Reflexive processes tend to follow a certain pattern. In the early stages, the trend has to be self-reinforcing, otherwise, the process aborts. As the trend extends, it becomes increasingly vulnerable because the fundamentals such as trade and interest payments move against the trend, in accordance with the precepts of classical analysis, and the trend becomes increasingly dependent on the prevailing bias. Eventually, a turning point is reached and, in a full-fledged sequence, a self-reinforcing process starts operating in the opposite direction. ~ George Soros

In this week’s Dirty Dozen [CHART PACK], we look at 2023 hot takes and Top 10 Trade ideas, pore over the growing body of evidence that we’re in the midst of a significant regime change (from Benign to Vicious), discuss some setups in commodities and small caps, and more.

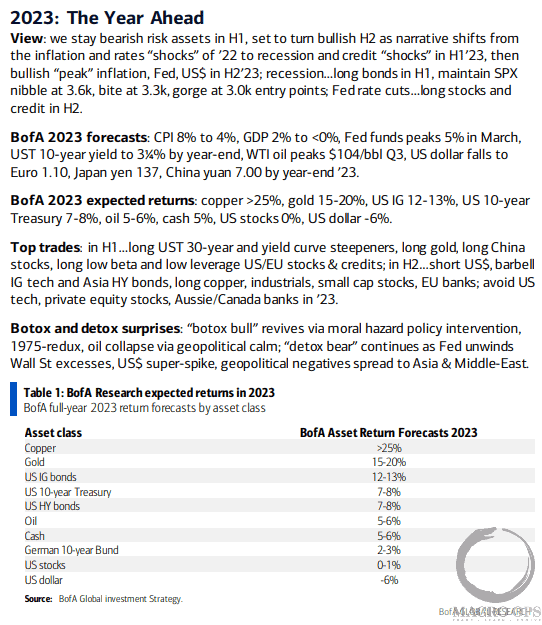

- BofA’s 2023 Outlook summary is below. I agree with much of their take, which makes me uncomfortable. Though I do disagree with them on recession timing. I think it’s an H2 23’ affair, as the Household savings buffer keeps the economy humming a bit longer than most expect.

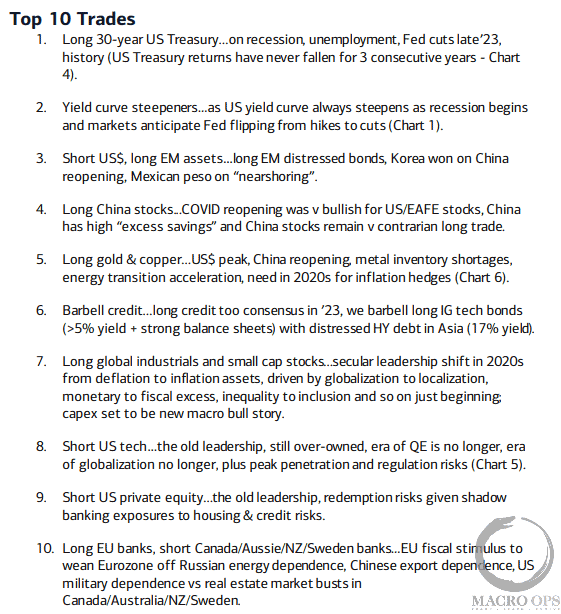

- And here’s their Top 10 Trades for 23’.

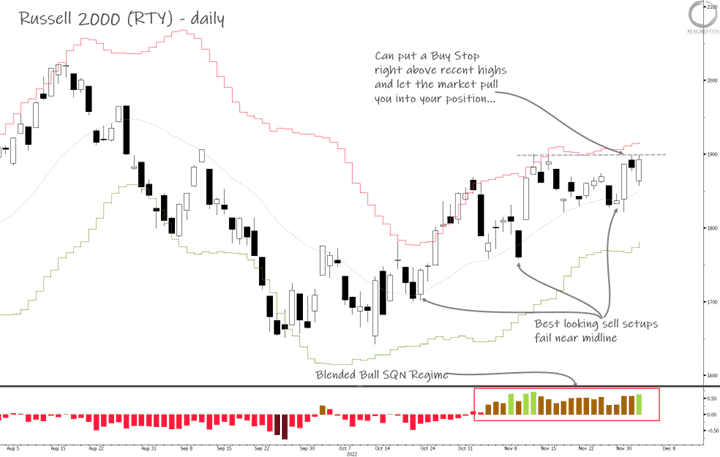

- The chart setup of the week is in small caps (IWM ETF alternative)…

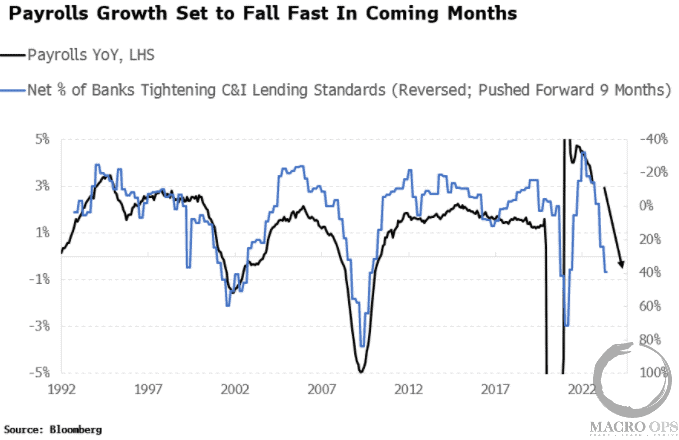

- C&I lending standards are tightening. This metric leads payrolls by about 9 months, which aligns with our H2 23’ recession call (chart via BBG).

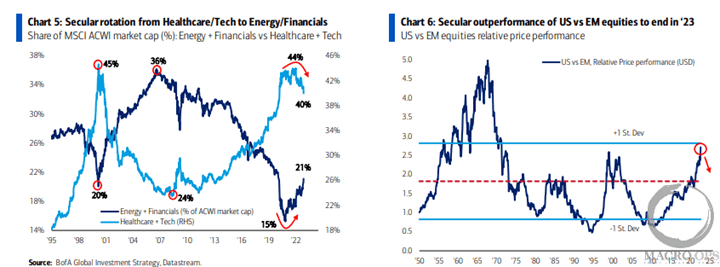

- New secular regimes are just starting. New leaders, new losers, a new game.

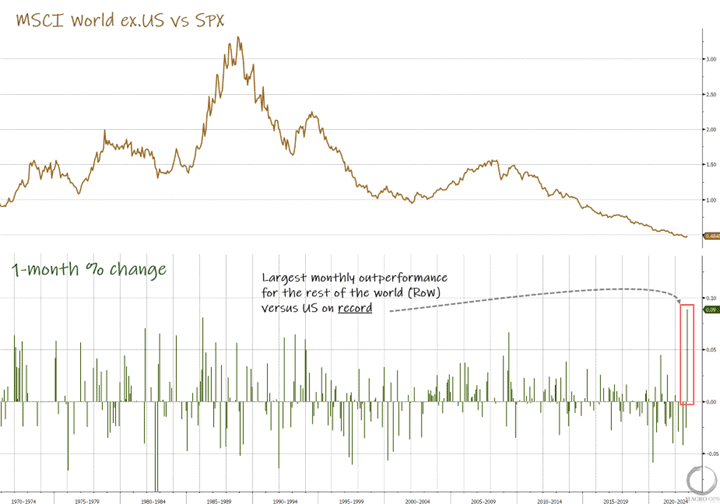

- More signs of a changing regime? MSCI World Ex.US saw its largest month of outperformance against the SPX in November.

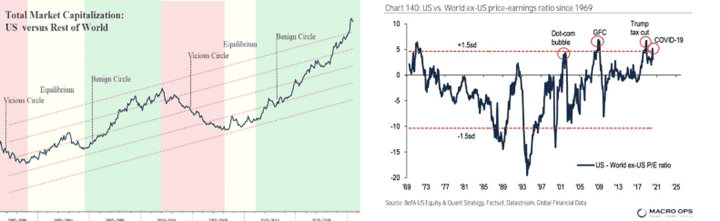

- Capital concentration in the US is near all-time highs. US vs RoW valuations are over 2stdev above their long-term trend. It’s highly likely that we’re transitioning from a Benign circle to a Vicious one. The clip below is from my George Soros Currency Framework piece:

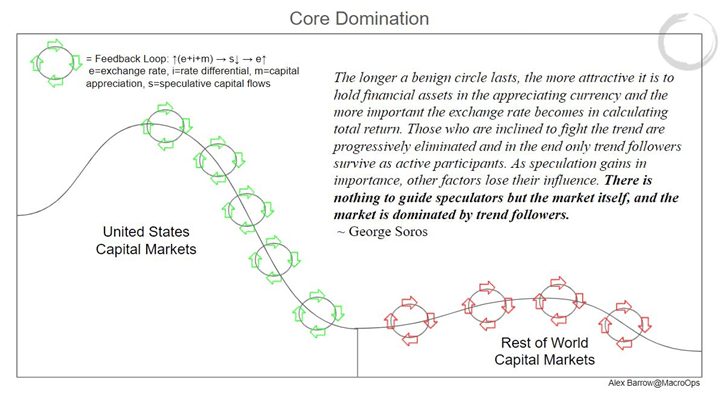

Benign Circles in the US are characterized by low inflation, an easy Fed, a strong dollar, and US outperformance. While US Vicious Circles are marked by above-trend inflation, a weak dollar, and US underperformance.

- And the key to this shift in the secular regime and the ending of Core Domination is, to pull again from my Soros piece:

…The primary thing preventing the dollar from completely tipping over is relative US outperformance, or rather the bullish trend in mega-tech. And this speculative trend that has driven Domination by the Core is itself being driven by stimulus-funded trend followers.

Understanding this, we’ll know the time is ripe for the real start of the USD bear market when the trend in US tech begins to bend — which I suspect will come sooner rather than later. That will mark the extinguishment of the final bullish USD supportive leg and the start of a new regime. One balanced by capital flows back to the periphery (RoW) and a Vicious Circle for the US.

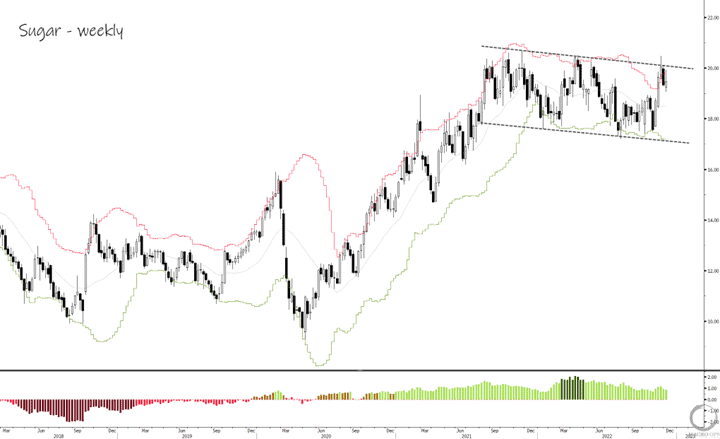

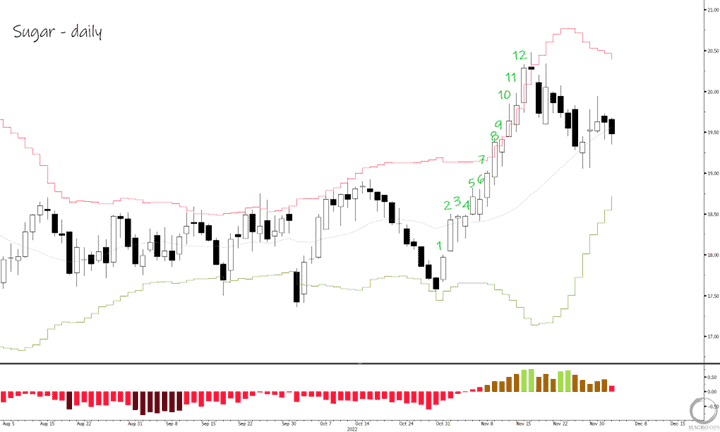

- One trade setup we’re tracking in our Collective this week is in Sugar (CANE is an ETF alternative).

The weekly chart shows sugar is in a 14-month sideways consolidation following a strong 18-month bull trend.

On the daily chart, sugar is consolidating after 12 consecutive bull bars, up near the upper bound of its broader sideways range. The consecutive bull bars show a rare sign of strength, indicating the bulls are in clear control.

The market is working off short-term overbought levels. 3yr OI adjusted Net Spec positioning is neutral, while the short-term delta on that is moving in the bull’s favor. And seasonality turns strongly positive in a week.

Collective members can check out the Commodities tab in the HUD for more details.

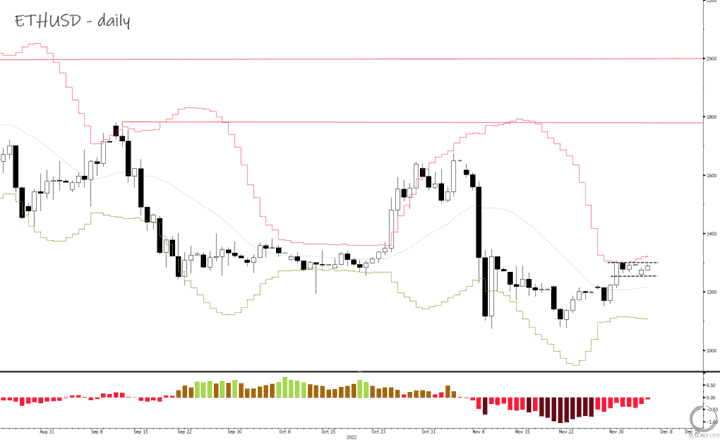

- I’m interested in playing ETHUSD to the long side here on a breakout from its current range. We’re throwing in a Buy Stop right above last week’s highs to see if the market can pull us into the trade.

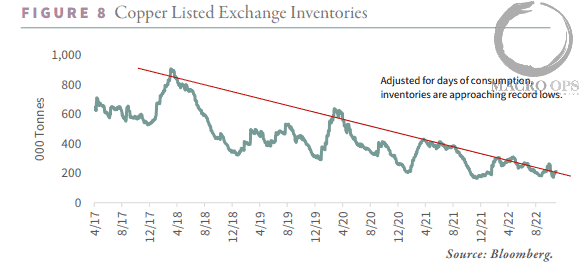

- Goehring & Rozencwajg published their Q3 update on commodities,. Their work is always worth a quick read (link here). Here’s a chart and snippet of their thoughts on copper.

“Chinese copper demand over the last twelve months has strengthened significantly, and bonded warehouse inventories likely met most of the surge. The effects of this are already being felt in the market. China has become more reliant on imports to meet its demand; at the same time, global inventories outside of China are historically low. The Chinese copper market is at its tightest in more than a decade, and traders narrate how commercial users are now paying significant premiums for readily available copper, confirming the market’s tightness.

“An interesting comment in the Bloomberg piece on the developing situation in China comes from the CEO of hedgefund Drakewood Capital Management Ltd: “ The physical market is so tight, it’s like a room full of gunpowder—any spark and the whole thing could blow… without the Shanghai bonded inventory, we are living without a safety net.”

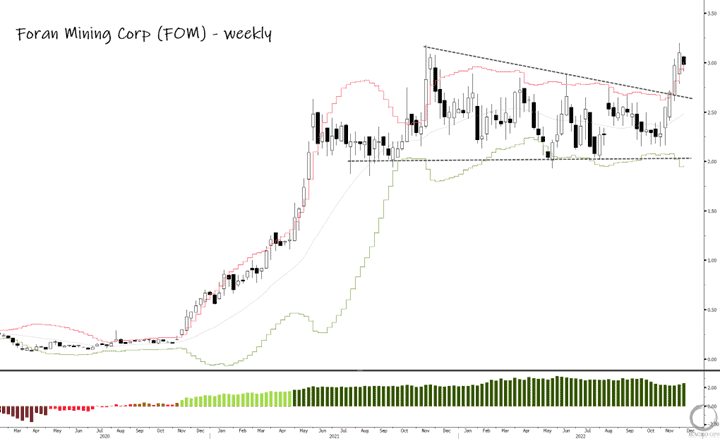

- A more speculative play on this global copper shortage is one of our portfolio holdings, Foran Mining Corp (FOM:TSX).

The chart below is a weekly.

Thanks for reading.

Stay frosty and keep your head on a swivel.