Most are familiar with the term “pavlovian response”. Here’s a short explanation via Wikipedia:

Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a biologically potent stimulus (e.g. food) is paired with a previously neutral stimulus (e.g. a bell). It also refers to the learning process that results from this pairing, through which the neutral stimulus comes to elicit a response (e.g. salivation) that is usually similar to the one elicited by the potent stimulus.

The idea, now a central part of behaviorism (a school of psychological thought), was first put forth by Ivan Pavlov in the early 20th century. Pavlov trained his dogs to associate the ringing of a bell with the assumption that they were about to be fed. The dogs quickly developed the biological response of salivating as soon as they heard the bell ring, regardless of whether they actually received food.

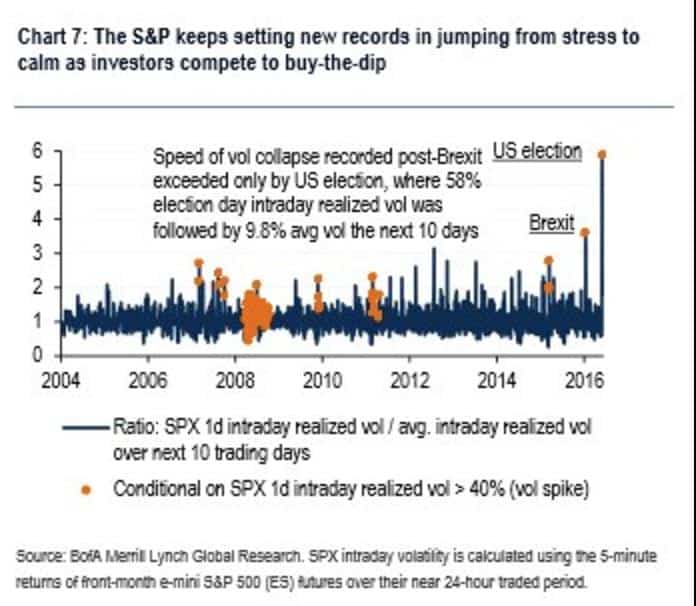

Now look at the chart below:

This chart from BofA shows the market continuing to set new records in both the speed and aggressiveness in which it “buys the dip”.

There’s a strong Pavlovian response occurring here:

- Market Selloff = Bell

- Salivation = Buy Dip

George Soros explained how responses like this, though sometimes short-term positive, are in reality long-term dangerous (emphasis mine).

Every bubble has two components: an underlying trend that prevails in reality and a misconception relating to that trend. When a positive feedback develops between the trend and the misconception, a boom-bust process is set in motion. The process is liable to be tested by negative feedback along the way, and if it is strong enough to survive these tests, both the trend and the misconception will be reinforced.

The last three major market selloffs were caused by important geopolitical events — all having to do with the global populist movement. These events, Brexit, Trump, and the Italian No vote, were all viewed by the market as potentially risky. And even though each resulted in the risky outcome, markets responded with increasingly aggressive dip buying each time.

Now here’s why this is important. The overwhelmingly positive market response to each event signals to the populist movement that protectionism and nationalism are economic positives, while geopolitical unions and free trade are not.

It also serves as a signal to investors of the strength of the market (ie, if Brexit and Trump can’t send the market lower, what can?)

This signalling will likely invigorate the populist movements and their leaders. It’ll push them to be more aggressive in asserting their policies because they see rising prices as validation. This feedback loop between populist politics and markets will strengthen with each dip bought. This means that the more positive the market’s response, the more aggressive populist movements should become.

And that’s where things become a problem. In the long-term, protectionism (ie, trade wars and anti-immigration policies) are economically bad. This is a fact. The world will become a poorer place if we erect barriers to both trade and the flow of people between nations. The last time the world entered a secular protectionist regime was in the late 1930’s. Historically, increasing economic non-cooperation between nations eventually leads to armed conflict.

This brings us to today. We find ourselves at a point where the market and its narrative are becoming overwhelmingly optimistic. This should lead to volatile moves higher in the indices in the coming months. But at the same time, this optimism is sowing the seeds for its own end; as reality diverges from narrative once again, eventually leading to another regime change. Here’s Soros to sum things up:

A positive feedback is self-reinforcing. It cannot go on forever because eventually, market prices would become so far removed from reality that market participants would have to recognize them as unrealistic. When that tipping point is reached, the process becomes self-reinforcing in the opposite direction.

Nearly half the S&P’s revenues come from overseas. Enacting tariffs on imports would result in retaliatory responses. Trade wars first lead to higher prices and then inflation.

Forcing companies to keep manufacturing jobs in the US will raise production costs. Those production costs will be passed through to the consumer in the form of higher prices, which means more inflationary pressures and higher rates. Higher rates means higher financing costs and tighter liquidity.

The bull narrative will go on until these higher rates force the economic reality of protectionism onto market participants. Then this whole self-reinforcing process will then work in reverse. My guess is that this won’t happen until the ten year is yielding between 3.25 and 3.5%. That’s when we’ll need to look out below…

The above excerpt is from the December issue of our Macro Intelligence Report (MIR). If you’re interested in learning more about the MIR, click here.