Hope you had a great week! Last week we discussed deferred revenue and why we should understand it. This week we’re examining its evil cousin: accrued revenue. There’s a lot in common. But here’s the key difference:

-

- Deferred Revenue = job not complete but cash received

- Accrued Revenue = job complete but cash not received

Alright let’s dive in.

What Is “Accrued Revenue”?

Accrued revenue occurs when a company completes a service or delivers a product but hasn’t received payment for that product or service. Let’s use our lemonade stand as an example.

If we sell a glass of $1 lemonade to a customer that promises to pay us tomorrow, that’s $1 of accrued revenue. We’ve completed the task of delivering our goods to the customer. Now we wait for reimbursement.

Why does this happen? You can thank GAAP accounting. GAAP accounting states that a company must recognize revenue at the time it’s earned. Not when the company receives the cash.

This is an important distinction. Most companies perform services and provide goods without accepting the cash up front. Think of manufacturing companies. Usually these companies supply parts and widgets on a Net-30 basis.

In other words, the customer (who receives the widget) has 30 days to pay for that widget.

You might know accrued revenue as another name, accounts receivable.

Mechanics of Accrued Revenue on Financial Statements

Accrued revenue hits the financial statement in two ways: the balance sheet and income statement. As soon as a sale takes place, the company recognizes that sale as revenue on the income statement.

If we don’t receive cash at the point of sale, we have to also record an increase in the accounts receivables account on the balance sheet.

When the customer pays for the goods or service, we reduce that dollar amount on the accounts receivable account and increase the company’s cash amount on the balance sheet.

The Importance of Accrued Revenue

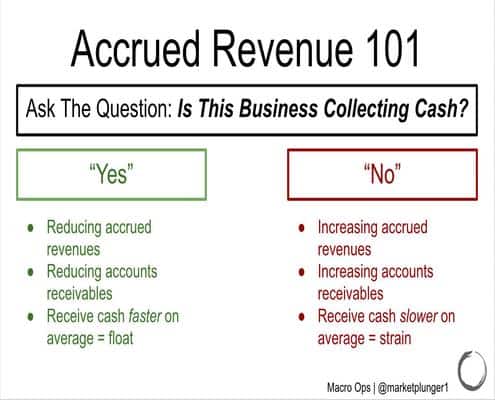

Understanding accrued revs is important because it offers us clues to the underlying health of a business. It allows us to spot cash-flow issues before they reach an earnings transcript or analyst write-up.

Remember: when in doubt, follow the cash

Here’s what you need to know about accrued revenue analysis:

-

- Rising accrued revenues = bad sign

- Shrinking accrued revenues = good sign

Rising accrued levels means the company’s having trouble collecting cash for goods and services it already performed.

Lower accrued revenues means the company’s collecting more cash from goods and services than it’s recording.

We want to buy businesses that reduce accrued revenues over time and avoid those that grow such balances. Doing so will save us a lot of money and stress over time.

If you have any questions feel free to reach out.