“The current policy stance is still somewhat restrictive, but we have moved it closer to its neutral level that neither restricts nor stimulates the economy. Given this, it makes sense to proceed slowly as we approach the neutral rate.” ~ Philip Jefferson (FOMC Vice Chair) said last week

Summary: The primary trend in equities is still up, but the short-term picture continues to be plagued by poor breadth, internals, and liquidity. We expect continued chop and vol in risk assets over the coming weeks until the Fed addresses issues in the funding markets. BTC’s chart is no bueno, and this large oil producer is setting up for a big breakout.

***The MO port is up +36% ytd, and we’re not seeing a shortage of great opportunities in this market. If you’d like to join me, the MO team, and our Collective of sharp, supportive investors and traders as we navigate these markets, then click the link below. I look forward to seeing you in the group.***

Join The Collective

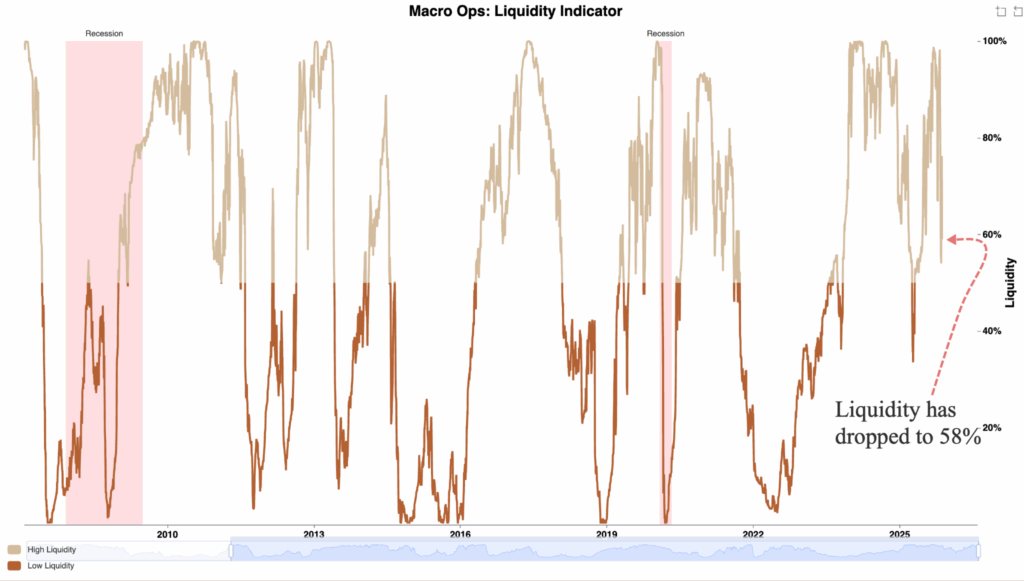

1. The slight volatility we’ve seen in markets over the past month has coincided with a notable decline in financial conditions, as measured by our aggregate liquidity indicator below. It’s now at 58%, which is still positive, though trending in the wrong direction.

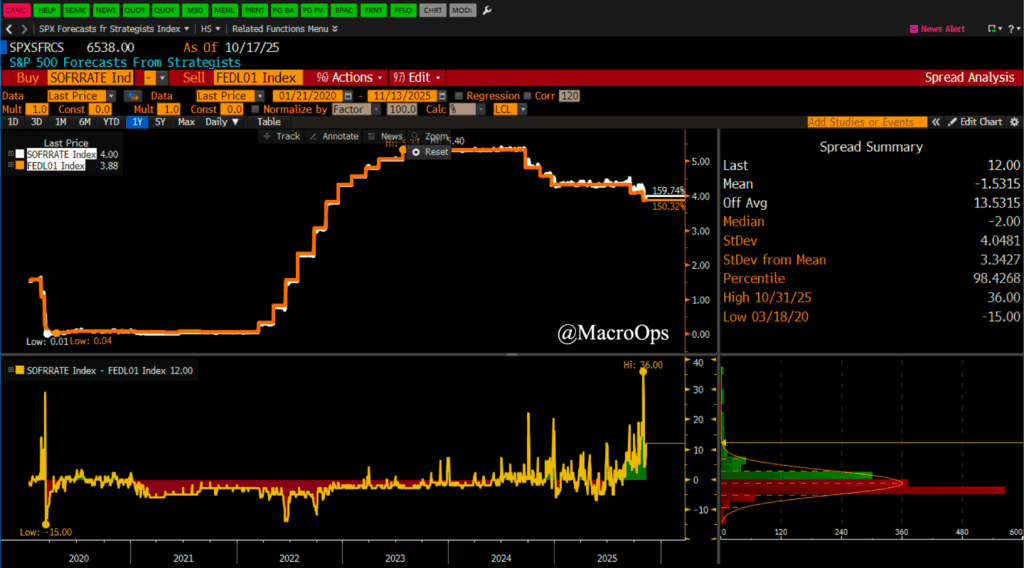

2. There’s an ongoing funding squeeze in the repo market, highlighted by widening SOFR spreads, and due to the government shutdown, rising TGA, and QT draining Fed cash reserves. This liquidity squeeze has tightened conditions for leveraged players and pressured risk assets like BTCUSD. More details below on when this could turn.

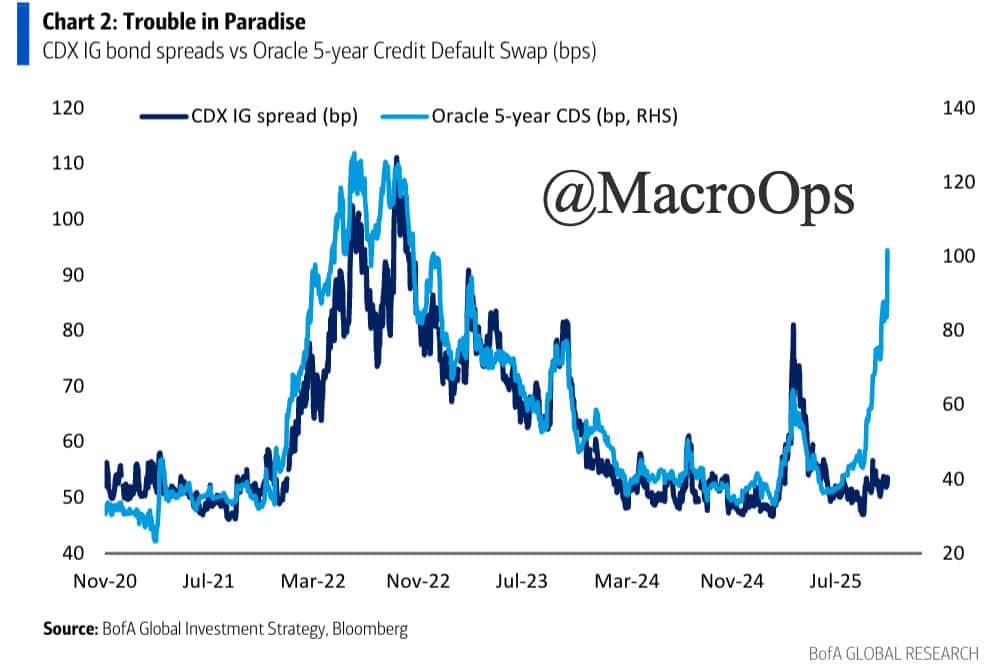

3. This is coinciding with a repricing of AI hyperscaler debt-financed CAPEX spend.

4. BTCUSD completed its megaphone topping pattern this past week. The measured move target for it is 80k. The latest Sentix sentiment data shows investors are relatively sanguine about this breakdown, which isn’t a great look.

5. While we remain bullish on the longer-term trend, I don’t hold much conviction on the short-term path over the next few weeks. Breadth continues to be weak, as well as market internals — though neither is weak enough to warrant significant concern. And I’d hoped to see our preferred measures of short-term sentiment reset on this vol, but they continue to stay elevated.

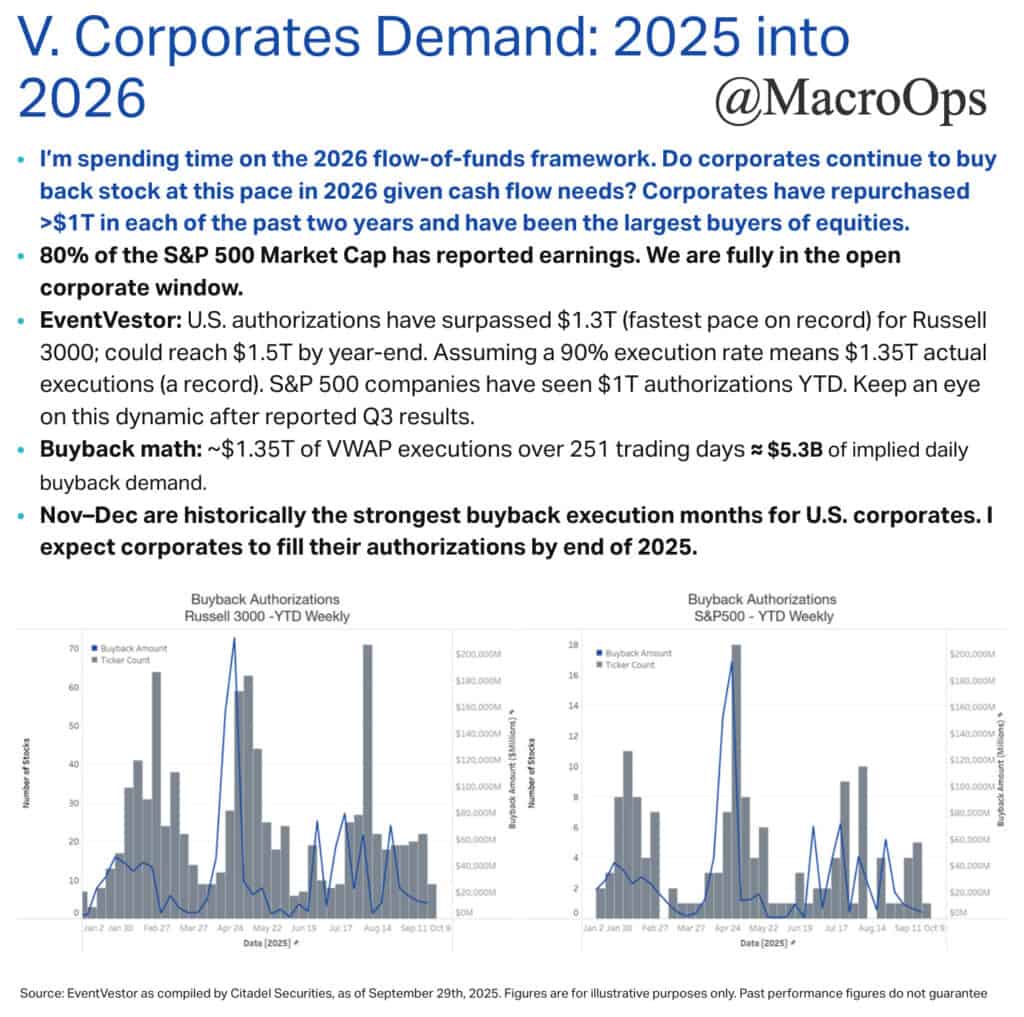

6. The positives are that Buybacks are picking up pace and are expected to provide a persistent structural bid over the next month (chart via Citadel).

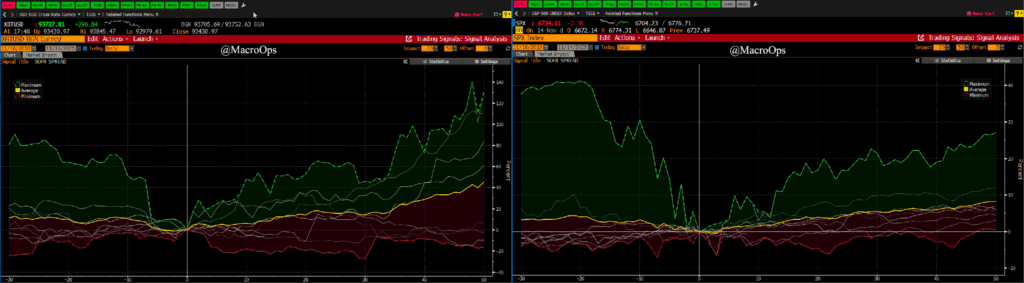

7. The Fed is expected to step in to ease funding market strains next month. With quantitative tightening wrapping up Dec 1, that’s the first positive step — though rising funding stress likely means they’ll need to pivot back to balance sheet expansion (QE) early next year. Markets are watching closely for this shift to manage mounting funding costs. The charts below illustrate that both SPX and BTCUSD typically drop in the month before SOFR spreads widen, then rebound as spreads tighten again.

8. On the bearish side, tight funding markets are draining liquidity and weighing on high-beta assets, while weak breadth and stretched short-term sentiment add pressure.

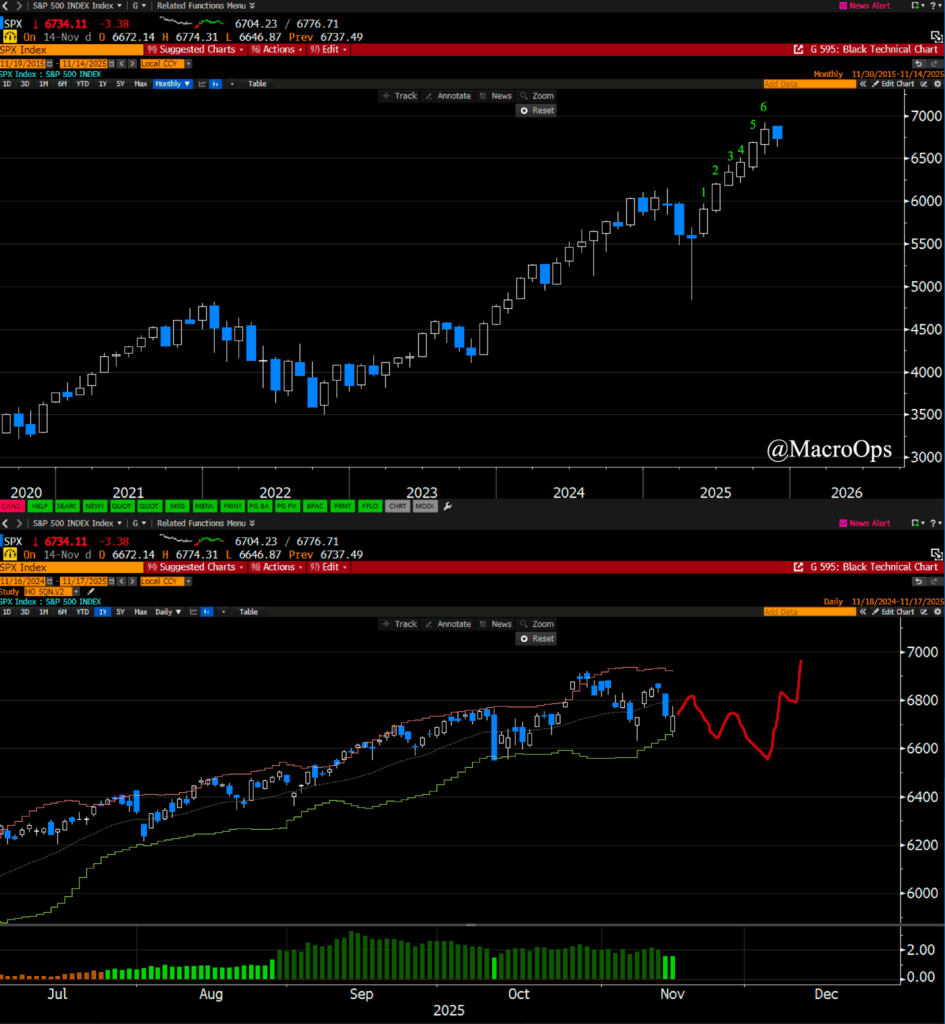

On the bullish side, the broader uptrend remains strong after six consecutive monthly bull bars — historically not a setup for deep corrections—and corporates are still buyers into year-end, with longer-term positioning data showing little FOMO. Taking this all together, expect continued range trading with possible new swing lows near term, but any downside should be limited ahead of a potential rebound by mid-December.

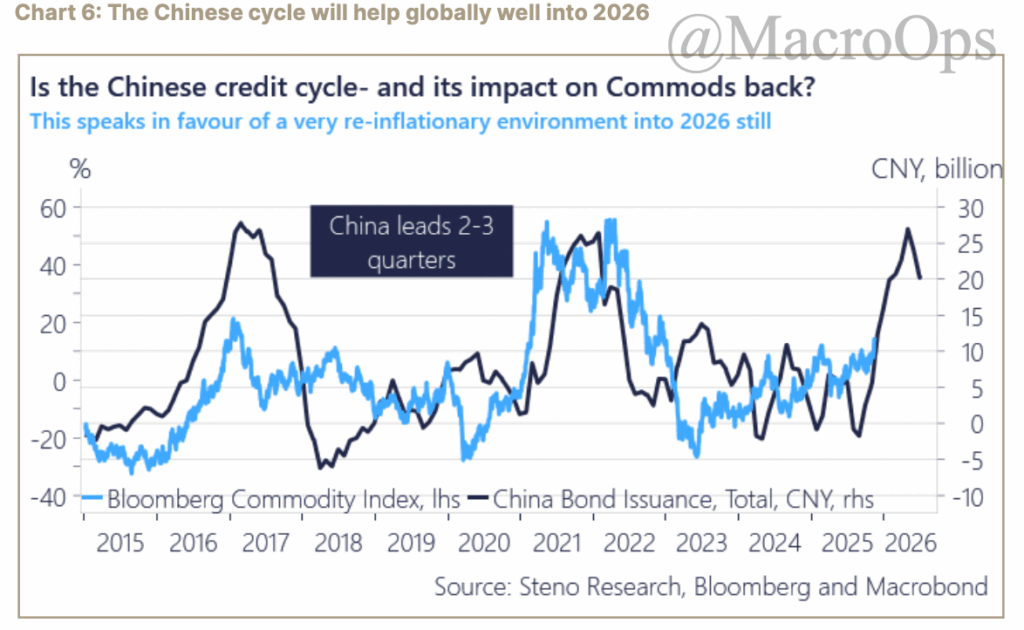

9. We’ve been pointing out the inflection in the global credit impulse for the past few months. Here’s a great chart from Steno Research showing the rise in Chinese liquidity that should begin to appear in the economic data in Q1 of next year (h/t to @JO for sharing this).

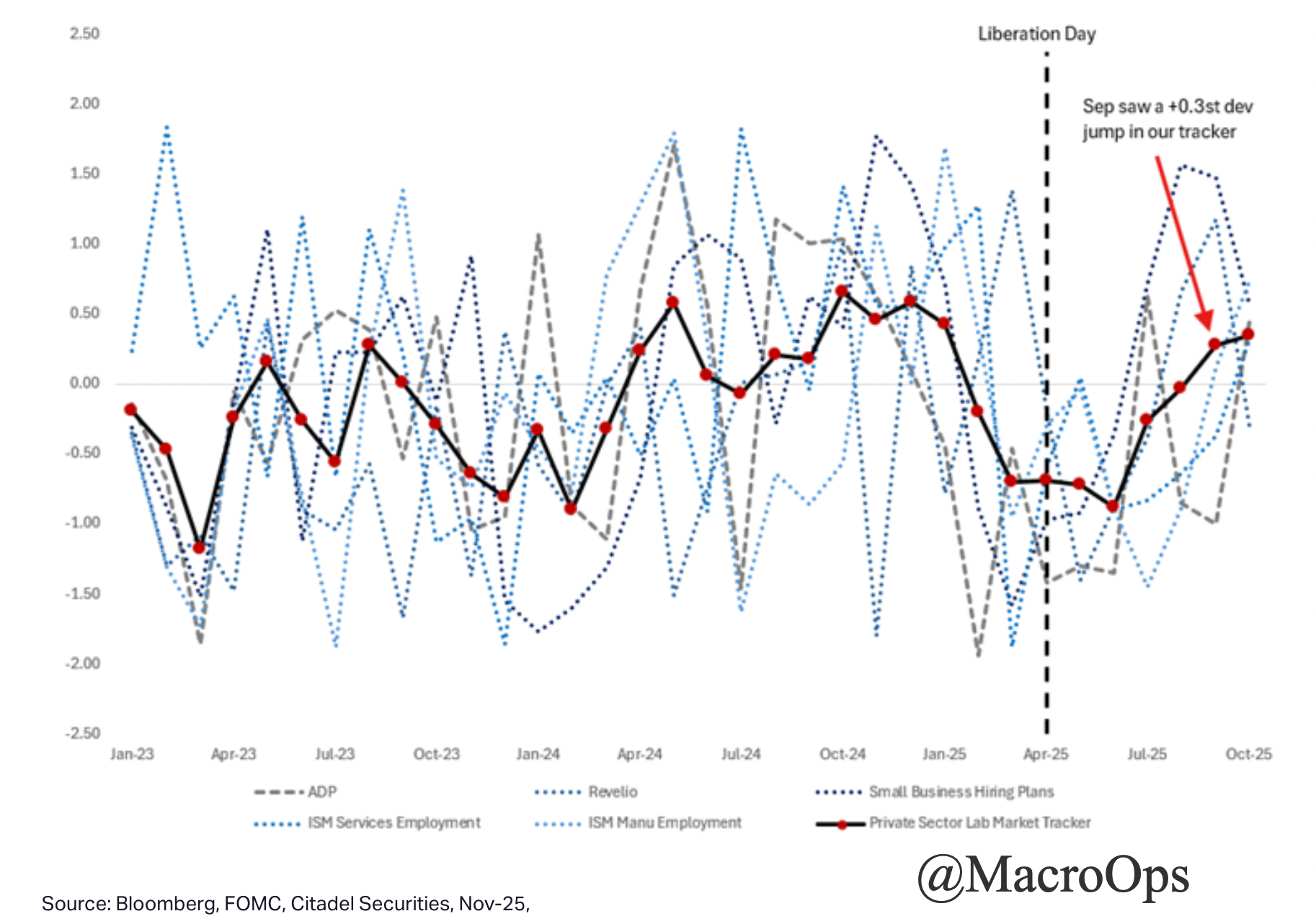

10. Citadel put out a note last week showing their proprietary jobs indicator is pointing to a rebound in the labor market. They go on to argue that recent Fed communications suggest the Fed will stay pat in Dec, which could lead to short-term market vol, though they remain bullish on the longer-term trend. You can read the note here.

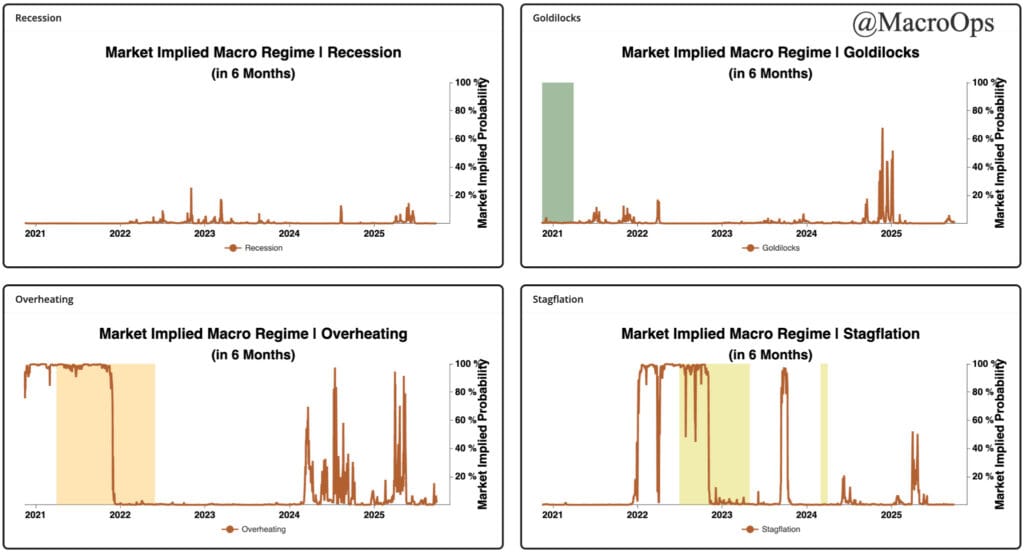

11. Our Market Implied Macro Regime Indicator is neutral across the board at the moment. Though I expect we’ll see the probability of an Overheating regime return in the first half of 26’.

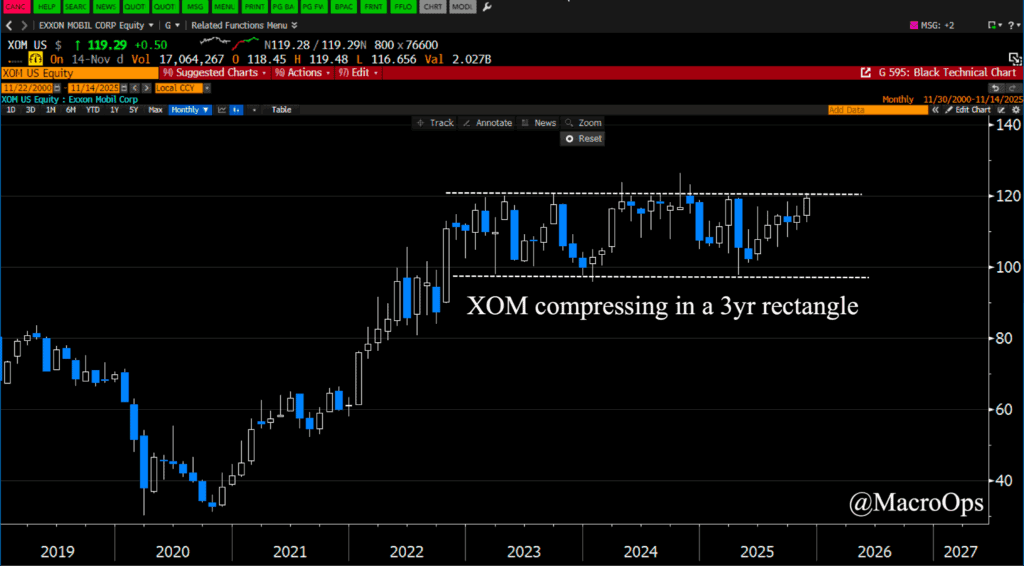

12. XOM just delivered $7.5 billion in Q3 earnings and raised its dividend 4%, underpinned by record oil production from Guyana and the Permian Basin. Capital returns remain robust, with $9.4 billion returned to shareholders last quarter via dividends and share buybacks. The stock is trading in a tight 3-year rectangle. We’re becoming increasingly bullish on oil, and we’ll likely be adding XOM to the book soon.

Join The Collective

Thanks for reading.