The 3×5 Card Breakdown:

- Brazil has the third-largest pet retail market globally, growing at a 16%+ CAGR in a mostly fragmented industry.

- PETZ is the country’s largest pet retailer with 138 stores, 116 veterinary hospitals, and an unrivaled digital/omnichannel platform

- The company’s size allows it to negotiate lower prices with suppliers, generating more significant customer savings and increased spending.

- Over time, PETZ will open new stores and sell more own-brand products to customers at higher incremental margins (like Target)

- Assuming ~30% 5YR Revenue CAGR, 15% EBITDA Margins, and a 20x EBITDA multiple, the current price represents ~72% upside.

The Brazilian pet market is one of the largest in the world, with strong secular tailwinds. From 2016-2020 Brazil’s pet product market grew at a 13.3% CAGR (the US market grew at a 6.4% CAGR). By 2026, Brazil’s pet products market should grow by an estimated 16% CAGR to R$ 66B.

Petz (PETZ3) is the best-positioned company to capture Brazil’s pet industry boom. Its 138 stores span 16 states and act as local distribution centers for Petz’s omnichannel business. No other pet retailer provides greater value to the customer.

The company offers retail products, grooming services, veterinary clinics, and adoption centers. They’ve even created the world’s first pet-commerce website, allowing pets to shop for toys they want. So far, customers love the experience. Petz boasts a 35% 5YR revenue CAGR with 48% gross margins.

Petz is investing heavily in new store expansion and added 31 new stores last year alone. This growth capex strategy hides its true FCF generating ability. Once at steady-state (i.e., no growth capex), Petz should generate substantial free cash for its shareholders. In fact, we covered this same thesis in our FRAGUA piece, which you can read here.

Consensus estimates signal further 30%+ revenue and EBITDA growth ahead. Despite these projections, the company trades for ~12x our base case 2025 EBITDA estimate, providing 72% upside from the current price, assuming base-case revenue growth and slight margin expansion.

Pet Product Retailing Is A Highly Fragmented Industry

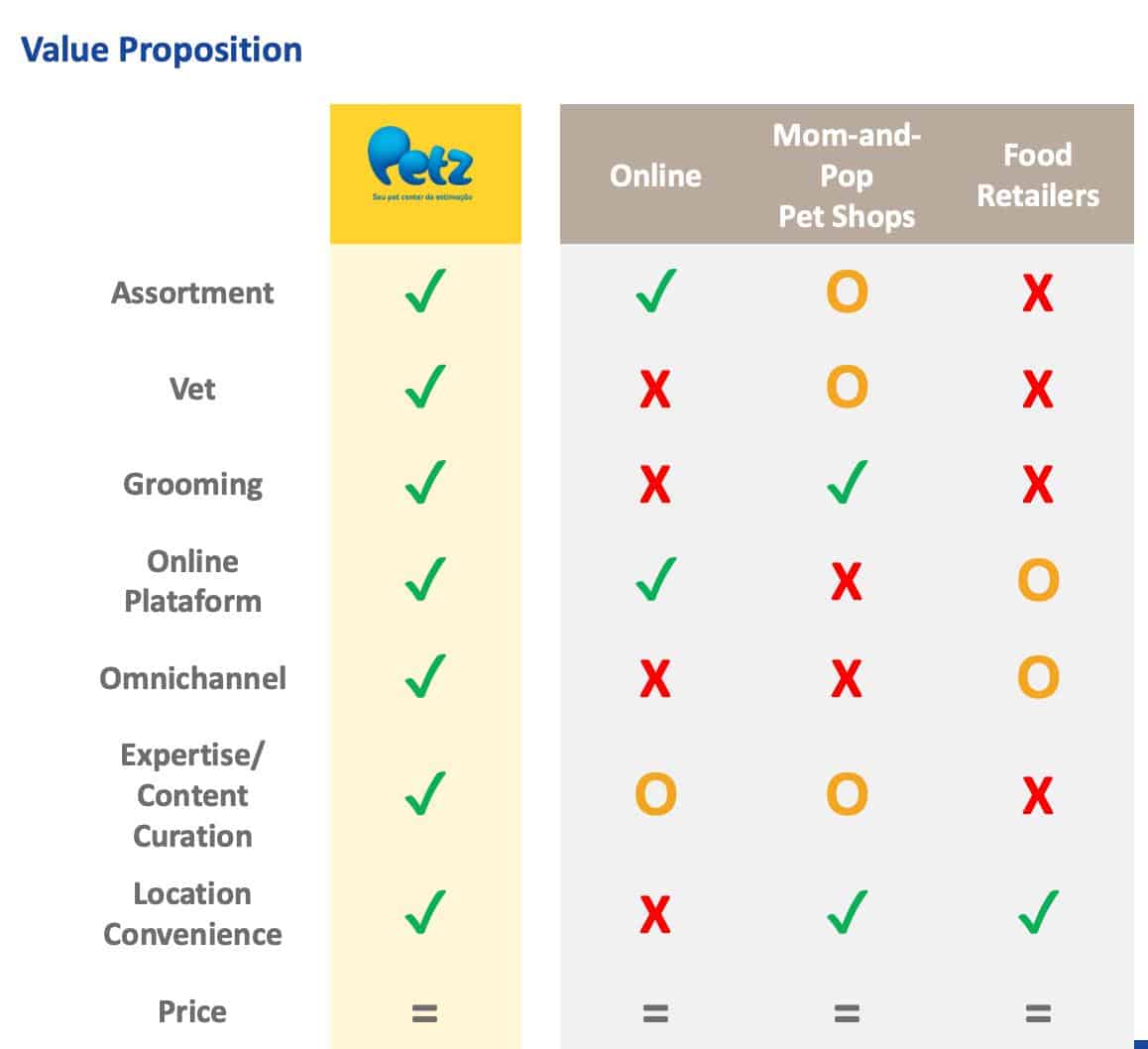

As the third-largest pet market globally, the Brazilian pet retail market is a highly fragmented melting pot of online-only e-commerce stores, mom-and-pop pet shops, and general food retailers. These options meet a few of the customer’s demands. For instance, online e-commerce businesses offer a wide assortment of products on an online platform. Yet, there’s no groomer, veterinarian, or omnichannel shopping option.

In a way, Petz is the best of each fragmented retail subsection. You get the product assortment of a large food retailer, the geographic convenience of a mom-and-pop shop, and the ease of shopping with an e-commerce business.

Petz has two primary sales channels to grow and take market share: e-commerce and general pet superstores. Last year in the United States, 26% of all pet product transactions took place online (up from 19% in 2019). Consumers bought an additional 19% of pet products through pet superstores like Petsmart and Petco.

Brazil’s sales data paints a different picture. In 2020, only 7% of pet products were bought via e-commerce platforms. Moreover, only 11% of pet products were sold via pet superstores.

Said another way, 50% of Brazilians buy their pet products through small pet shops (mom and pop) and veterinary clinics.

Our bet is that Brazilians will buy more pet products via e-commerce/omnichannel platforms over time than anywhere else.

Such a transformation will benefit Petz more than any other Brazilian pet retailer, thanks to the company’s massive mini distribution network and industry-leading digital platform. But before we dive into Petz’s competitive advantages, it’s crucial to examine Brazil’s pet product e-commerce penetration rates. It shows the massive amount of growth still in the pipeline.

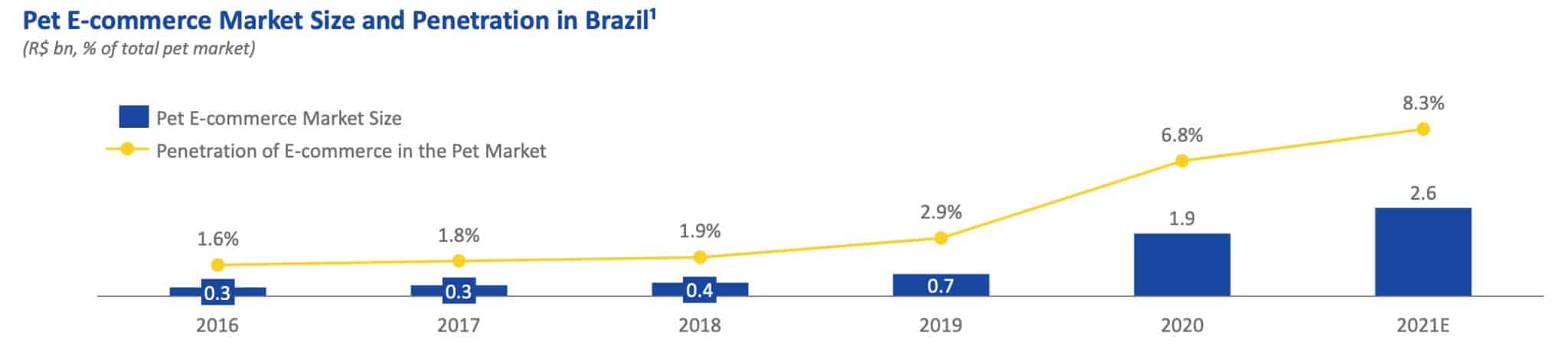

Brazil’s Pet E-Commerce Market: Small But Growing

Brazil is one of the few countries where the penetration of e-commerce in the pet market is lower than the share of e-commerce in retail in general. Take the US, for example, where pet e-commerce represents ~26% of all pet sales (compared to 20.3% retailing e-commerce penetration).

As we mentioned earlier, Brazil sports a 6.8% pet product e-commerce penetration rate. While small, Brazil’s pet e-commerce penetration rate is growing fast. Penetration rates have grown at a 65% CAGR since 2016 and are expected to hit 8.3% by FY 2021.

Looking globally, we find that Brazil trails the rest of the world in online pet product e-commerce adoption. For example, in 2019, Brazil generated ~4% of its pet product sales from e-commerce platforms. The following closest country was the United Kingdom, at 11% of sales.

If Brazil’s penetration rates ever reached that of the US (25%), the country would generate ~R$ 17B in e-commerce pet product sales by 2026.

Petz: The Most Logical Customer Value Proposition

Petz satisfies its customers through three main segments: retail products, veterinary/hospital services, and the digital platform. In short, Petz offers a complete solution for its customers’ pet needs.

The company’s retail product segment offers ~15K SKUs comprising super-premium, premium, standard foods, wet rations and snacks, and non-food items, including hygiene items, medicines, accessories, toys, and clothing.

The company’s retail product segment offers ~15K SKUs comprising super-premium, premium, standard foods, wet rations and snacks, and non-food items, including hygiene items, medicines, accessories, toys, and clothing.

Petz sells these retail products through its Standard, Convenience, and online stores. Standard Stores are usually 1,000m2 in size and house veterinary clinics, animal hygiene centers, adoption centers and carry ~8-12K SKUs at a time.

Then there’s the Convenience Store, which is half the size of a Standard Store, carries between 6-8K SKUs, and focuses primarily on dogs and cats. Petz uses these smaller stores to gain a foothold in less-populated areas where a more prominent Standard Store wouldn’t make sense.

Finally, there’s Petz’s online store (or digital platform) where the company sells its products online through its website (petz.com.br) and its mobile app “Petz.” Petz’s digital platform carries the most comprehensive assortment of products (15K SKUs) with exclusive online/app-only discounts and deals. As of 1Q 2021, digital sales represented 29% of total sales.

In total, Petz generates ~95% of its revenue from pet product sales, with the other 5% from its “Services” business, which includes its Seres Veterinary Clinics, Hospitals, Grooming, and Adoption.

Yet what separates Petz from every other Brazilian pet retailer is its omnichannel sales and distribution strategy.

Petz’s Omnichannel Strategy: Physical Stores Create Digital Multiplier Effect

Founder/CEO Sergio Zimerman built each physical store with the mini-DC model in mind. You can see it in their IPO Prospectus (emphasis mine and translated using online document translator):

“In addition, we will seek greater integration between digital channels and services available in the store, in order to improve the experience of our customers and provide a complete monitoring of the lifecycle of pets. In this way, we intend to capture all possible operational synergies between the physical and digital sales channels, aiming at increasing sales by physical store area, operating stores as effective mini distribution centers, expanding sales via digital channels and improving of the relationship actions with our customers.”

We saw the same strategy in our last company deep dive, Via Varejo. So why is omnichannel important? The platform provides insights into a company’s economies of scale and network benefits.

For example, Petz can command lower prices from its suppliers because it is the country’s most extensive pet retailer. The result is lower prices for its customers and a wider assortment of products. Lower prices and greater choices bring more customers to Petz retail shops and online platforms.

Plus, each incremental DC/physical store translates to a better customer experience, faster shipping times, and lower freight costs. In fact, Petz now offers Express and Super Express delivery, so pet parents receive packages within two hours or a few minutes, respectively. As of 1Q 2021, 85% of Petz’s sales come via its omnichannel platform.

The company’s also noticed a multiplier effect with new physical store builds. According to its Institutional Presentation, digital sales increase by multiples when a physical store opens in a new region.

Customers love Petz’s digital platform. The company’s mobile app ranks #1 in the pet sector on Apple and Google app stores. Its website generates 790M+ monthly active users.

Petz’s Growth Levers: New Stores, Own Brands, & Cross-Selling Services

There are three main growth levers Petz can use over the next decade. First (and most important) is the company’s ability to open new physical retail stores. Physical stores increase not only retail sales but digital platform sales. More stores also equal more distribution centers, allowing Petz to service more customers per location.

To do this, the company takes a hub-and-spoke approach, opening one Standard Store with ancillary Convenience locations.

To do this, the company takes a hub-and-spoke approach, opening one Standard Store with ancillary Convenience locations.

Petz will also leverage its own-brand product sales to bolster growth (think Target’s own-brand product sales.)

Own-brand product growth is vital for two reasons. First, own-brand products reinforce customer loyalty and top-of-mind brand recognition.

In addition to increased customer loyalty and brand awareness, own-brand products are higher-margin items. This makes sense as Petz doesn’t need to pay a middle man (i.e., the supplier) for the goods it produces in-house.

The higher percentage of sales Petz generates from its own-brand products, the higher its run-rate gross and EBITDA margins.

Finally, Petz will cross-sell more of its Veterinary, Hospital, and Other Services to its customers. As we mentioned earlier, Petz’s Service revenue represented a mere 5% of total sales. Cross-selling such services shouldn’t be an issue as Petz does most of these services inside its Standard Stores.

Thinking About Valuation

Petz has experienced tremendous growth over the last five years, increasing revenue from R$ 414M in 2016 to R$ 1,436M in 2020. During that time, they’ve expanded gross margins 700bps, from 41% to 48%.

The company’s estimating 13%, 38%, and 35% revenue growth over the next three years to reach R$ 3.60B by 2023. Let’s assume Petz grows 2024 and 2025 revenue by 30% and 20%, respectively. That gets us R$ 5.6B in 2025 revenue (~2x 2025E EV/Sales), representing a 5YR 30% top-line CAGR.

Next, let’s talk EBITDA. The company’s estimating gradual EBITDA margin expansion over the next three years from 12% to 15% by 2023, generating a potential R$ 541M in 2023 EBITDA. Petz will get there if they sell more own-brand products, shift more sales to their online platform, and build new stores.

Let’s assume the company continues its margin expansion, hitting 22% by 2025.

At 22% run-rate EBITDA margins, Petz would generate ~R$ 1.24B in EBITDA by 2025, valuing the company today at ~10x our estimated EBITDA figure.

Let’s assume Petz can’t expand EBITDA margins after 2023 and gets stuck at 15% for conservatism’s sake. In that case, they’d end 2025 with R$ 842M in EBITDA, or 12x the current EV. A 20x EBITDA multiple gets us to R$ 16.8B in Enterprise Value. Subtract another R$ 717M in net debt, and you get ~R$ 16B in shareholder value, or R$ 41/share (72% upside).

Concluding Thoughts

Petz is the most dominant pet retailer in Brazil. The company benefits from top-of-mind brand awareness, 138 physical retail locations acting as mini distribution centers and a founder whose long-term incentives align with common shareholders.

As Brazil’s largest pet retailer, Petz possesses unfair competitive advantages in lower supplier prices, greater logistics distribution for its omnichannel business, and an unmatched complete service offering for every pet need. The company provides a level of service never before seen in the Brazilian pet retail market.

Finally, pet retail is one of the most durable investable industries. Between 2014 and 2020, Brazil’s retail market stalled, growing at most 1.8% (2017) yet twice contracting 7% or greater (2015 and 2016). During that same time, Brazil’s pet retail market boomed. In 2018 pet retail grew 8.1% and in 2020, a mind-boggling 17.8%.

The formula is simple: Industry-leading business with unfair competitive advantages + durable and high-growth market + aligned founder/CEO = a potentially great opportunity.