Ray Dalio is the founder of Bridgewater. Two years ago, Bridgewater surpassed Soros’ Quantum fund for the title of most profitable hedge fund of all time; returning over $46 billion since inception.

In your author’s humble opinion, Ray Dalio is one of the more original thinkers alive today. In the investing world he stands alone in his depth of understanding of how the “economic machine” works. His “principles” for life and management are like beautiful computer code designed to produce desired outcomes while stripping away the non-essential. The man is a philosophizing engineer taking apart and designing machines for all aspects of life. Dalio has devoted himself to pursuing truth at all costs (I know, it sounds like I’m fawning, but I admire the guy’s thinking. He’s also one of my three favorite traders next to Livermore and Soros.)

It’s this radical devotion to “finding out what is true and what isn’t” that unnerves many and makes Dalio and Bridgewater easy targets for ridicule. The two have been frequent subjects of poor journalism. Recently, a few hack reporters have tried painting Bridgewater as cultish and its founder as an egomaniacal Jonestown leader.

Nothing could be further from the truth. I’ve been lucky enough to spend some time at their headquarters in Connecticut and my opinion is that Dalio and company simply practice what they preach, which is “radical transparency”. Yes, the culture is, well, radically different than anything you’ll find elsewhere and definitely not for everyone. But it’s also completely, perfectly, logical. He refers to the company as an “intellectual Navy Seals”, which I think is a fair analogy.

Dalio has built a machine to produce a desired outcome. That outcome is excellent long-term risk-adjusted returns. There’s no doubting he’s been successful at it… or actually, THE MOST successful at it. Though different, or rather because of this difference, Bridgewater’s unparalleled success is worthy of examination.

With that let’s explore and dissect the thinking and practices of the man who’s built the world’s best money making machine.

On Philosophy and How to Build the Machine to Get What You Want

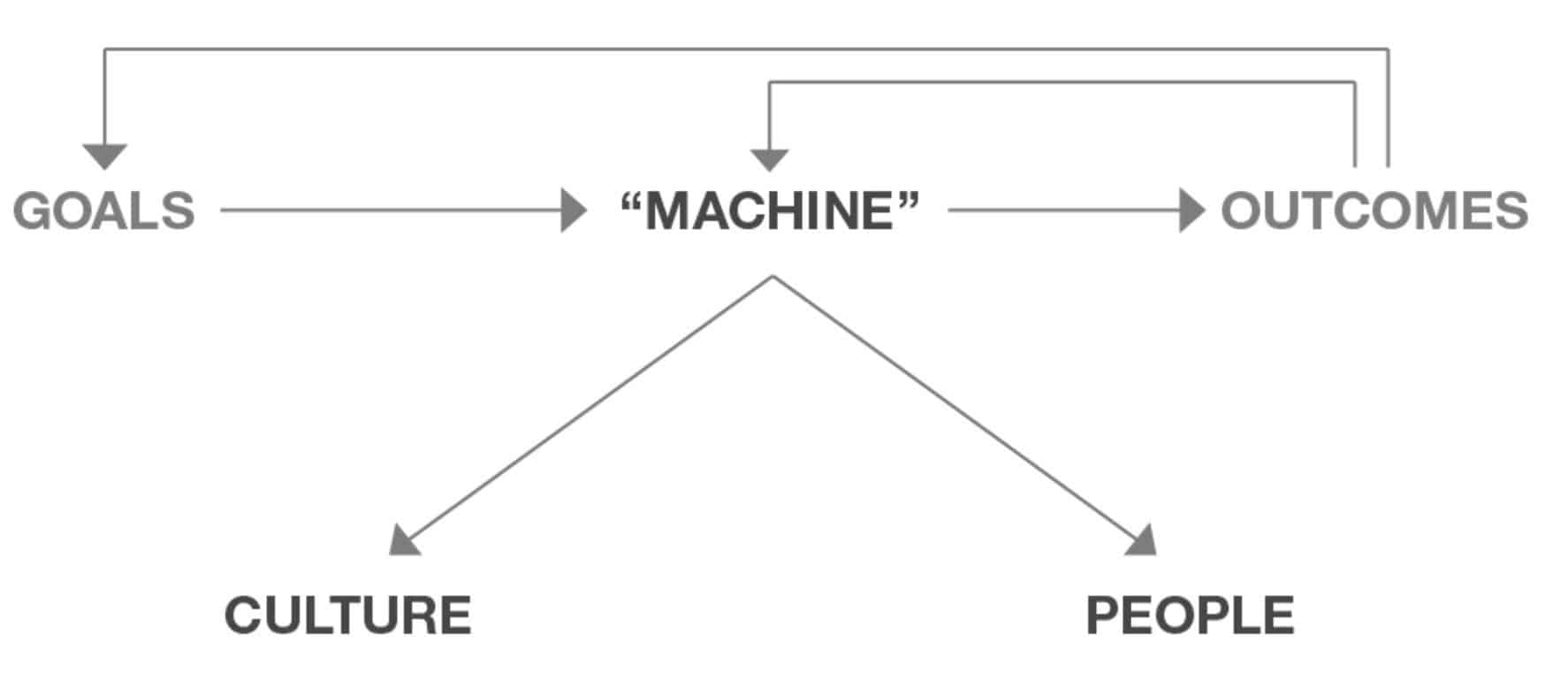

The framework for Dalio’s philosophy and the way in which he views/evaluates the world is summed up in the following chart (via Principles).

That schematic is meant to convey that your goals will determine the “machine” that you create to achieve them; that machine will produce outcomes that you should compare with your goals to judge how your machine is working. Your “machine” will consist of the design and people you choose to achieve the goals. For example, if you want to take a hill from an enemy you will need to figure out how to do that—e.g., your design might need two scouts, two snipers, four infantrymen, one person to deliver the food, etc. While having the right design is essential, it is only half the battle. It is equally important to put the right people in each of these positions. They need different qualities to play their positions well—e.g., the scouts must be fast runners, the snipers must be precise shots, etc. If your outcomes are inconsistent with your goals (e.g., if you are having problems), you need to modify your “machine,” which means that you either have to modify your design/culture or modify your people.

Do this often and well and your improvement process will look like the one on the left and do it poorly and it will look like the one on the right, or worse:

I call it “higher level thinking” because your perspective is that of one who is looking down on your machine and yourself objectively, using the feedback loop as I previously described. In other words, your most important role is to step back and design, operate and improve your “machine” to get what you want.

This is a powerful model. It forces you to be objective in assessing the quality of your beliefs and habits, thus leading to improving outcomes through the feedback loop of continuous iteration.

Now compare this to how most people go after their goals. The average person’s machine is akin to throwing spaghetti at the wall to see what sticks. Most people are reactive to life; never objectively assessing the quality of their beliefs or habits. This is why they never attain their desired outcomes.

The first step in effectively working towards your goals is to clarify what they are and why you really want them. From there you work backwards.

Without clarity of purpose and planning out the “how”, you’re doomed to walk circles. Stoic philosopher Seneca the Younger mentioned this in his writings Tranquility of Mind, “Let all your efforts be directed to something, let it keep that end in view. It’s not activity that disturbs people, but false conceptions of things that drive them mad.”

Law 29 of The 48 Laws of Power is: Plan All The Way To The End. Author Robert Greene writes, “By Planning to the end you will not be overwhelmed by circumstances and you will know when to stop. Gently guide fortune and help determine the future by thinking far ahead.” The second habit in The 7 Habits of Highly Effective People is to “begin with the end in mind.”

The end is always your starting point. Here’s Dalio further spelling out the process for creating optimal outcomes.

My 5-Step Process to Getting What You Want Out of Life

There are five things that you have to do to get what you want out of life. First, you have to choose your goals , which will determine your direction. Then you have to design a plan to achieve your goals. On the way to your goals, you will encounter problems . As I mentioned, these problems typically cause pain. The most common source of pain is in exploring your mistakes and weaknesses. You will either react badly to the pain or react like a master problem solver. That is your choice. To figure out how to get around these problems you must be calm and analytical to accurately diagnose your problems. Only after you have an accurate diagnosis of them can you design a plan that will get you around your problems. Then you have to do the tasks specified in the plan. Through this process of encountering problems and figuring out how to get around them, you will become progressively more capable and achieve your goals more easily. Then you will set bigger, more challenging goals, in the same way that someone who works with weights naturally increases the poundage. This is the process of personal evolution, which I call my 5-Step Process.

In other words, “The Process” consists of five distinct steps:

Have clear goals.

Identify and don’t tolerate the problems that stand in the way of achieving your goals.

Accurately diagnose these problems.

Design plans that explicitly lay out tasks that will get you around your problems and on to your goals.

Implement these plans—i.e., do these tasks.

By and large, life will give you what you deserve and it doesn’t give a damn what you “like.” So it is up to you to take full responsibility to connect what you want with what you need to do to get it, and then to do those things—which often are difficult but produce good results—so that you’ll then deserve to get what you want.

This mental model can — and should — be applied to every endeavor, especially trading and investing.

But objectively assessing the quality of our beliefs and habits is a lot easier said than done. It’s the main reason why the majority of people keep spinning their wheels.

To be truly objective requires us to acknowledge frequent mistakes and wrong beliefs — both of which everybody is guilty of. I can assure you that you hold a number of completely false beliefs and have numerous poor habits. I know I do. And dealing with these are initially painful. That initial pain stems from the human ego.

Here’s Dalio on the many harmful 1st and 2nd order effects of being ruled by ego and how to work to tame that ego.

Watch out for people who think it’s embarrassing not to know.

Be wary of the arrogant intellectual who comments from the stands without having played on the field.

Don’t worry about looking good – worry about achieving your goals.

I believe that one of the best ways of getting at truth is reflecting with others who have opposing views and who share your interest in finding the truth rather than being proven right.

There is giant untapped potential in disagreement, especially if the disagreement is between two or more thoughtful people.

The pain of problems is a call to find solutions rather than a reason for unhappiness and inaction, so it’s silly, pointless, and harmful to be upset at the problems and choices that come at you.

The best advice I can give you is to ask yourself what do you want, then ask ‘what is true’ — and then ask yourself ‘what should be done about it.’ I believe that if you do this you will move much faster towards what you want to get out of life than if you don’t!

More than anything else, what differentiates people who live up to their potential from those who don’t is a willingness to look at themselves and others objectively.

Life is like a game where you seek to overcome the obstacles that stand in the way of achieving your goals. You get better at this game through practice. The game consists of a series of choices that have consequences. You can’t stop the problems and choices from coming at you, so it’s better to learn how to deal with them.

If you can stare hard at your problems, they almost always shrink or disappear, because you almost always find a better way of dealing with them than if you don’t face them head on. The more difficult the problem, the more important it is that you stare at it and deal with it.

Unlike in school, in life you don’t have to come up with all the right answers. You can ask the people around you for help — or even ask them to do the things you don’t do well. In other words, there is almost no reason not to succeed if you take the attitude of One: total flexibility — good answers can come from anyone or anywhere. Two: Total accountability. Regardless of where the good answers come from, it’s your job to find them.

You’ll see that excuses like “That’s not easy” are of no value and that it pays to “push through it” at a pace you can handle. Like getting physically fit, the most important thing is that you keep moving forward at whatever pace you choose, recognizing the consequences of your actions.

Life is like a giant smorgasbord of more delicious alternatives than you can ever hope to taste. So you have to reject having some things you want in order to get other things you want more.

People who worry about looking good typically hide what they don’t know and hide their weaknesses, so they never learn how to properly deal with them and these weaknesses remain impediments in the future.

People who confuse what they wish were true with what is really true create distorted pictures of reality that make it impossible for them to make the best choices.

People who acquire things beyond their usefulness not only will derive little or no marginal gains from these acquisitions, but they also will experience negative consequences, as with any form of gluttony.

Since the only way you are going to find solutions to painful problems is by thinking deeply about them — i.e., reflecting — if you can develop a knee-jerk reaction to pain that is to reflect rather than to fight or flee, it will lead to your rapid learning/evolving.

I believe that we all get rewarded and punished according to whether we operate in harmony or in conflict with nature’s laws, and that all societies will succeed or fail in the degrees that they operate consistently with these laws.

Though how nature works is way beyond man’s ability to comprehend, I have found that observing how nature works offers innumerable lessons that can help us understand the realities that affect us.

Success is achieved by people who deeply understand reality and know how to use it to get what they want. The converse is also true: idealists who are not well-grounded in reality create problems, not progress.

I believe there are an infinite number of laws of the universe and that all progress or dreams achieved come from operating in a way that’s consistent with them. These laws and the principles of how to operate in harmony with them have always existed. We were given these laws by nature. Man didn’t and can’t make them up. He can only hope to understand them and use them to get what he wants.

I believe that our society’s “mistake-phobia” is crippling, a problem that begins in most elementary schools, where we learn to learn what we are taught rather than to form our own goals and to figure out how to achieve them. We are fed with facts and tested and those who make the fewest mistakes are considered to be the smart ones, so we learn that it is embarrassing to not know and to make mistakes. Our education system spends virtually no time on how to learn from mistakes, yet this is critical to real learning.

I learned that everyone makes mistakes and has weaknesses and that one of the most important things that differentiates people is their approach to handling them. I learned that there is an incredible beauty to mistakes, because embedded in each mistake is a puzzle, and a gem that I could get if I solved it, i.e. a principle that I could use to reduce my mistakes in the future.

Sometimes we forge our own principles and sometimes we accept others’ principles, or holistic packages of principles, such as religion and legal systems. While it isn’t necessarily a bad thing to use others’ principles — it’s difficult to come up with your own, and often much wisdom has gone into those already created — adopting pre-packaged principles without much thought exposes you to the risk of inconsistency with your true values.

Don’t be a perfectionist, because perfectionists often spend too much time on little differences at the margins at the expense of other big, important things. Be an effective imperfectionist. Solutions that broadly work well (e.g., how people should contact each other in the event of crises) are generally better than highly specialized solutions (e.g., how each person should contact each other in the event of every conceivable crisis).

Experience creates internalization. A huge difference exists between memory-based “book” learning and hands-on, internalized learning. A medical student who has “learned” to perform an operation in his medical school class has not learned it in the same way as a doctor who has already conducted several operations. In the first case, the learning is stored in the conscious mind, and the medical student draws on his memory bank to remember what he has learned. In the second case, what the doctor has learned through hands-on experience is stored in the subconscious mind and pops up without his consciously recalling it from the memory bank.

It is a law of nature that you must do difficult things to gain strength and power. As with working out, after a while you make the connection between doing difficult things and the benefits you get from doing them, and you come to look forward to doing these difficult things.

Ask yourself whether you have earned the right to have an opinion. Opinions are easy to produce, so bad ones abound. Knowing that you don’t know something is nearly as valuable as knowing it. The worst situation is thinking you know something when you don’t.

There are far more good answers “out there” than there are in you.

When you think that it’s too hard, remember that in the long run, doing the things that will make you successful is a lot easier than being unsuccessful.

Remember that experience creates internalization. Doing things repeatedly leads to internalization, which produces a quality of understanding that is generally vastly superior to intellectualized learning.

At Bridgewater people have to value getting at truth so badly that they are willing to humiliate themselves to get it.

For those of you who have studied the literature on performance psychology, you’ll recognize a large number of influences in Dalio’s work. Everything from the teachings of Buddhism to est to Tony Robbins and many others are woven into Dalio’s framework for success. In my opinion, his Principles are the most comprehensive and effective framework for getting what you want that I’ve read… and I’ve read a lot on this topic.

Dalio has taken this framework and has ruthlessly applied it to markets as well.

On the Nature of Trading

Alpha is zero sum. In order to earn more than the market return, you have to take money from somebody else.

If you’re going to come to the poker table, you’re going to have to beat me. … We have 1500 people who work at Bridgewater. We spend hundreds of millions of dollars on research and so on, we’ve been doing this for 37 years.

The nature of investing is that a very small percentage of the people take money, essentially, in that poker game, away from other people who don’t know when prices go up whether that means it’s a good investment or if it’s a more expensive investment. Too many investors are reactive decision-makers. If something has gone up, they say, ‘Ah, that’s a good investment.’ They don’t say, ‘That’s more expensive.

This is something many traders forget but it’s a very important truth to keep front of mind. There’s always another person on the other side of your trade. If you’re buying, someone is selling to you. If you’re selling, someone is buying from you. And everybody has the same goal: To Make Money! But the buyer and seller can’t both be right. Obviously one party always has to be wrong. Couple that with the fact that some of the smartest people in the world are working with enormous amounts of money and incredibly advanced tools (like Bridgewater) to extract profits from the markets and trading doesn’t seem so easy, does it?

Not to discourage you, that’s just the reality of it. Consistently beating the market is as difficult as becoming an olympic athlete… or probably even more so.

But it’s not impossible either…

It all comes down to interest rates. As an investor, all you’re doing is putting up a lump-sum payment for a future cash flow…. The big question is: When will the term structure of interest rates change? That’s the question to be worried about. .. He who lives by the crystal ball [in trying to forecast interest rates] will eat shattered glass.

Risky things are not in themselves risky if you understand them and control them. If you do it randomly and you are sloppy about it, it can be very risky.

We think of commodities from a few different perspectives: as an alternative currency and store hold of wealth, as a growth-sensitive asset class, and as an asset with specific supply and demand considerations.

The biggest mistake investors make is to believe that what happened in the recent past is likely to persist. They assume that something that was a good investment in the recent past is still a good investment. Typically, high past returns simply imply that an asset has become more expensive and is a poorer, not better, investment.

People tend to think that my success, or whatever you want to call it, has been because I’m a really good decision-maker. I think it is actually because I’m less confident in making decisions. So in other words, I never know anything really. Everything is a probability.

You can’t make money agreeing with the consensus view, which is already embedded in the price. Yet whenever you’re betting against the consensus, there’s a significant probability you’re going to be wrong, so you have to be humble.

On What Moves Markets and How to Profit From Them

If you’re interested in macro — if you’re a trader or investor, you should be — then it behooves you to take some time and read through Bridgewater’s paper titled “How the Economic Machine Works”. It’s the best framework on how to view and understand markets and economies.

At the foundation of this framework is the Transactions Approach; which is a different way of looking at transactions and price discovery compared to classic economic supply and demand models.

![]()

Every time you buy something, you create a transaction and transactions are the building blocks of the economic machine. Understanding transactions is the key to understanding the whole economy. An economy consists of all of the transactions and all of its markets. Adding up the total quantity of transactions in all markets gives you everything you need to know to understand the economy. The biggest buyer and seller is the government, which a) through a central bank controls the credit in the economy and b) collects taxes and spends money.

These transactions form markets and markets form economies. One of the keys to successful trading and investing is to understand who the buyers are, what their motivation is, and what the credit/liquidity picture looks like.

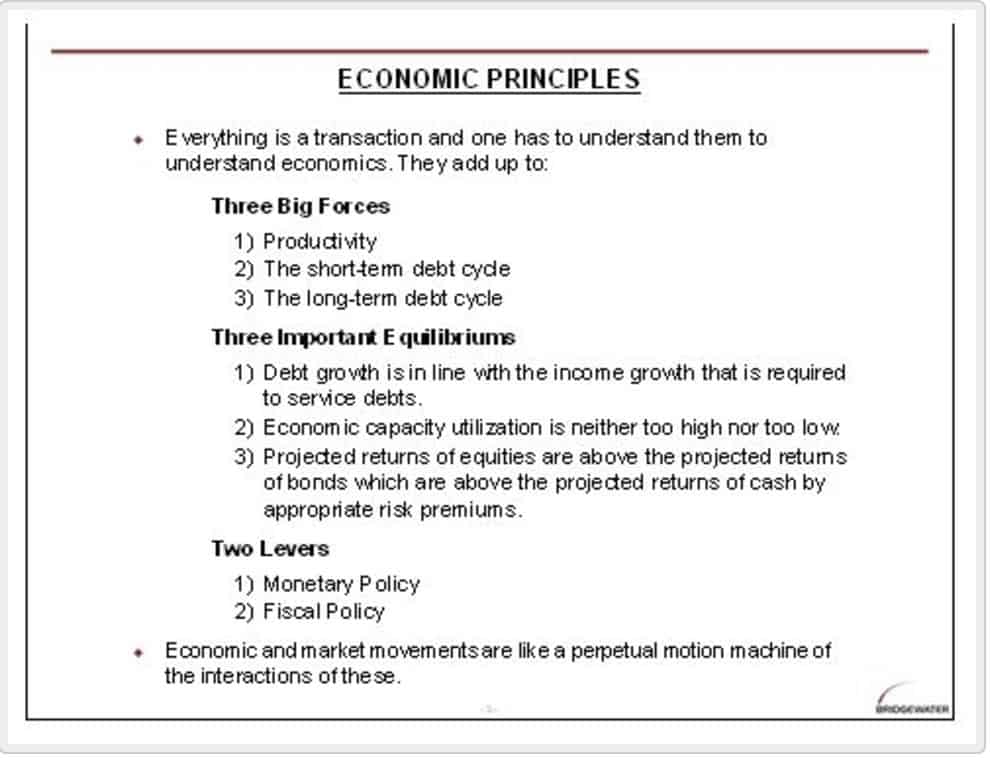

Following the transaction model we get to debt cycles (which you can read more about here). Here is the basic premise below (via Economic Principles).

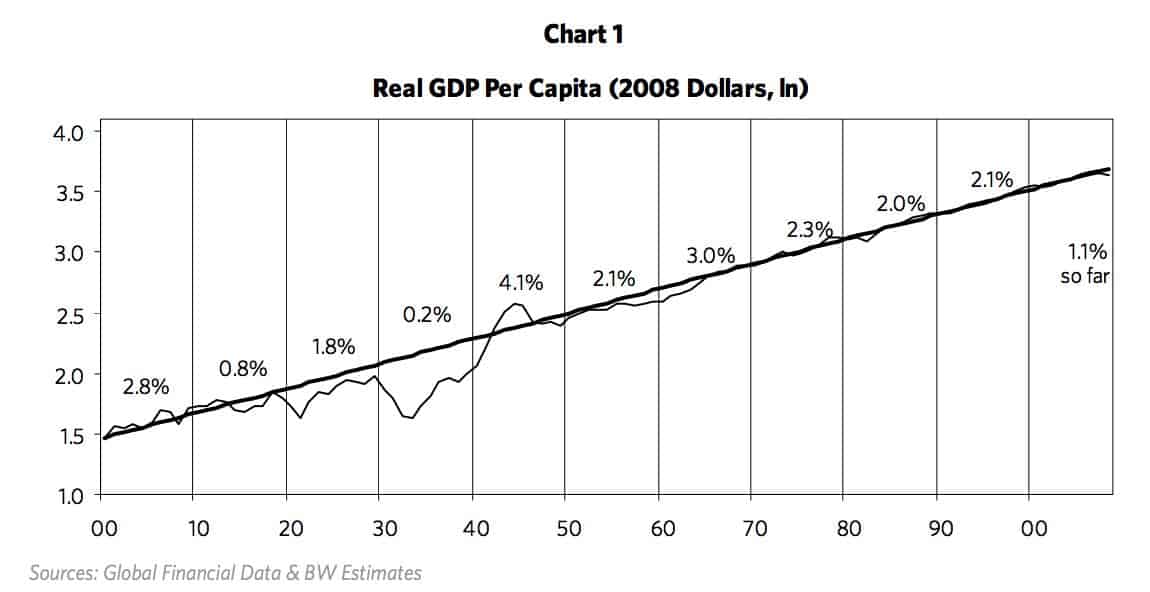

As shown below in chart 1, real per capita GDP has increased at an average rate of a shade less than 2% over the last 100 years and didn’t vary a lot from that. This is because, over time, knowledge increases, which in turn raises productivity and living standards. As shown in this chart, over the very long run, there is relatively little variation from the trend line. Even the Great Depression in the 1930s looks rather small. As a result, we can be relatively confident that, with time, the economy will get back on track. However, up close, these variations from trend can be enormous. For example, typically in depressions the peak-to-trough declines in real economic activity are around 20%, the destruction of financial wealth is typically more than 50% and equity prices typically decline by around 80%. The losses in financial wealth for those who have it at the beginning of depressions are typically greater than these numbers suggest because there is also a tremendous shifting of who has wealth.

Swings around this trend are not primarily due to expansions and contractions in knowledge. For example, the Great Depression didn’t occur because people forgot how to efficiently produce, and it wasn’t set off by war or drought. All the elements that make the economy buzz were there, yet it stagnated. So why didn’t the idle factories simply hire the unemployed to utilize the abundant resources in order to produce prosperity? These cycles are not due to events beyond our control, e.g., natural disasters. They are due to human nature and the way the credit system works. Most importantly, major swings around the trend are due to expansions and contractions in credit – i.e., credit cycles, most importantly 1) a long-term (typically 50 to 75 years) debt cycle and 2) a shorter-term (typically 5 to 8 years) debt cycle (i.e., the “business/market cycle”).

I find that whenever I start talking about cycles, particularly the long-term variety, I raise eyebrows and elicit reactions similar to those I’d expect if I were talking about astrology. For this reason, before I begin explaining these two debt cycles I’d like to say a few things about cycles in general.

A cycle is nothing more than a logical sequence of events leading to a repetitious pattern. In a market-based economy, cycles of expansions in credit and contractions in credit drive economic cycles and they occur for perfectly logical reasons. Each sequence is not pre-destined to repeat in exactly the same way nor to take exactly the same amount of time, though the patterns are similar, for logical reasons. For example, if you understand the game of Monopoly®, you can pretty well understand credit and economic cycles. Early in the game of Monopoly®, people have a lot of cash and few hotels, and it pays to convert cash into hotels. Those who have more hotels make more money. Seeing this, people tend to convert as much cash as possible into property in order to profit from making other players give them cash. So as the game progresses, more hotels are acquired, which creates more need for cash (to pay the bills of landing on someone else’s property with lots of hotels on it) at the same time as many folks have run down their cash to buy hotels. When they are caught needing cash, they are forced to sell their hotels at discounted prices. So early in the game, “property is king” and later in the game, “cash is king.” Those who are best at playing the game understand how to hold the right mix of property and cash, as this right mix changes.

If you can grasp this and understand the role of credit in driving demand and both the short-term debt cycle (aka business cycle) and longer-term debt-cycle, then you are already leaps and bounds ahead of any economist with a PhD attached to their name.

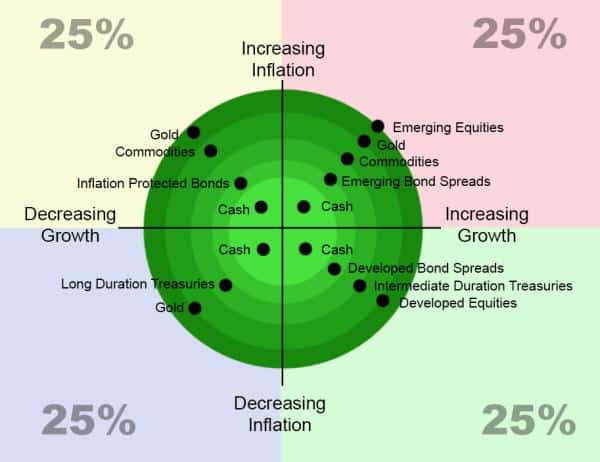

Dalio is great at breaking things down to their essentials or first principles. An example of this is how he looks at the drivers of various asset classes. This is called the quadrant approach, which he uses as a basis for his All-Weather fund.

The idea is that every asset class performs a certain way depending on the economic environment. There are two primary forces that comprise an economic environment. These are: inflation and growth. You combine these and you get four states: decreasing inflation, decreasing growth; decreasing inflation, increasing growth; increasing inflation, decreasing growth; increasing inflation, increasing growth.

In our view, there are many markets but just a few primary market forces, and these forces influence all of them. A market price is the discounted present value of future cash flows. Economic growth and inflation are the two most significant drivers of those cash flows, and discount rates and risk premiums determine how these cash flows are reflected in current prices. Given this, prices largely reflect discounted future economic scenarios, which are a combination of discounted growth, discounted inflation, risk premiums and discount rates. The magnitudes of price changes reflect shifts in these four forces.

Bonds will perform best during times of disinflationary recession, stocks will perform best during periods of growth, and cash will be the most attractive when money is tight. Translation: All asset classes have environmental biases. They do well in certain environments and poorly in others.

When I say uncorrelated asset classes, what I’m really doing is not using the classic measure of correlation, like stocks and bonds are 40% correlated. What I am instead really referring to us, do you know how they behave, and is it intrinsically going to behave alike or differently?

The only way to achieve reliable diversification is to balance a portfolio based on the relationships of assets to their environmental drivers, rather than based on correlation assumptions, which are just fleeting byproducts of these relationships. To do this, we recognize that while asset classes offer a risk premium that is by and large the same once adjusting for risk, their inherent sensitivities to shifts in the economic environment are not the same. Therefore you can structure a portfolio of risk-adjusted asset classes so that their environmental sensitivities reliably offset one another, leaving the risk premium as the dominant driver of returns.

Underperformance of a given asset class relative to its risk premium in a particular environment (e.g., nominal bonds in higher than expected inflation) will automatically be offset by the outperformance of another asset class with an opposing sensitivity to that environment (e.g., commodities), leaving the risk premium as the dominant source of returns, and producing a more stable overall portfolio return.

The only free lunch in investing is diversification. But what is true diversification?

Many investors thought they were diversified in 2008 but quickly found out that was wrong when their asset correlations all went to one.

Recent beta and short-term backward looking correlations are a poor indicator of future correlations and risk. To truly diversify, you need to understand the principle drivers (inflation, growth) of the broader asset classes you hold and deduce the correlations (risk) from there.

As soon as you understand that, you can then apply what Dalio calls, “The Holy Grail of investing” (first paragraph via Market Wizards).

[Dalio walks over to the board and draws a diagram where the horizontal axis represents the number of investments and the vertical axis the standard deviation.] This is a chart that I teach people in the firm, which I call the Holy Grail of investing. [He then draws a curve that slopes down from left to right—that is, the greater the number of assets, the lower the standard deviation.] This chart shows how the volatility of the portfolio changes as you add assets. If you add assets that have a 0.60 correlation to the other assets, the risk will go down by about 15 percent as you add more assets, but that’s about it, even if you add a thousand assets. If you run a long-only equity portfolio, you can diversify to a thousand stocks and it will only reduce the risk by about 15 percent, since the average stock has about a 0.60 correlation to another stock. If, however, you’re combining assets that have an average of zero correlation, then by the time you diversify to only 15 assets, you can cut the volatility by 80 percent. Therefore, by holding uncorrelated assets, I can improve my return/risk ratio by a factor of five through diversification….I strive for approximately 100 different return streams that are roughly uncorrelated to each other. There are cross-correlations that enter into it, so the number works out to be less than 100, but it is well over 15. ~

So for example, if I had return streams that were 60% correlated, and I had a thousand of them, I would only reduce the risk by about 15%. And after 5 or 6, it’s limited. SO there’s a certain notion when approaching investing. What do I want? I need to have a certain structure. That can come in the form of alphas and betas. What is my risk neutral position? I’ll say everybody in the room, they say what should I invest in? They don’t start off, I think, with what is a neutral position. What represents a good neutral position, balance? For example, does gold represent a part of my portfolio? What should, if I had no view, what should the concentration in dollars be? What is a structural beta portfolio? And then how do I take a deviation from that beta portfolio? And how do I do that in an uncorrelated way, so that I can then maximize my return to risk? So in that first principle, what I’m saying is that if you follow that first principle and you get 15 good — don’t have to be great — uncorrelated return streams, you’ll improve your return to your risk by a factor of 5. That means 5 times the return for the same amount of risk. That’s just a principle; that’s a reality.

So that’s the framework, the Machine, for not only how to view markets and economies but for how to attain everything you want in life, all via Ray Dalio.

His thinking has had a profound impact on my own, as I hope it does with your thinking as well.

If you’re craving more lessons from the trading greats, then check out our in-depth special report by clicking here.