The idea that you can’t beat the markets is a frightening prospect. That is why my guiding trading philosophy is playing great defense. If you make a good trade, don’t think it is because you have some uncanny foresight. Always maintain your sense of confidence, but keep it in check. ~ PTJ

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at some of the historic record-breaking moves going on in markets, check out the worst single day of carnage in the energy sector’s history, look at some increasing signs we’re nearing a tradeable bottom, and finish with some indicators showing the cycle may be turning for the worst. Let’s dive in…

***click charts to enlarge***

- It seems nearly every trading day now we’re seeing a new “record” being made. Well, here’s another one for the books via Bloomberg “Total U.S. Trading volume, on a 10-day moving average basis, is now higher than during the meltdown in 2008. Volume is another whopper today, over 17 billion shares. Emotional moves are tied to large volumes — what does it say about investor psychology when the big volume days are sustained over the course of two weeks?”

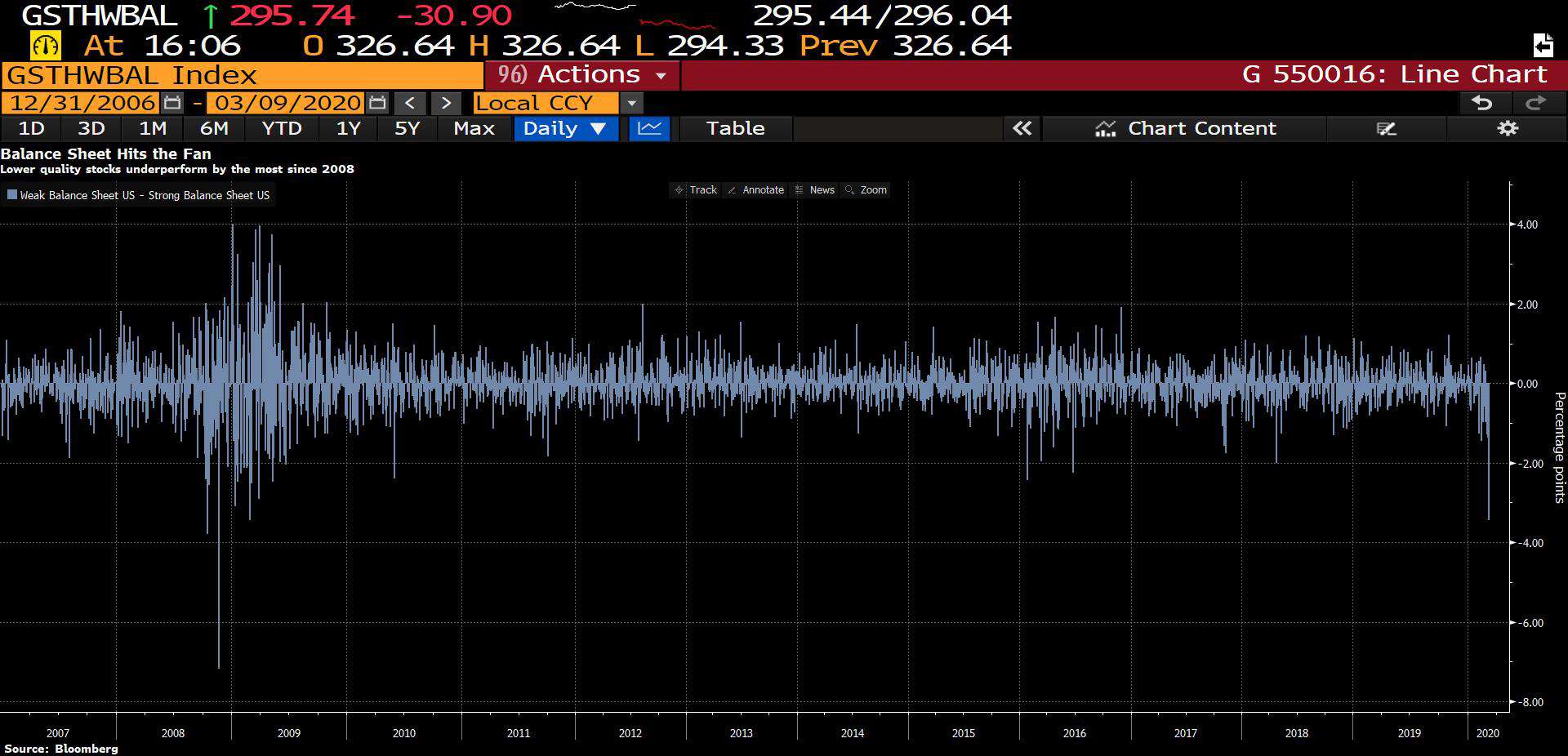

- If you’re still sitting long some names or are thinking about buying some soon, you might want to do a thorough QC of the balance sheet as US stocks with weak balance sheets are vastly underperforming those with strong foundations.

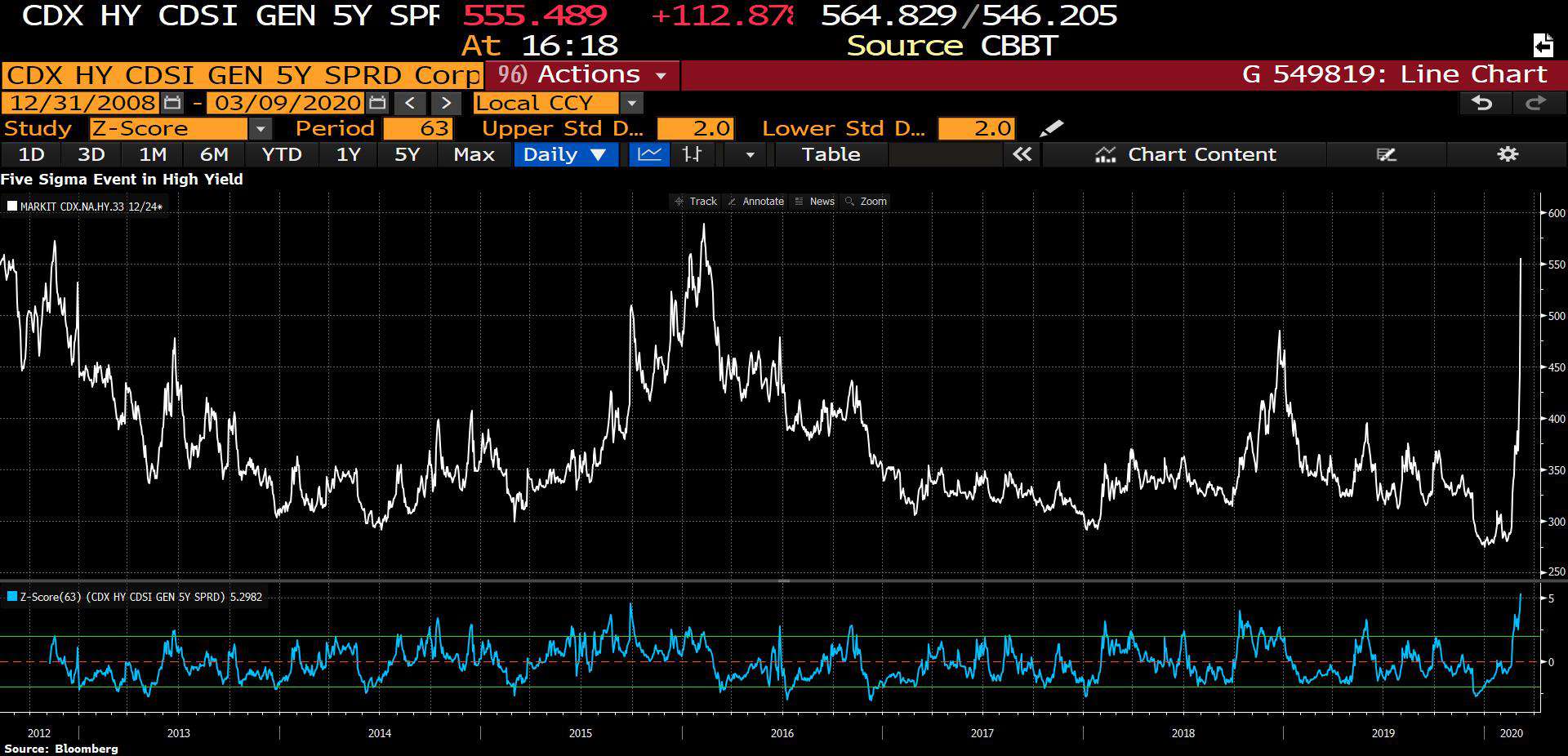

- We just saw a FIVE SIGMA EVENT in the credit market. This is the most violent dislocation to high-yield since the collapse of Lehman. Be careful out there…

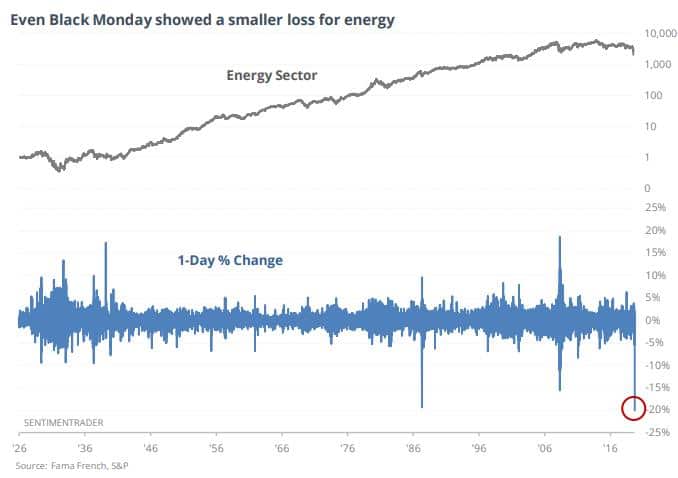

- The energy sector saw its worst single-day loss on record on Monday following the news that Russia and the Sauds are going to engage in an all-out price war. SentimenTrader notes that following similar one day declines to new 52-week lows, energy stocks were higher one month later every time with an instance in 2008 being the only exception.

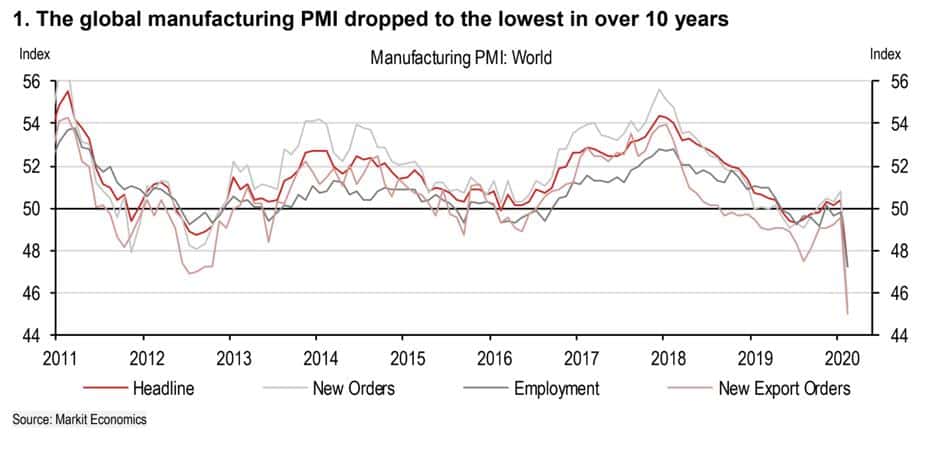

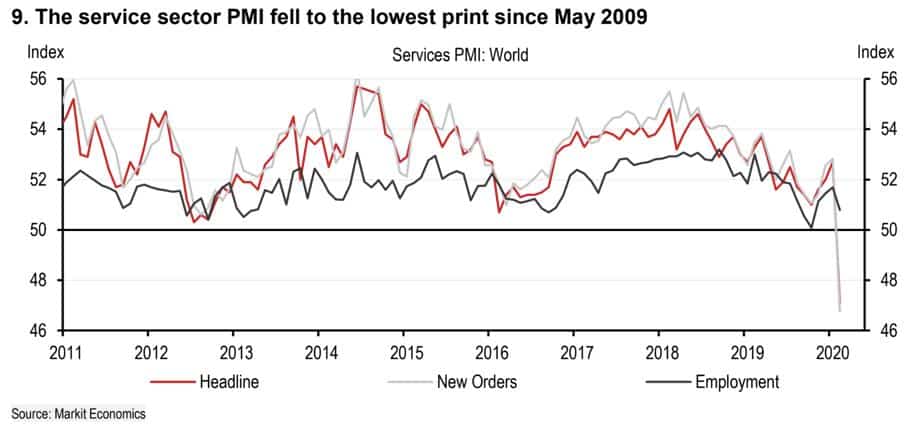

- The economic impact of the virus is just beginning to wind its way through the global economy and we should expect things to get worse before they get better. And that’s scary, considering Global Manufacturing PMI and Service’s New Orders are at their lowest levels since the GFC (charts via HSBC).

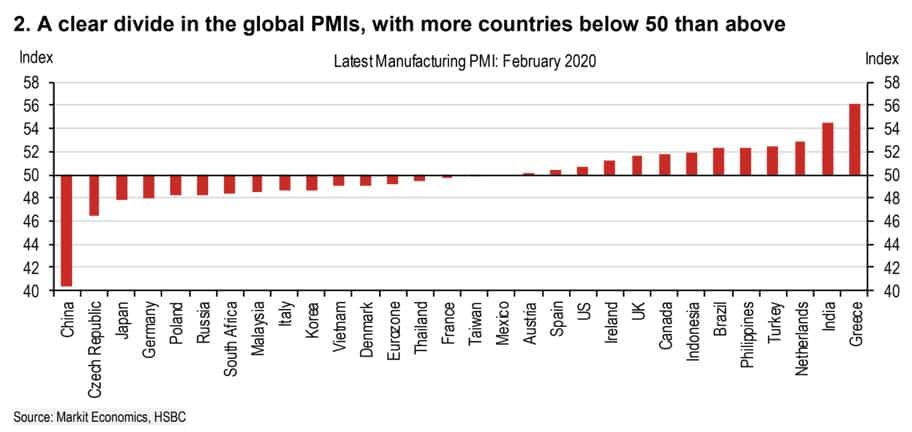

- There are now more countries with contractionary PMIs (sub 50) than there are ones showing growth (chart via HSBC).

- Scoping in and looking at things from a more short-term perspective, we are finally putting in the requisite foundations for a tradeable (multi-week) bottom. All the length of the put/call ratios that were so extended just a few weeks ago has now been taken out. Complacency has been replaced by fear.

- And oversold conditions have been hit across the board with the percentage of stocks trading above their 20d, 50d, and 200d moving averages now firmly in bottoming territory. I’m not convinced we’ve seen the full capitulation dump yet but that may come soon.

- @MacroCharts shared this chart showing the clusters of S&P down Fridays followed by -3%+ Mondays. As he points out “Since 87’, Monday crashes marked the closing bottom 6/11 times (five later retested). The remaining 5/11 were near final bottom — but needed residual declines to exhaust selling. Getting close-time to be on MAXIMUM alert.”

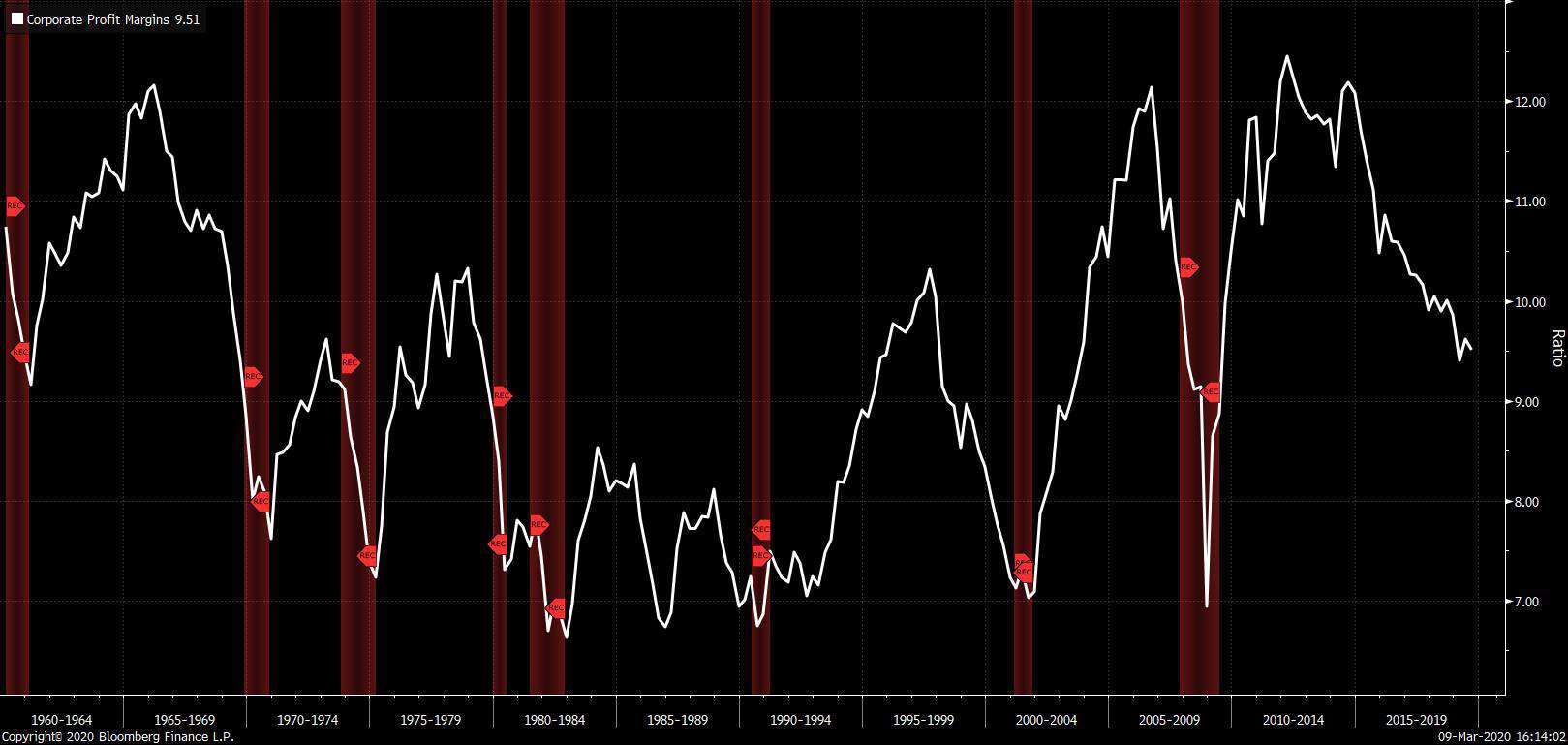

- Considering the high leverage being carried in our economy along with declining profit margins here in the US, I believe the risks that we tip into a recession and extended bear market later this year has gone up dramatically.

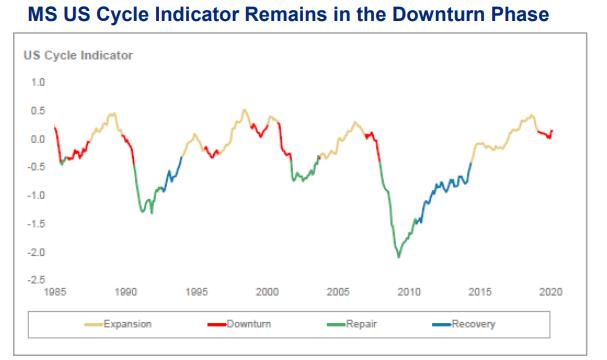

- Morgan Stanley’s US Cycle Indicator remains in a downturn phase. This indicator should weaken as more countries follow in Italy’s footsteps and enact stringent lockdown measures.

- Financial conditions are also tightening considerably according to MS’s Financial Conditions Index. Tops are processes, not events. The average market top takes 10-months to form, so I’m not calling for the start of an extended bear market. I just want to keep hammering home the point that the cone of plausible outcomes has widened dramatically in recent weeks and that means we should expect continued volatility. This is an environment for playing defense, not offense.

Stay safe out there and keep your head on a swivel!