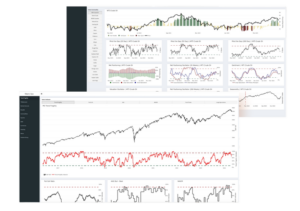

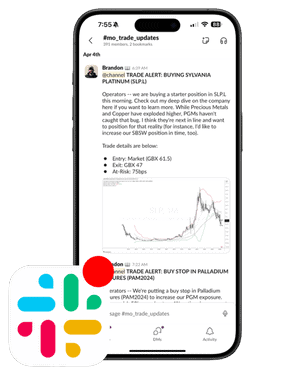

Investment picks are a dime a dozen. And any true Operator in this game will tell you that trade picks are maybe 20% of what matters – and that’s being generous. At MO we eat our cooking, every last bit of it. We run a 100% fully transparent model portfolio with real-time trade alerts, position sizing, exits, profit targets, and all of our day-to-day trade management.