It is poor policy, I find, to wait for Opportunity to knock at your door. I train my ear so that I can hear Opportunity coming down the street long before it reaches my door. When Opportunity knocks, I try to reach out, grab Opportunity by the collar and yank it in. ~ Richard D. Wyckoff

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at price targets following new record highs, check out rising global markets, dissect fund flows to see where capital is headed, look at world equity valuations, and see what’s going on in Putin’s Russia, plus more…

- Both the S&P 500 and Nasdaq made new all-time weekly highs last week. The technician Peter Brandt (@PeterLBrandt) has a measured move target on the S&P of 3,524. Approximately 15% higher from current levels.

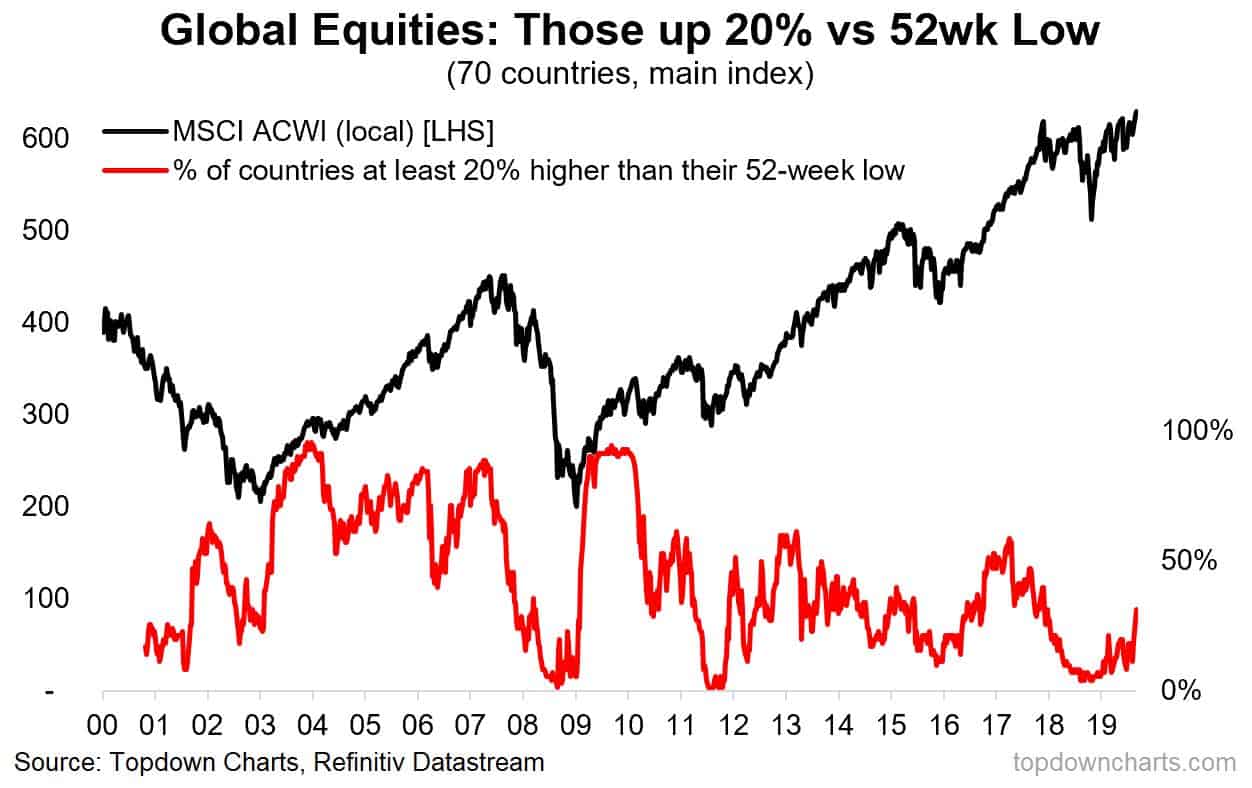

- This chart from Callum Thomas (@Callum_Thomas) shows it’s not just US markets that are moving higher. The percentage of countries at least 20% off their 52-week lows is trending up from a very low base.

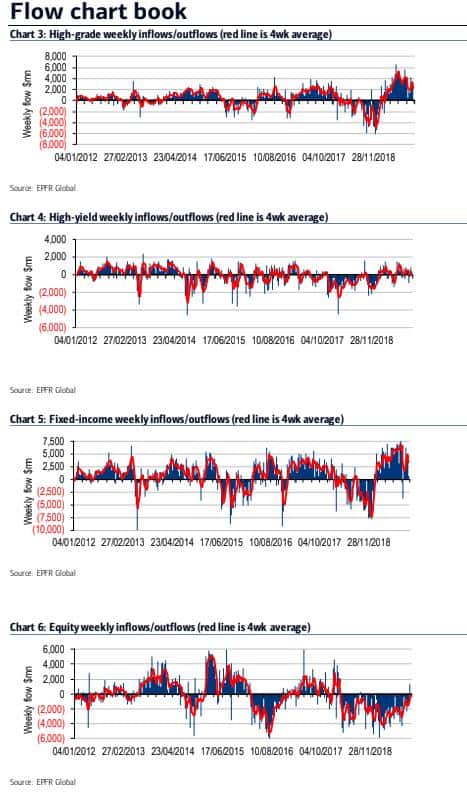

- We’re starting to see a reversal in flows out of bonds and into equities for the first time in a long while (chart via BofAML).

- Like a rubber band that has been wound tight, there’s plenty of potential energy to unravel. A process that could spark a flood back into risk assets (chart via BofAML).

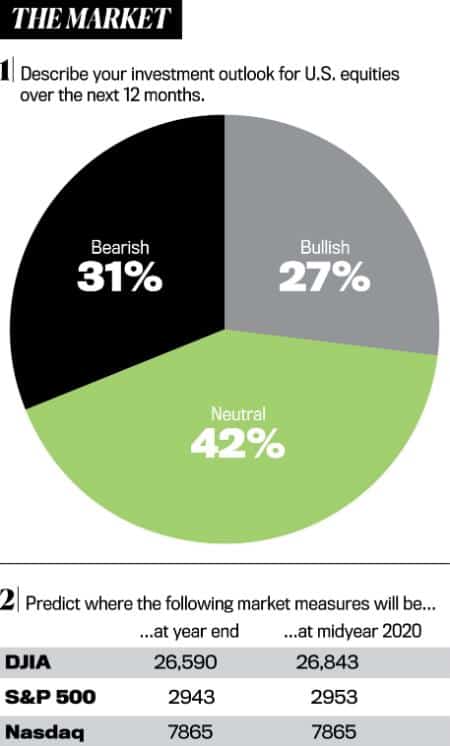

- The reason behind the lopsided flows is that money managers are bearish… and I mean extremely bearish… Barron’s latest “Big Money Poll” finds that only 27% of fund managers surveyed are bullish on stocks over the next 12-months. That’s the lowest bullish reading in more than 20-years.

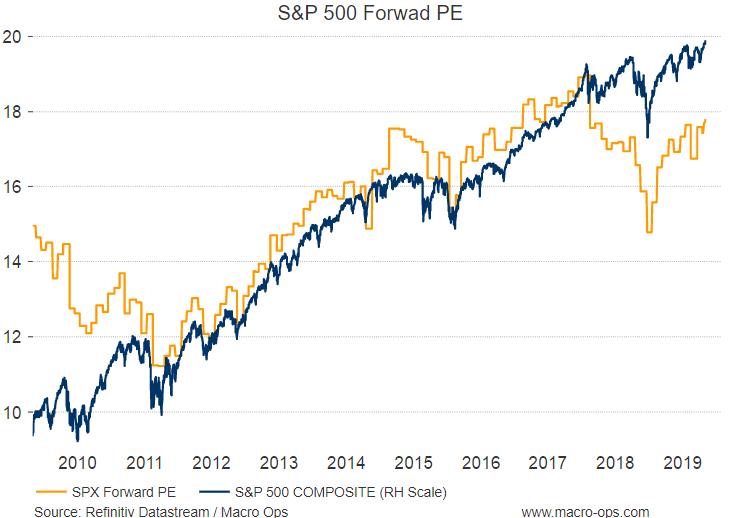

- Valuations in the US are back near levels that in the past have acted as headwinds for equity market returns. This doesn’t mean we can’t see US multiples expand further (they probably will). But it increases the fragility of the trend.

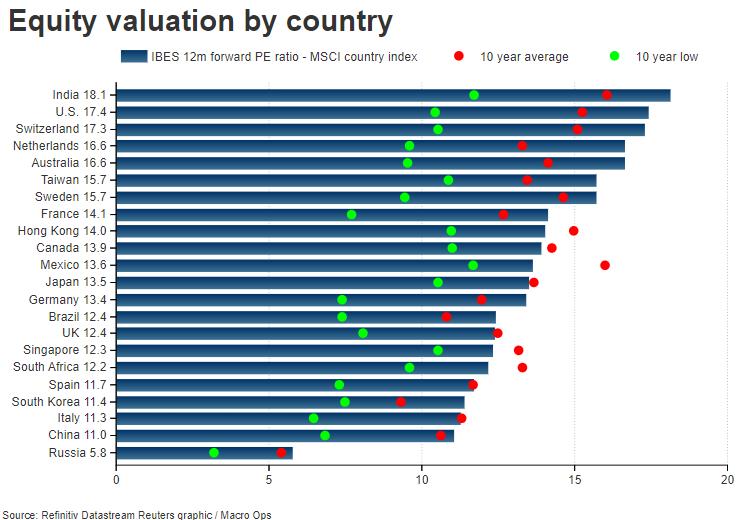

- It also means that investors who now find themselves horribly underinvested and who are looking to dramatically up their exposure to equities may look elsewhere.

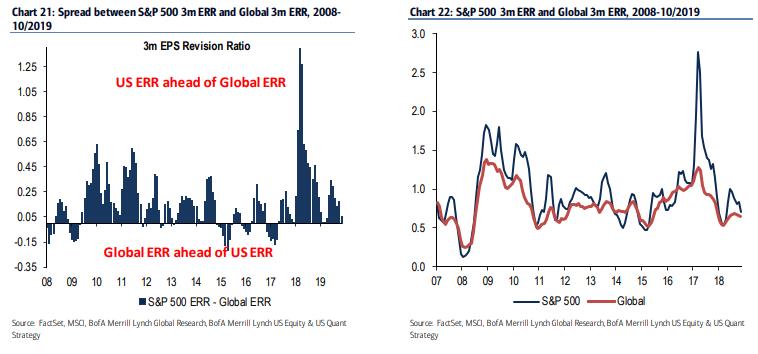

- The US has long earned its valuation premium over the rest-of-the-world due to its strong trend in earnings. But, BofAML noted in a recent report that this trend may be changing, writing “The US one-month ERR (0.49) has dropped below the global ERR (0.65) which is unusual. Note that in the post-crisis period, the S&P 500 ERR has been above the Global ERR 74% of the time, underscoring the earnings prowess of the S&P 500 relative to other regions due to its secular growth and quality biases. Are the tides shifting? Other signals suggest shifts from the US to other neglected pockets. Our global team notes that the October ratio improved the most in Asia Pac ex-Japan and Emerging Markets, but the ratio fell the most in the US (Europe’s ratio remained unchanged).”

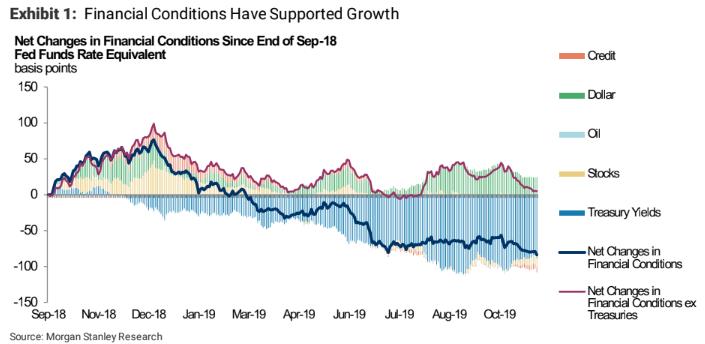

- Equity markets have been benefitting from improved financial conditions this year relative to last. One of the few remaining conditions that have been tightening liquidity has been the persistently strong US dollar. But the USD is back below its 200-day moving average and as I noted in last week’s Dozen, we might finally be seeing the turn in King Dollar. A trend that would further boost financial conditions and make underweighted ex.US assets even more attractive.

- One of the cheapest markets at the moment is Russia (RSX) which just broke out to new multi-year highs last week.

- Remember how a month ago the bears were sharing this chart of the ISM Manufacturing New Export Orders which had just hit new post-crisis lows? Well, it just rebounded in one of its strongest MoM reversals. I wonder why those same people aren’t sharing the chart now?

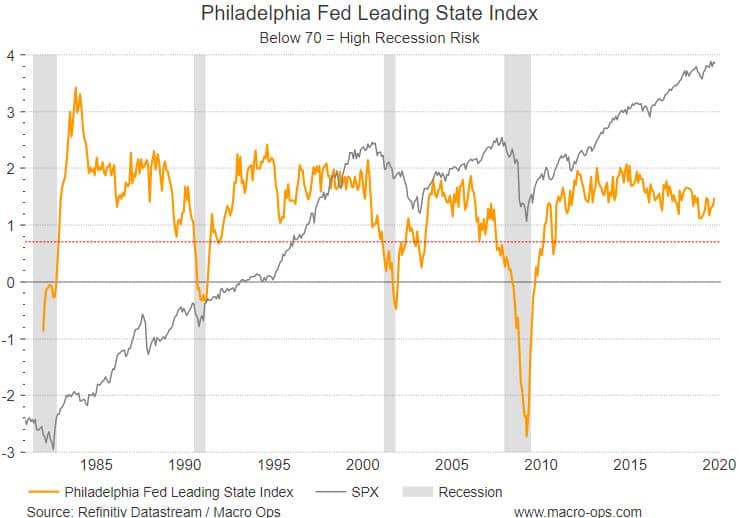

- Finally, one of my favorite leading recession indicators, the Philadelphia Fed Leading State Index, came out with another solid print this last month (when it crosses below the red horizontal line is when you need to worry). Just another sign, amongst many, that a recession is still a ways off.