Hope you’ve had a great week! We paused our accounting series to highlight our Collective membership service. Doors closed last Sunday. If you didn’t get in but remain interested, shoot me an email.

I know, you missed your weekly dose of accounting knowledge.

But we’re back baby! This week we’re covering Deferred Revenue. It’s an important topic in the age of SaaS business models. If we don’t understand it, we’ll pass on an amazing business.

Let’s dive in.

What Is “Deferred Revenue (DR)”?

Deferred revenue is money a company receives before delivering those goods or services. Think of it like an advancement payment. Like we mentioned above, deferred revenue is common in the SaaS space. But older, more blue-collar industries also use deferred revenue.

Let’s use lawn care as an example. A lawn care company might need a 50% down payment before they even get to your property. They haven’t performed any service, yet have your money.

That’s deferred revenue.

Where Does It Sit on The Financial Statement?

Now it’s time to get into the weeds. Since deferred revenue isn’t “earned” in the traditional sense — we can’t show it on the income statement. So where does it hide? The liabilities section of the balance sheet.

At first glance, that sounds weird. Why should potential income live as a liability? Think about it this way. It’s like an IOU with another company for future services. You are liable as a company to perform those services or deliver those products.

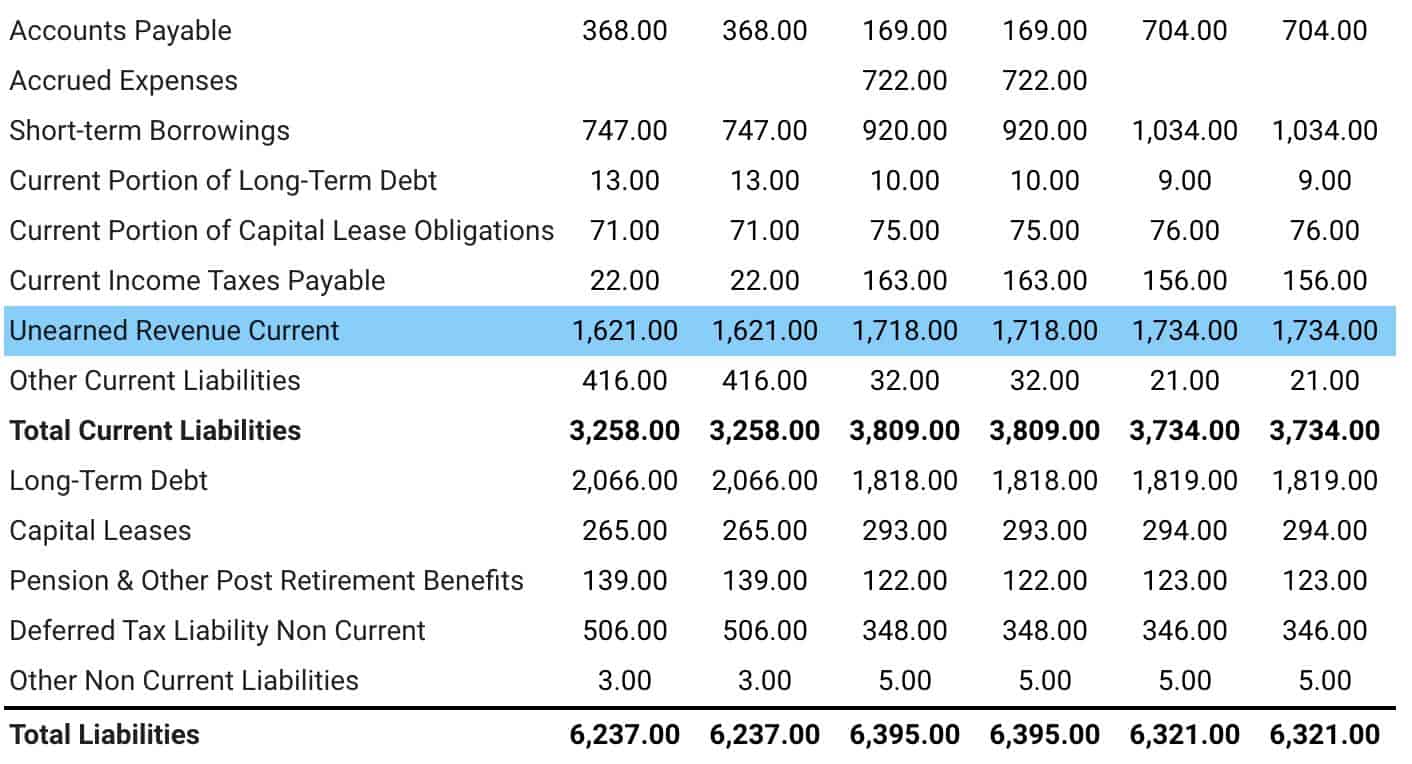

If we don’t, we’ll lose that revenue and face a potential lawsuit. Let’s look at an example of this with a name we’re currently digging into at the Collective.

I’ve highlighted the DR section on the liabilities side (note: also called “unearned revenue”):

Now that we know where it sits, let’s learn why it’s important to track.

Why Should We Study Deferred Revenue?

There’s two reasons we should study this. First, we can plot the long-term growth of a company’s DR. We don’t want a dramatic increase in DR. A high DR balance signals underlying issues. Does the business have problems bringing products to market? Is there something wrong with distribution?

Second, it helps us value SaaS businesses that might show little in current revenues. If we ignore deferred revenue, we could miss a good software business. Accounting for DRe allows us to model what the company may earn once it’s collected on those revenues.

Next week we’ll look at Accrued Revenue.

If you have any questions feel free to reach out.