George Soros was quoted in a speech he gave to the Committee for Monetary Research and Education back in the early 90’s as follows:

Economic history is a never-ending series of episodes based on falsehoods and lies, not truths. It represents the path to big money. The object is to recognize the trend whose premise is false, ride that trend, and step off before it is discredited.

“Falsehoods and lies…,” these are some striking words from one of the greatest traders of all time. It’s also profound insight into how markets really work.

What the Palindrome (his name is spelled the same forward and backwards) is really talking about here is his theory on false trends.

The idea of false trends in markets is predicated on the belief that contrary to common Western thinking, reality cannot be neatly packaged into true and false; black and white.

Rather, Soros believes that reality (and markets) should be classified into three categories:

● Things that are true

● Things that are untrue

● Things that are reflexive

He noted the importance of differentiating between these when he said:

The truth value of reflexive statements is indeterminate. It is possible to find other statements with an indeterminate truth value, but we can live without them. We cannot live without reflexive statements. I hardly need to emphasize the profound significance of this proposition. Nothing is more fundamental to our thinking than our concept of truth.

For those of you not familiar with the concept of reflexivity, go and read our explanation here, it’ll be worth your time.

The benefit of judging truth and untruth on a sliding scale versus fixed one has also been discussed by Nassim Taleb:

Since Plato, Western thought and the theory of knowledge have focused on the notions of True-False; as commendable as it was, it is high time to shift the concern to Robust- Fragile, and social epistemology to the more serious problem of Sucker-Nonsucker.

False trends arise when a dominant belief (what we refer to as a narrative) is founded on untrue assumptions, but the narrative is so strong it moves price action anyway. The false narrative’s effect on the market actually acts to reinforce the strength of the belief that its initial assumptions are correct; thus driving price action further away from reality (what is true) in a reflexive loop. This is how bubbles are created.

Soros discussed the large impact false trends can have on markets in his 2010 “Act II of the Drama” speech. Below is an excerpt and the full text can be found here:

Let me briefly recapitulate my theory for those who are not familiar with it. It can be summed up in two propositions. First, financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. This is the principle of fallibility. The degree of distortion may vary from time to time. Sometimes it’s quite insignificant, at other times it is quite pronounced. When there is a significant divergence between market prices and the underlying reality I speak of far from equilibrium conditions. That is where we are now.

Second, financial markets do not play a purely passive role; they can also affect the so-called fundamentals they are supposed to reflect. These two functions that financial markets perform work in opposite directions. In the passive or cognitive function, the fundamentals are supposed to determine market prices. In the active or manipulative function market, prices find ways of influencing the fundamentals. When both functions operate at the same time, they interfere with each other. The supposedly independent variable of one function is the dependent variable of the other, so that neither function has a truly independent variable. As a result, neither market prices nor the underlying reality is fully determined. Both suffer from an element of uncertainty that cannot be quantified. I call the interaction between the two functions reflexivity. Frank Knight recognized and explicated this element of unquantifiable uncertainty in a book published in 1921, but the Efficient Market Hypothesis and Rational Expectation Theory have deliberately ignored it. That is what made them so misleading.

Reflexivity sets up a feedback loop between market valuations and the so-called fundamentals which are being valued. The feedback can be either positive or negative. Negative feedback brings market prices and the underlying reality closer together. In other words, negative feedback is self-correcting. It can go on forever, and if the underlying reality remains unchanged, it may eventually lead to an equilibrium in which market prices accurately reflect the fundamentals. By contrast, a positive feedback is self-reinforcing. It cannot go on forever because eventually, market prices would become so far removed from reality that market participants would have to recognize them as unrealistic. When that tipping point is reached, the process becomes self-reinforcing in the opposite direction. That is how financial markets produce boom-bust phenomena or bubbles. Bubbles are not the only manifestations of reflexivity, but they are the most spectacular.

In my interpretation equilibrium, which is the central case in economic theory, turns out to be a limiting case where negative feedback is carried to its ultimate limit. Positive feedback has been largely assumed away by the prevailing dogma, and it deserves a lot more attention.

I have developed a rudimentary theory of bubbles along these lines. Every bubble has two components: an underlying trend that prevails in reality and a misconception relating to that trend. When a positive feedback develops between the trend and the misconception, a boom-bust process is set in motion. The process is liable to be tested by negative feedback along the way, and if it is strong enough to survive these tests, both the trend and the misconception will be reinforced. Eventually, market expectations become so far removed from reality that people are forced to recognize that a misconception is involved. A twilight period ensues during which doubts grow and more and more people lose faith, but the prevailing trend is sustained by inertia. As Chuck Prince, former head of Citigroup, said, “As long as the music is playing, you’ve got to get up and dance. We are still dancing.” Eventually a tipping point is reached when the trend is reversed; it then becomes self-reinforcing in the opposite direction.

Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions. Disillusionment turns into panic, reaching its climax in a financial crisis.

The simplest case of a purely financial bubble can be found in real estate. The trend that precipitates it is the availability of credit; the misconception that continues to recur in various forms is that the value of the collateral is independent of the availability of credit. As a matter of fact, the relationship is reflexive. When credit becomes cheaper, activity picks up and real estate values rise. There are fewer defaults, credit performance improves, and lending standards are relaxed. So at the height of the boom, the amount of credit outstanding is at its peak, and a reversal precipitates false liquidation, depressing real estate values.

The bubble that led to the current financial crisis is much more complicated. The collapse of the subprime bubble in 2007 set off a chain reaction, much as an ordinary bomb sets off a nuclear explosion. I call it a superbubble. It has developed over a longer period of time, and it is composed of a number of simpler bubbles. What makes the superbubble so interesting is the role that the smaller bubbles have played in its development.

The prevailing trend in the superbubble was the ever-increasing use of credit and leverage. The prevailing misconception was the belief that financial markets are self-correcting and should be left to their own devices. President Reagan called it the “magic of the marketplace,” and I call it market fundamentalism. It became the dominant creed in the 1980s. Since market fundamentalism was based on false premises, its adoption led to a series of financial crises. Each time, the authorities intervened, merged away, or otherwise took care of the failing financial institutions, and applied monetary and fiscal stimuli to protect the economy. These measures reinforced the prevailing trend of ever-increasing credit and leverage, and as long as they worked, they also reinforced the prevailing misconception that markets can be safely left to their own devices. The intervention of the authorities is generally recognized as creating amoral hazard; more accurately it served as a successful test of a false belief, thereby inflating the superbubble even further.

If nothing else, these words from Soros should impart a deep respect for the complexity of the trading game we play. It should also explain why, like the Palindrome, our approach to markets should start with the full acceptance of our own fallibility, first and foremost.

The occurrence of false trends will only rise as global information and interpretation flow increases and narratives become more uniformed and accordant. Taleb put it well, when he said:

The mind can be a wonderful tool for self-delusion – it was not designed to deal with complexity and nonlinear uncertainties. Counter to the common discourse, more information means more delusions: our detection of false patterns is growing faster and faster as a side effect of modernity and the information age: there is this mismatch between the messy randomness of the information-rich current world with complex interactions and our intuitions of events, derived in a simpler ancestral habitat – our mental architecture is at an increased mismatch with the world in which we live.

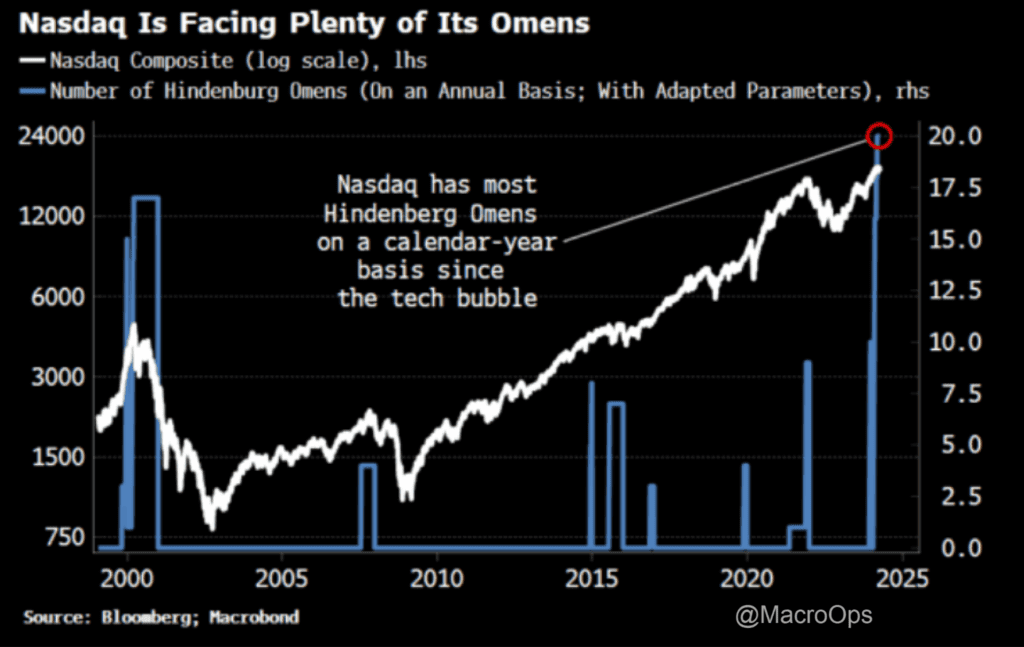

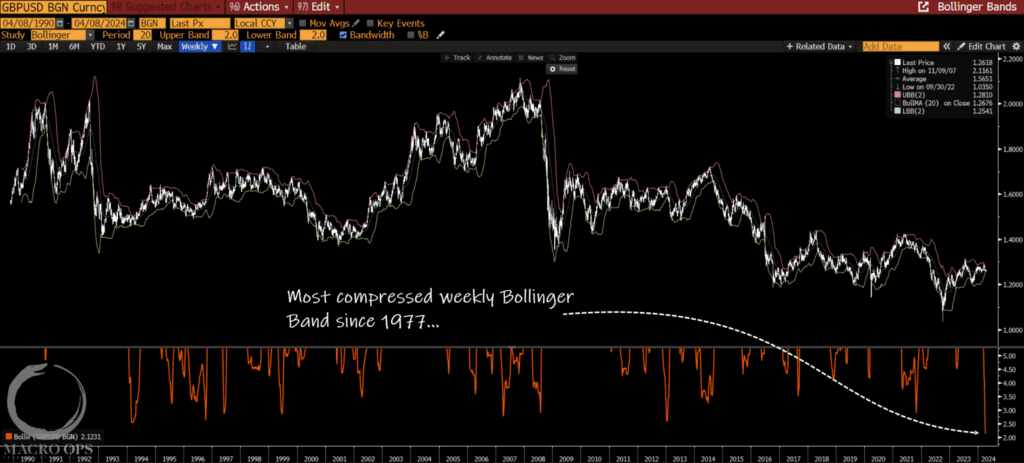

Look around you… do you see any false trends in the markets at the moment?