We had a lot go down in the value space last week. Remember when I got all excited for Michael Burry being on Twitter? Yeah, that’s gone. Get a load of this:

Damnit, Twitter! For once we couldn’t play nice. We drove the death-metal-listening investor to the hills. There goes my chance of getting him on the podcast!

Anyways — I’m still bitter.

This week we’ve got more Q1 letters to comb through. But before we do that, check out our latest podcast episodes.

Our Latest Podcast Episodes:

Here’s what we cover this week:

-

- Desert Lion Q1 Letter

- Ensemble Fund Q1 Letter

- Upslope Capital Q1 Letter

Let’s ride!

—

April 22, 2020

“Everyone’s Frozen”: Jason Zweig produced (another) jem of an interview. This time he sat down with Buffett’s right-hand-man, Charlie Munger. At one point in the interview, Munger utters the most dangerous phrase in investing:

“This time it’s different.”

How’s it different? For one, companies aren’t calling Berkshire asking for bailouts or sweet 8% preferred stock deals. That’s saying something.

Everyone’s waiting for Buffett to make a huge splash with his cash. What company will he take private? My bet is he’ll buy back a ton of his own stock.

__________________________________________________________________________

Investor Spotlight: Let The Good Times Q1 Letters Roll

GIFs by tenor

GIFs by tenor

This week we feature three more Q1 letters. We’ll start with one of my favorite quarterly reads: Desert Lion Capital.

Rudi Van Niekerk runs Desert Lion Capital. The fund invests exclusively in South African stocks. Unfortunately for Rudi, South Africa hasn’t been the most friendly place for investors. Despite the short-term pain, Rudi is finding incredible businesses trading at ridiculously low valuations.

Desert Lion returned -41.4% in Q1 2020. This lags the JSE All Share Index by 2%.

Cheap Got Cheaper

Rudi notes that although SA equities experienced the pandemic drawdown like the rest of the world — they did so at cheaper valuations. In short, “the cheap got cheaper.”

So what is Rudi buying these days? He mentions five companies:

-

- Balwin Properties

- Stadio

- Cartrack

- PSG Group

- Alviva Group

Balwin Properties (BWN)

Rudi’s Take: “Balwin is the largest listed residential build-to-sell developer in SA, building apartment complexes targeted at the growing middle-income class. Their target market has a current housing backlog of 700 000 units. Balwin is currently adding about 2 750 units per year, with an annual capacity of 5 000. Importantly, their brand has become known and respected in the country for its well-managed quality offerings. As a “cherry on top,” they also have the exclusive domestic rights to the Crystal Lagoons concept, which serves as a major differentiating advantage where they have been installed.”

Rudi’s back-of-the-envelope (BOE) valuation assumes 4,000 units sold by 2024 for 1,91 earnings per share. Adding BWN’s dividends from 2021-2023 gets us another 0,48/share. Finally, Rudi assumes a 7.5x multiple on 2024 earnings to give us 14,30 in cash flow by 2024.

That’s good enough for a 56% 4-year compound rate of return. Not bad.

BWN also trades at a 50% discount to book value with insiders owning 45% of the company. It’s on my watchlist for further due diligence.

Here’s the chart …

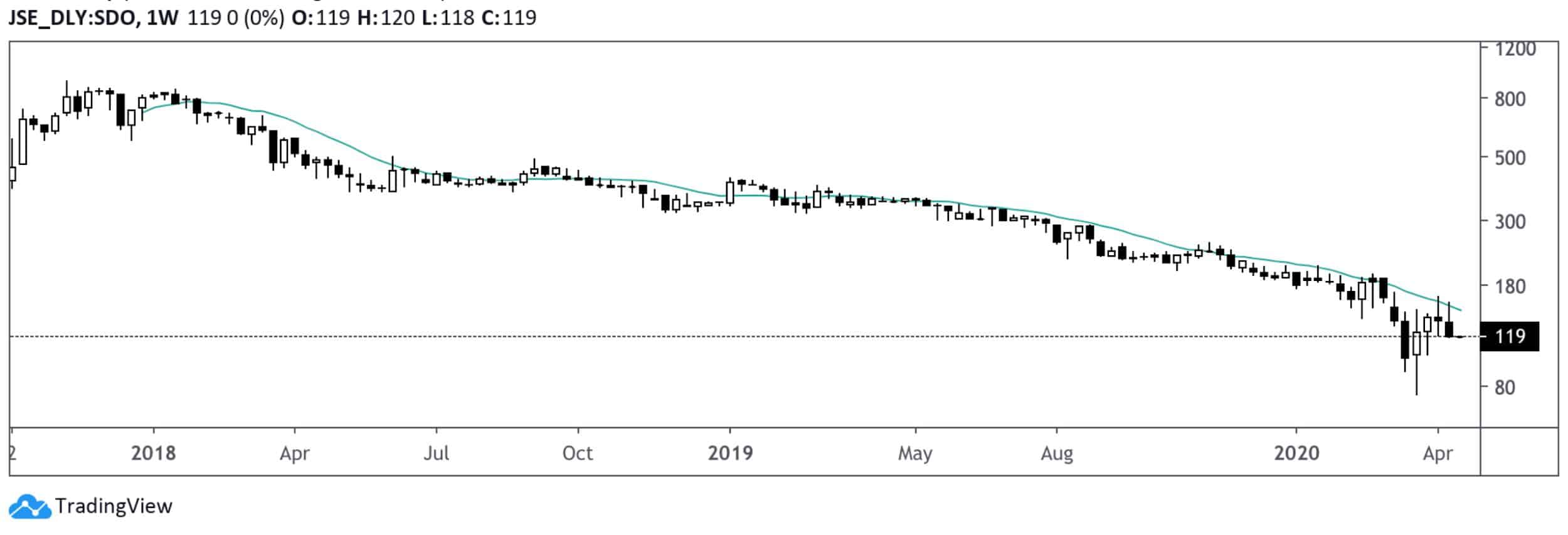

Stadio (SDO)

Rudi’s Take: “Stadio is managed by intelligent fanatic founders and has solid backing in PSG Group as 44% anchor shareholder. They have exceeded all targets since listing 2017 and have set a minimum target of 56 000 students and R 500 million profit after tax by 2026. I believe these targets are very conservative as the demand is just way too high and they will already have capacity for 100 000 students by then, operating on a 20% contact / 80% distance learning split. Earnings are understated as the business is ramping up and they are progressing through the J-curve. The balance sheet is virtually debt-free.”

There’s a few things I love about this investment. First, it’s in the for-profit education industry. There’s a long runway there. Second, their model can scale with 80% of their students learning through distance (i.e., online) education. Finally, I love seeing a near debt-free balance sheet and heavy investment in growth.

Rudi’s BOE valuation assumes 56K students by 2026 and 0,61 in earnings per share. In six years, Rudi believes SDO should command a higher multiple (15 vs. 11). This multiple re-rating would result in 9,17 in earnings to the fund (15 times 0,61).

Under those conditions, that’s a 40% 6YR compound return.

Here’s the chart …

Cartrack (CTK)

Rudi’s Take: “Cartrack is trading at 3 times price-to-sales and 14 PE multiple, which is extremely cheap for a global SaaS company of this quality. The business can continue to reinvest earnings at very high returns on capital and margins will likely expand in the future as the business scales. As a base case, I can see a long runway of compounding at 20% to 30% for many years.”

CTK is a Stolen Vehicle Recovery and Fleet Telematics company. It’s a high-return business in a (to quote Rudi) “winner-take-most” industry.

Check out some of these stats:

- Gross Margin: 67%

- Pre-Tax Margin: 29%

- ROE: 43%

- ROIC: 36%

- Debt/Equity: 0.28x

And for 4x sales? Not bad!

Rudi’s base case valuation gets us 20% CAGR for the next five years.

Here’s the chart …

PSG Group (PSG)

Rudi’s Take: PSG is trading at a -37% discount to its SOTP and -9% discount to its holding in Capitec alone. We are effectively buying Capitec at a 15 PE (28% ROE and growing EPS at >20% annually) and getting all the other holdings (PSG Konsult, Curro, Stadio, Zeder, Energy Partners, Evergreen, etc.) for free. Further, the group has almost no debt.

PSG is an investment holding company with businesses across myriad industries.

Rudi’s BOE anticipates 20% annual top-line growth with “look-through” earnings growiung from 12,60/share to 26,12/share.

At that rate, Rudi assumes a 14.6x exit P/E multiple on 2024 earnings. This gives us 381,53/share in stock price. That’s a 31% 4YR compound annual return.

Here’s the chart …

Alviva (AVV)

Rudi’s Take: “Alviva has conservative debt (17% debt to equity) and is highly cash generative. They are reducing debt further by redeeming higher yield preference shares and repurchasing shares on the cheap. There is pent-up demand for Alviva’s IT products and services in South Africa. Any normalization of the cycle will see a massive rebound in earnings.”

AVV operates in the ICT (Information & Communication Technology) business. They have three segments: distribution, services & solutions and financial services.

The stock trades roughly 2.5x earnings. Rudi’s BOE assumes 2023 EPS of 3,74, dividends worth 0,32 and an 8x exit P/E multiple. That gets us nearly 30/share stock price versus its current 5,30.

_________________

Ensemble Fund: -18.64% in Q1 2020

Ensemble Fund returned -18.64% in Q1 2020. The letter discloses many positions in the Fund, but for length-restrictions, we’ll focus on the following names:

-

- Netflix (NFLX)

- NVR, Inc. (NVR)

- Ferrari NV (RACE)

- Blackline, Inc. (BL)

Netflix (NFLX)

Ensemble’s Take: “So, from our reading, the value of Netflix has gone up tremendously for its users as they stay in and socialize less. In the meantime, with economic pressures on consumers globally, we think it’s reasonable to expect that Pay TV subscriptions like cable and satellite, could see accelerating declines, especially here in the US where that trend has already been in place. This would free up five to ten times more budget than cancelling a Netflix subscription of $13/month. Netflix is more likely to be near the bottom of costs to cut and near the top of services to add in our view.”

NFLX is one company benefiting from the COVID quarantine. The stock recently broke out of a long-term symmetrical triangle pattern (see below):

We actually featured NFLX in our Breakout Alerts service a few weeks ago.

NVR, Inc. (NVR)

Ensemble’s Take: “Rather than owning land, NVR’s long-time strategy has been to option its land, providing it with more financial flexibility when times get tough. Further, NVR had over $500 million of net cash at year-end 2019. During the housing crisis, NVR expanded into new territories and in the coming quarters we expect management to once again capitalize on opportunities to both expand and consolidate share of key markets.”

NVR is a developer of single-family homes and condos. As it goes, NVR usually gets thrown out with the bathwater when homebuilding takes a hit.

But the company has attractive qualities. They’re net cash, trade at 12x earnings and generate 30%+ ROIC.

The current stock price assumes zero top-line revenue growth over the next five years, as well as EBITDA margin compression (from 14% to 12%). Assuming conservative top-line growth rates and stagnant EBITDA margins, we see a path towards $1.2B in EBITDA by 2024.

Ferrari NV (RACE)

Ensemble’s Take: “Given Ferrari’s high average selling price and margins, we believe the company is resilient enough to see through a multi-month period without severe cashflow issues while we expect demand to be fairly inelastic given its long 12-24 month waiting lists across 6 recently launched and limited supply models, all supported by the wealth of its clientele.”

As Ensemble notes in their letter, RACE’s value proposition hasn’t changed. Buying a Ferrari is a status symbol. It’s your ticket into an exclusive club of wealth, sport and taste. There’s natural exclusivity built-in to the car and brand.

It’s why RACE is such an attractive investment during economic downturns.

That said, it’s not cheap by any means. RACE trades near 40x earnings and 25x EBITDA. They have roughly $1.3B in net debt, but their EBIT covers interest expense 23x over.

I’d love to own this company, but not at this price.

Blackline, Inc. (BL)

Ensemble’s Take: “With a 97% customer retention rate and about 110% revenue retention rate, the company’s software is clearly very sticky. But this is a young market and Blackline is the leader, so growth is an important value creation goal. As a result, it rationally invests heavily in sales marketing and R&D to both acquire new customers and grow its footprint of products within its customer base.

We expect that with a recently deepened partnership with SAP in its go-to market strategy, when customers are ready again to focus on faster speed, lower cost, and improved efficiency in the virus’ aftermath, Blackline will be ready to help them do just that with its software solution.”

BL supplies cloud-based software for the management and tracking of repetitive accounting procedures. Most of which revolve around accounting closing.

BL’s a fast grower in this young market. The company averages 30%+ annual revenue growth and 80% gross margins. The company’s losing money on a GAAP basis, but this makes sense given the upfront CAC expense most SaaS companies induce.

Even at 30%/year growth, the company trades at 11x sales. That’s a bit expensive for my taste.

_________________

Upslope Capital: -1.9% Q1 2020

George Livadas’ fund, Upslope Capital, returned -1.9% in Q1. Livadas notes that while some stocks are cheap, others remain significantly overvalued. George breaks down the cheap stocks into two buckets:

-

- Junk stocks

- Quality businesses

Given the prevalence of discounted “junk”, there’s often an urge to load-up on these companies. George warns against such action. He elaborates:

“I think this is mistake, given: (1) the prevalence of value traps (shares appear cheap, but represent ownership of businesses in permanent decline) and (2) the long term benefits of owning steadily-growing and competitively-advantaged businesses with solid balance sheets at attractive prices are well-worth any short-term performance “sacrifice,” in my view.”

Anyways, onto his new positions. Livadas added four new investments:

-

- Evercore (EVR)

- Crown Holdings (CCK)

- Diploma (DPLM.LN)

- Subsea 7 (SUBC.NO)

Evercore (EVR)

George’s Take: “a world-class M&A advisory franchise – that happens to be cyclical – at a crisis-level valuation.”

EVR trades around 7x earnings and 8.4x free cash flow. The last time it was that attractive? 2008.

There’s a lot to like about EVR. It sports a 14% net income margin and generates 30%+ returns on equity. They’ve grown operating income at a 31% 5YR CAGR.

If we assume EVR grows net income 15% total over the next five years we get $341M by 2024. Let’s also assume the market assigns a more normalized multiple on that net income — say 12x. That gives us nearly $4.1B in equity value (~$100/share).

Crown Holdings (CCK)

George’s Take: “A global beverage/food can business that we’ve been both long and short in the past. The vast majority of CCK’s cash flows exhibit modest, non-cyclical growth; and, investors appear to be ignoring potential upside from the typically lackluster food can segment. But, a levered balance sheet has spooked investors.”

CCK is a boring, not-so-high margin business. It’s hard to get excited about a food can manufacturer. But there are some bright spots.

George is right about the leverage. The company has as much debt as equity ($8B market cap with $16B EV). It sports a Net Debt / EBITDA of 4.4x — which doesn’t sound appealing.

Despite the leverage, they generate enough EBIT to cover interest expense 3x over. This is a durable business, and the kind of business you can afford to leverage.

For example, operating margins haven’t changed much in the last fifteen years. So it comes down to revenue and EBIT predictability.

The company’s currently trading at crisis-level valuations (around 12x normalized earnings).

Diploma (DPLM.LN)

George’s Take: Diploma (DPLM.LN) is a U.K.-based specialty distributor. This is an under-the-radar, high-quality business that finally went on sale. “High-quality” is an overused phrase in the investing world (I’m not innocent); but, I think it applies here, given DPLM’s track record of disciplined GDP+ growth, conservative balance sheet, and notable exposure to non-cyclical healthcare markets. “

DPLM is a good business. They sport 30%+ gross margins and 15% operating margins with only 15M euros in net debt.

You can buy the business for 18x EBITDA and 27x free cash flow.

Subsea 7 (SUBC.NO)

George’s Take: “a Norway-based provider of specialized off-shore energy services. Of the four new longs, SUBC could most fairly be tagged with the “junk” label. Fine. Here our bet is that the business has staying-power due to a solid market position, an abnormally strong balance sheet, and a sober-minded management team. If the energy cycle turns, SUBC will be there to benefit.”

Let’s see what George likes about the business.

Like all energy businesses — SUBC is feeling the pain of <$12 oil. Revenues have declined $1.2B over the last five years. Operating income declined $700M during that same time. Ouch.

What would SUBC look like if (and it’s a BIG if) oil recovered? Between 2014-2016 the company generated an average of $880M in operating income. That’s a 57% yield at the current market price if they generate that type of income again.

__________________________________________________________________________

Shipping Chart Update: Base Building Development

GIFs by tenor

GIFs by tenor

Ahh yes, the favorite section for FinTwit’s shipping-stock cohort. Lots of action going on in shipping this week. Let’s take a look at the charts (based on Monday at noon EST):

-

- Scorpio Tankers (STNG)

Disclosure: I am long STNG at an average cost basis of $23.54

-

- Diamond S Shipping (DSSI)

Loving this rectangle consolidation on DSSI and clean breakout.

-

- Dorian LPG Limited (LPG)

If prices hold where they are, that would signal a weak breakout attempt.

-

- Teekay Tankers (TNK)

Flying right above the right shoulder on the H&S top pattern.

-

- Euronav (EURN)

No chart pattern developing

-

- Overseas Shipholding Group (OSG)

Like DSSI, OSG is in the middle of a beautiful rectangle consolidation pattern. Looking for a breakout above its resistance to confirm the bull trend.

__________________________________________________________________________

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!