There are really four kinds of trades or bets: good bets, bad bets, winning bets, and losing bets. Most people think that a losing trade was a bad bet. That is absolutely wrong. You can lose money even on a good bet. If the odds on a bet are 50/50 and the payoff is $2 versus a $1 risk, that is a good bet even if you lose. The important point is that if you do enough of those trades or bets, eventually you have to come out ahead. ~ Larry Hite

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at breakouts, breadth, and credit confirmations that are ALL signaling a move higher in global risk assets. Also, we look at positioning amongst inflation assets and see where the pain points in the US dollar are amongst CTAs. Plus more…

- Markets are breaking out to the upside everywhere. The S&P 500 Value Index is one of them. It made a new all-time high last week. According to Sentiment Trader, when the index “broke out to a new all-time high for the first time in 200+ days, the S&P 500 Value Index always went higher 6 months later”.

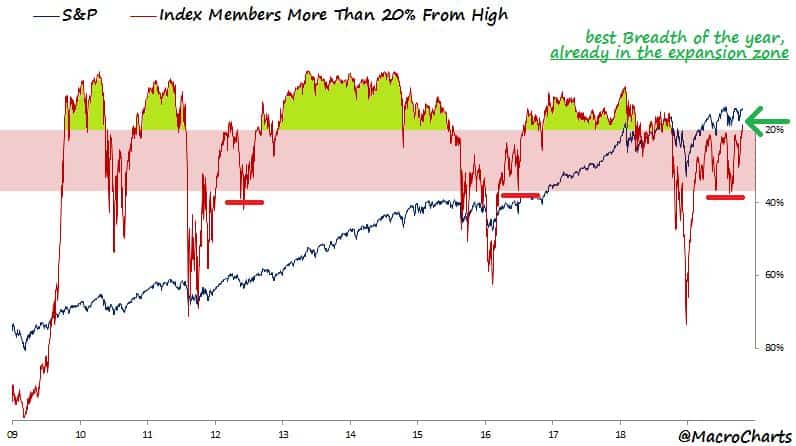

- When trying to gauge the strength of the underlying market trend, it’s key to pay attention to what’s going on under the hood in the individual issues. Breadth will nearly always precede major changes to the trend. This chart from @MacroCharts shows that breadth in the S&P is at its best level in over a year.

- I’m seeing similar indications of strength in nearly all my breadth and momentum indicators. Take the NYSE AD-line for example. It just made a new cycle high last week.

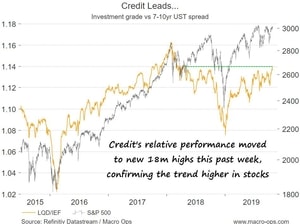

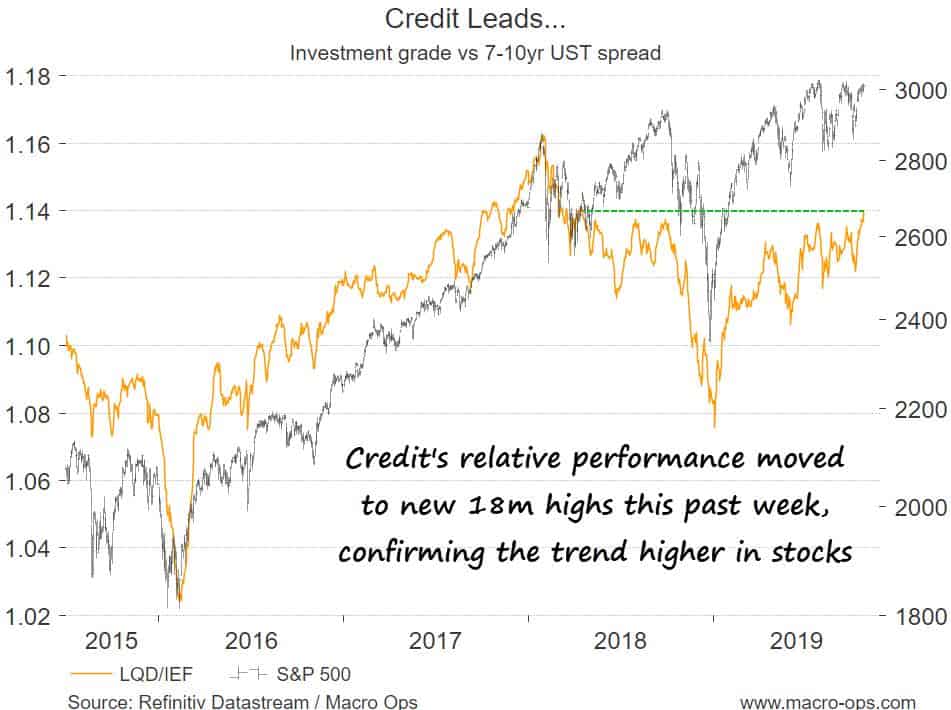

- And this strength isn’t just isolated to the equity market. Just as importantly, it’s showing up in credit as well. This past week we saw credit’s relative performance break out to new 18-month highs. This is exactly the type of action you want to see before a major move higher in stocks.

- Our “Leaders” are all doing what they’re supposed to be doing; moving up and to the right. Notice how the news and fintwit bears were all whining about Texas Instruments (TXN) earnings miss and lower guidance? Yet, the semis index (SMH) made new all-time highs last week (chart below is a weekly). Check your bias.

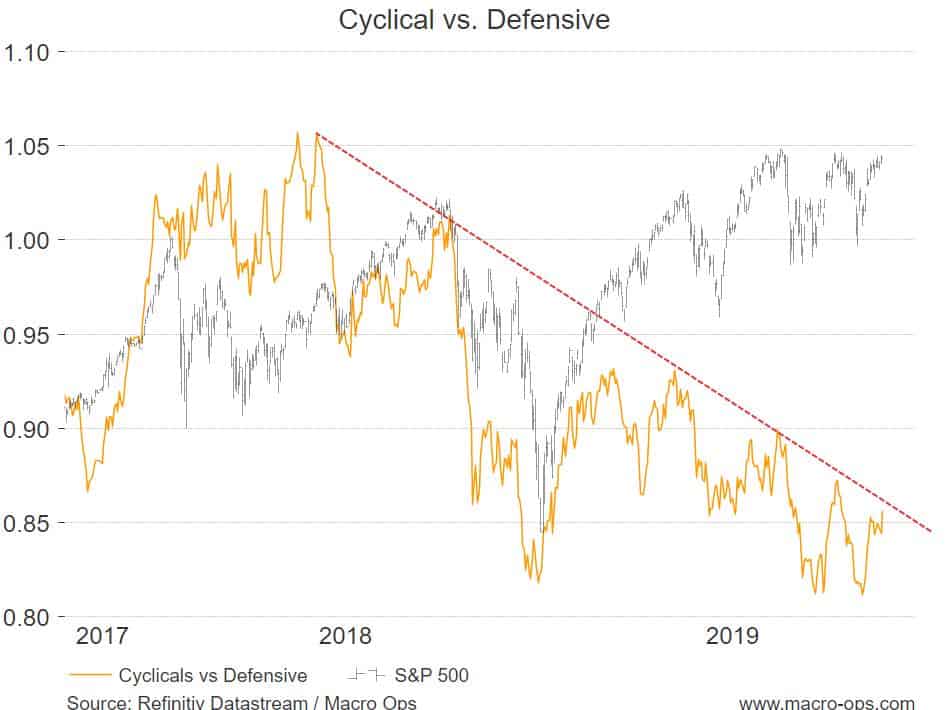

- Another thing to keep an eye on is cyclical vs defensive relative performance. Financials and industrials are on the verge of breaking out and the copper/gold ratio looks like it’s about to do the same. Another rate cut from the Fed this week (something which is looking likely) will steepen the curve and drive a bullish thrust in relative cyclical/defensive performance.

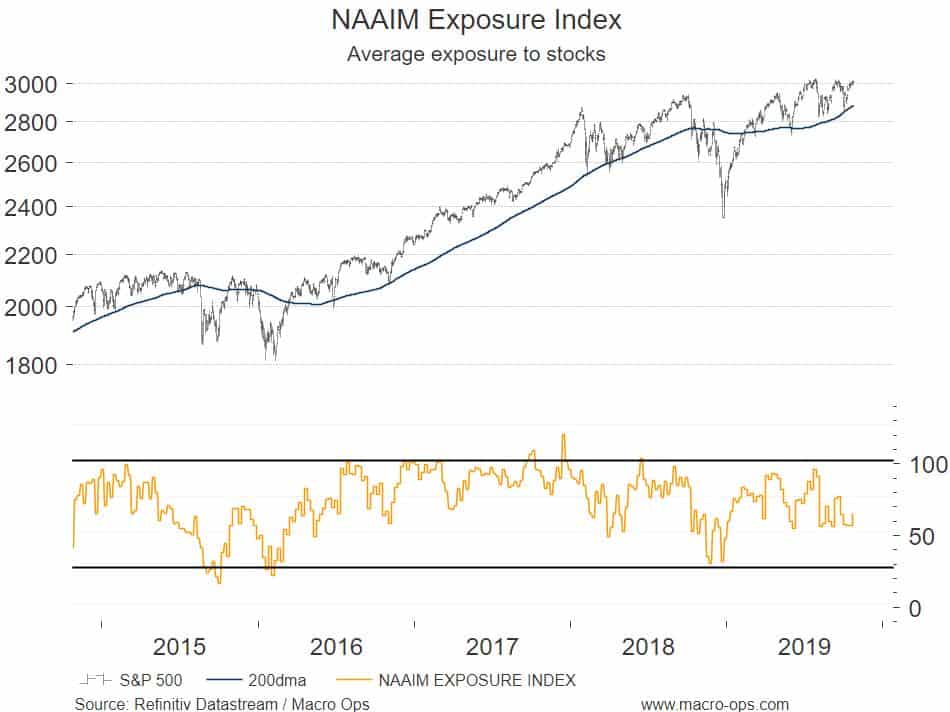

- I know I’ve been hammering this point over and over the last couple of months but sentiment and positioning remain in stark contrast to markets that are hitting new highs. The NAAIM Average Stock Exposure Index is at 65%, well below its 3yr and 5yr averages.

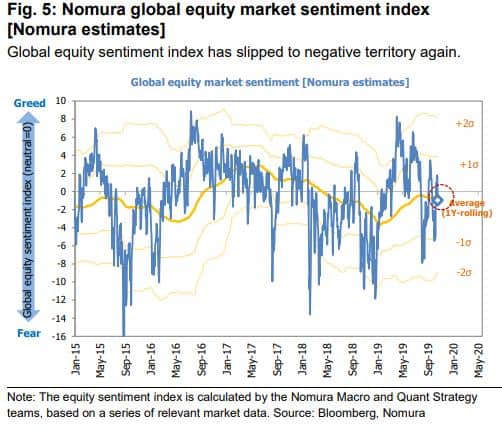

- And Nomura’s Global Equity Sentiment Index is back in negative territory. Apparently, no one is impressed with the across the board breakouts that are happening. This is exactly the type of sentiment we want to see for the next leg higher.

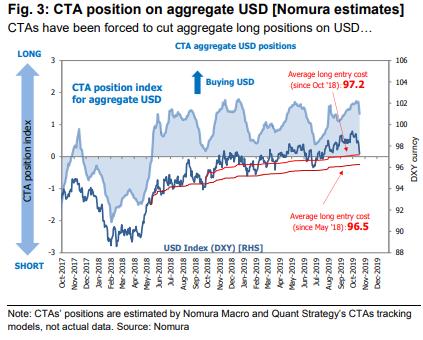

- We’re at a critical level for the US dollar. It’s still well within a technical uptrend and above its 200-day moving average. But as this chart from Nomura shows, if it moves any lower from here it will trigger selling from CTAs which could spark a positive feedback loop of a lower USD and more forced selling. The FOMC this week will be key to where the USD trades in the weeks to come.

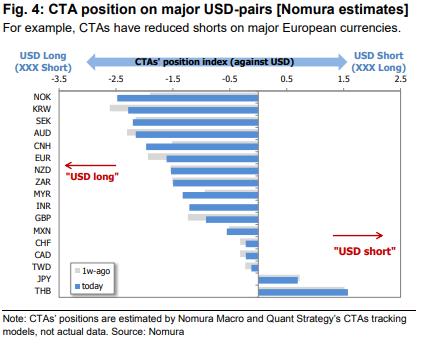

- And CTA’s are positioned fairly long the dollar against a number of pairs (chart via Nomura).

- If we do see the dollar trade lower from here it’ll be a nice and needed tailwind for crude where hedge fund short positioning has become increasingly crowded on the short side (chart via @Warrenpies & h/t @TN).

- We’ll end with another great chart from @MacroCharts that serves as a perfect reflection of the current positioning/sentiment zeitgeist. Citi’s Long/Short Inflation Ratio is at levels that have marked the absolute lows in long/short inflation positioning two other times this cycle. Stocks are breaking out on the back of strong breadth while bonds are looking precarious and the Fed is likely to cut right at the moment when the global manufacturing recession has troughed. Position accordingly.