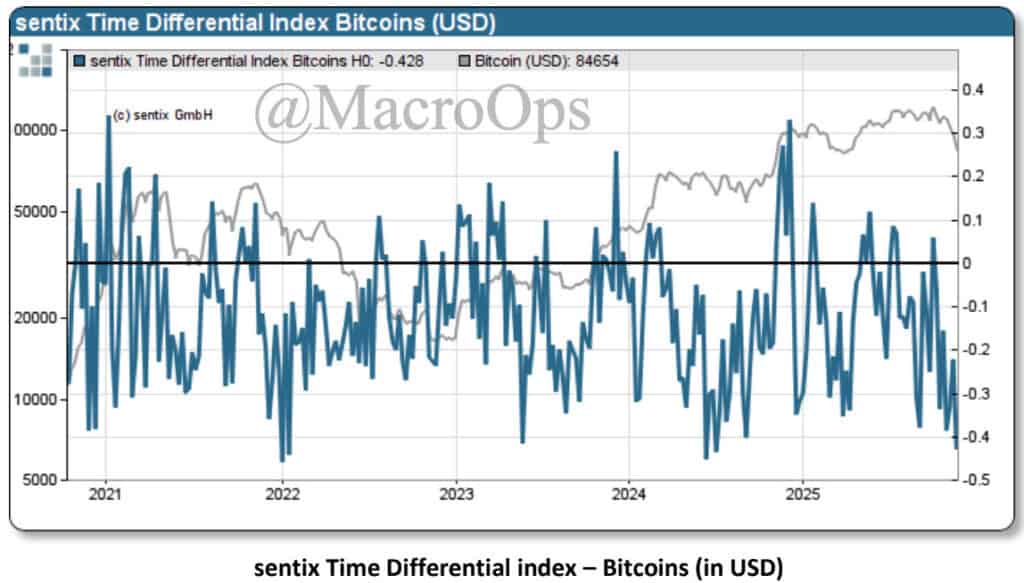

10. Sentix’s Time Differential Index for BTCUSD, which is the differential between Strategic Confidence and short-term Sentiment, has fallen to multi-year lows. Sentix notes that “sentiment is now significantly more subdued at -25 percentage points, almost as bad as it was on 25 August 2023,” which marked a major low.

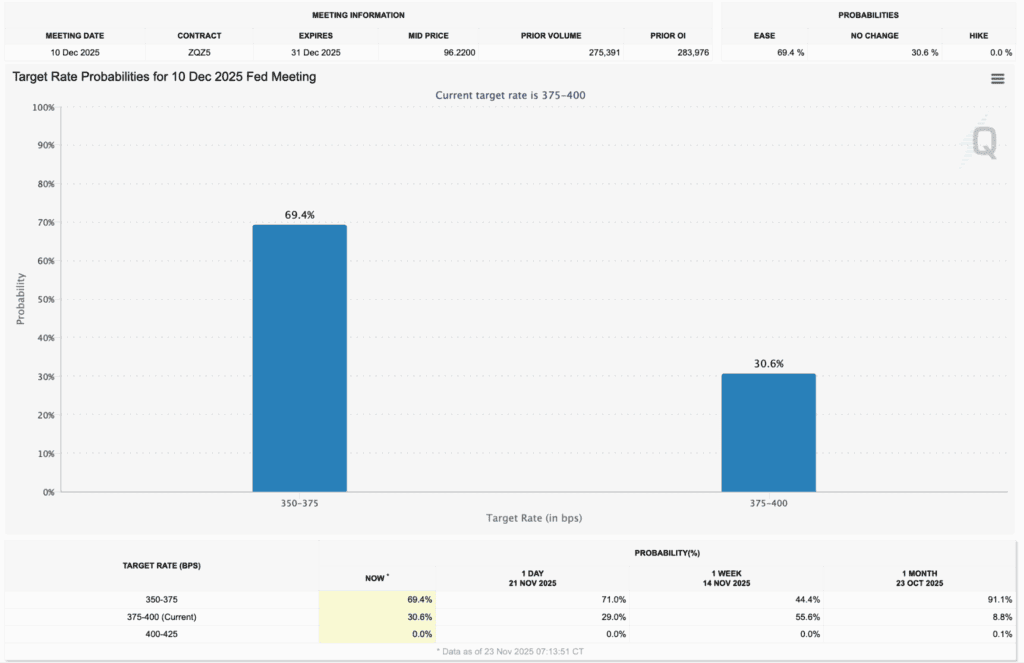

11. The probability of a Dec cut climbed to 70% at the end of last week. I don’t see this dovishness in the Fed’s recent communication. Unless something changes, it looks to me like, at best, we’ll get a hawkish cut in Dec (a 25bps cut with hawkish guidance). We’ll see… The Fed’s communication over the past few months has been all over the place, which has made things difficult. So we’ll just have to adjust fire as things come inbound.

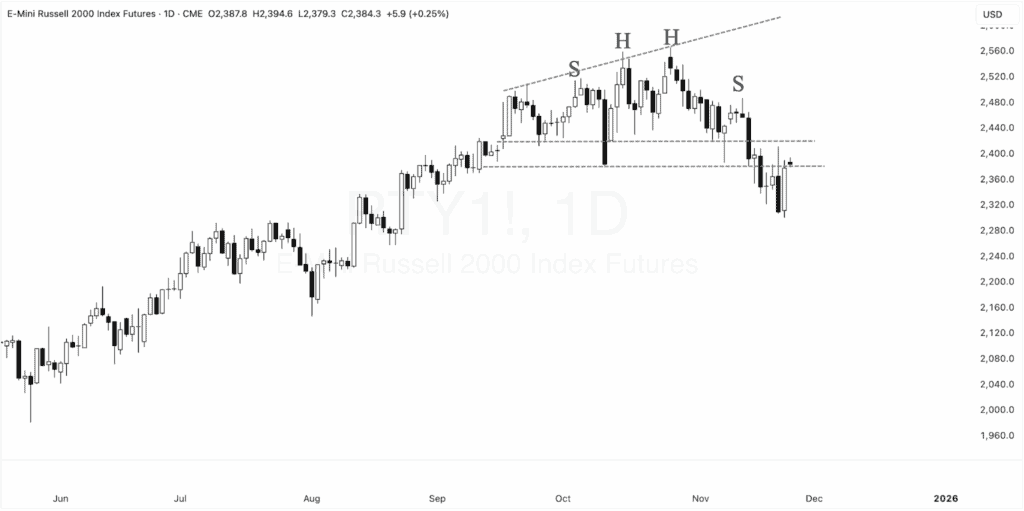

12. I’m considering shorting RTY here on a retest of its upper neckline, depending on how the tape reacts.

Join The Collective

Thanks for reading.