The market anticipates, while the news exaggerates. ~ Bob Farrell

Good morning!

In this week’s Dirty Dozen [CHART PACK] we look at more short-term sell signals indicating further downside ahead, a massive collapse in global auto demand, a profit contraction in Germany and a possible recession in Mexico, plus some unprofitable IPOs and 230-years of global debt. Here we go…

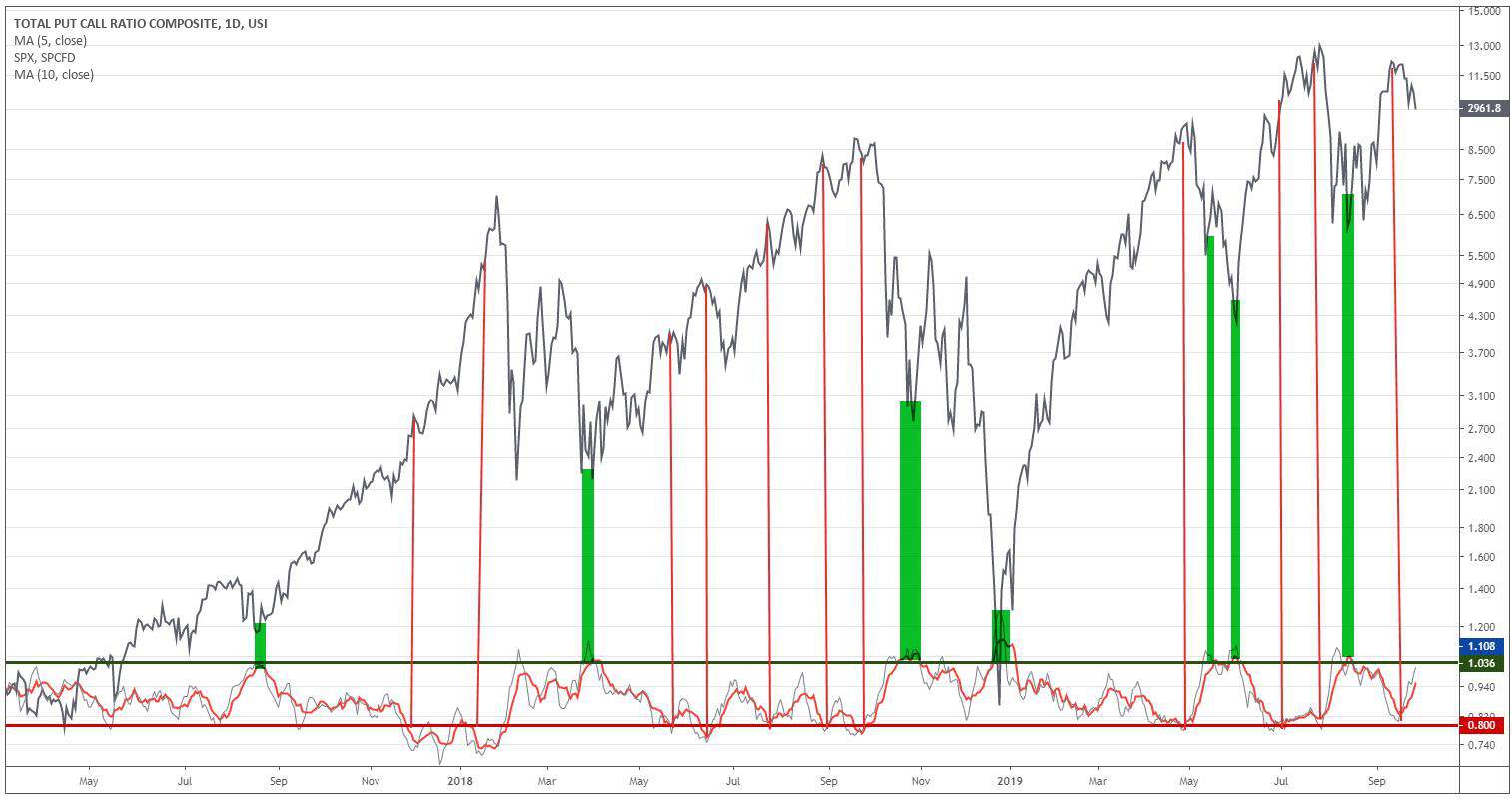

- Both NASI and NYMO (McClellan summation and oscillator indexes) triggered sell signals this week telling me that the overbought levels I noted two weeks ago (link here) are still being worked off. I’m looking for more downside over the next week or two. And with the increased tape bomb risk floating around, make sure you’re keeping your head on a swivel and managing your risk tight.

- My base case remains that this decline will be laying a trap for bears, of which there seems to be a growing number — did you know that #recession2020 is a trending tag on Youtube? Apparently all the big social media influencers are making videos about how to prepare for the coming crash. I think I’ll fade that… Anywho, our near put/call sell signal from 2-weeks ago has mostly reversed and it looks like we may see a firm buy signal triggered (red line crossing above green horizontal) in the next couple of weeks should the market take more of a dip here.

- This would be great since it’d bring down our other sentiment/positioning indicators (the MO Sent/Pos Composite indicator is still a bit too elevated for my liking). I’d like to see Extreme Exposure flatten out as we saw at the previous three bottoms.

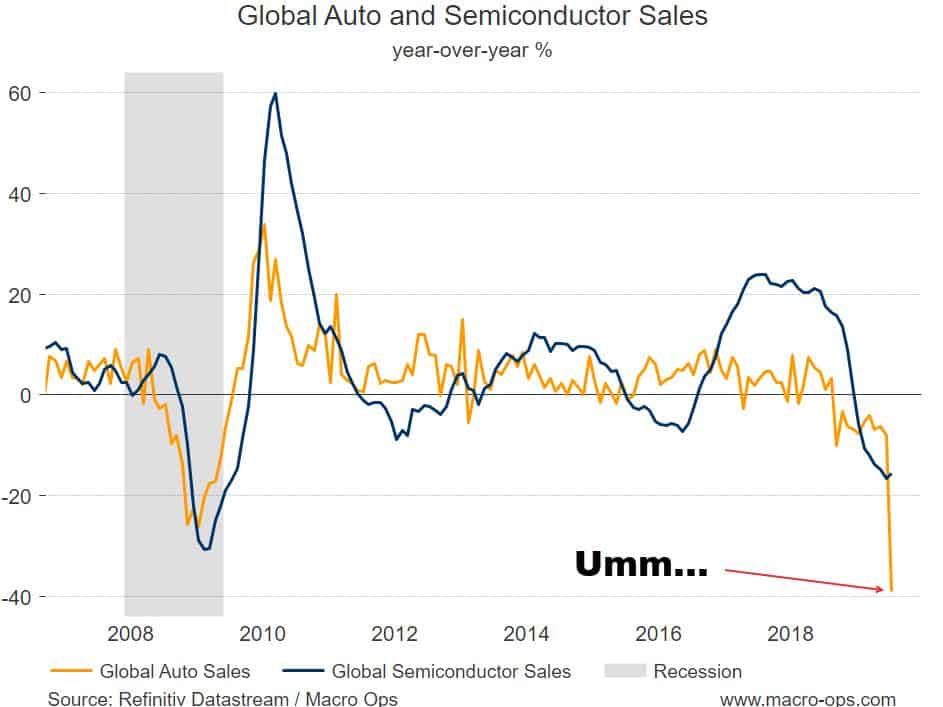

- This chart, is, um… quite the sight. Global auto sales have fallen some on a YoY% basis. Semiconductors haven’t been doing too hot either.

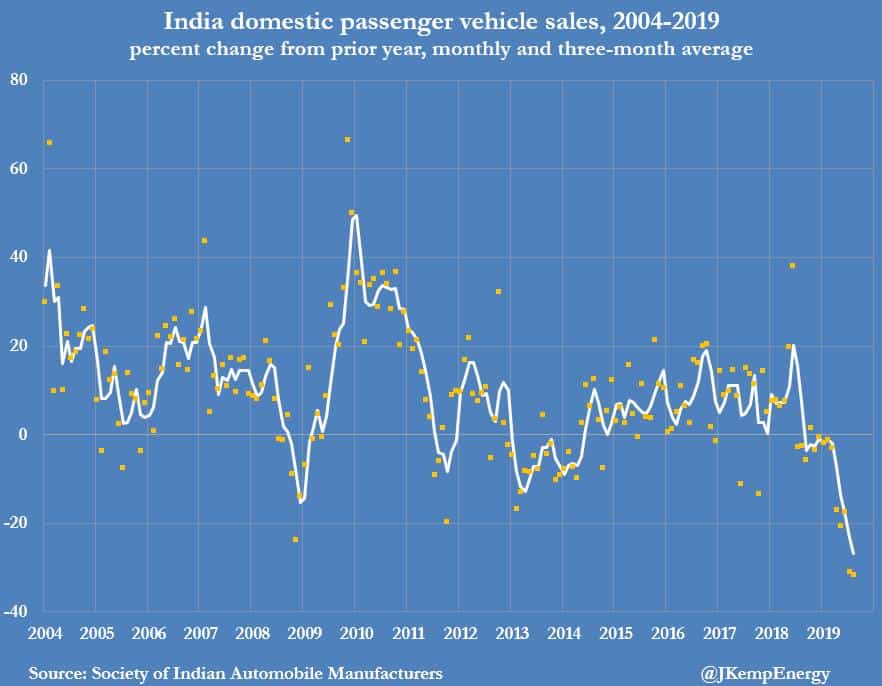

- Where is this big drop in global auto sales coming from? Well, it’s due to a number of factors. Both China and Germany changed their emission regulations recently which led to car buyers in both countries deferring purchases (this drove the largest YoY% collapse in China’s auto sales over the last 30-years). Plus, there’s India who also recently saw their largest fall in vehicle sales in nearly 30-years.

Unlike China and Germany, India’s lack of demand for autos is due to a liquidity crunch that was sparked by the collapse of a major shadow bank which has tightened consumer lending in the country. This, along with the general slowdown in China, is what’s behind the global manufacturing recession (chart via @JKempEnergy).

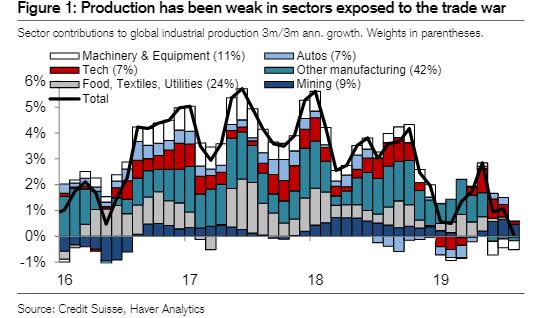

- We can see the drag from autos on global industrial production below (chart via Credit Suisse).

- The slowdown in China and the collapse in auto sales have reverberated across the global economic system, dragging growth and trade down with it. The share of PMI New Export Orders has been falling for the last 18-months and now sits at its lowest point since 2012 (chart via NDR and CMG Wealth).

- Germany has been one of the hardest hit from the global manufacturing recession since their economy is so dependent on high-end exports (autos especially). Corporate profits in the country recently saw their largest YoY% decline since 2013 (chart via Credit Suisse).

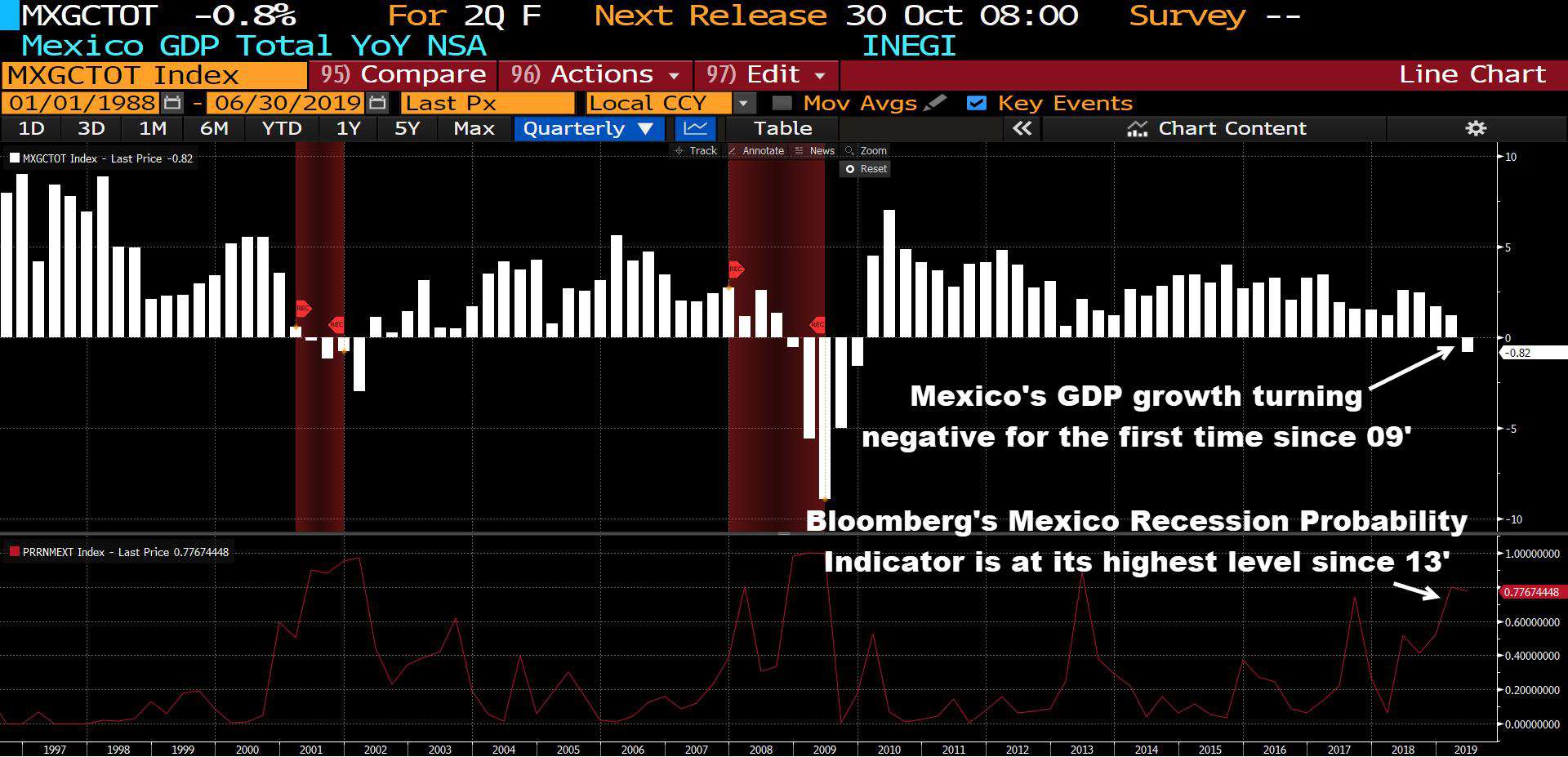

- Mexico, whose economy is extremely exposed to the global swings in manufacturing and trade, just saw its first negative YoY% drop in GDP since the GFC. The Bloomberg Recession Indicator is signaling the highest probability of a recession in Mexico since 2013.

- And with tariffs set to rise substantially going into the end of the year, the trade war sure isn’t helping things (chart via Credit Suisse).

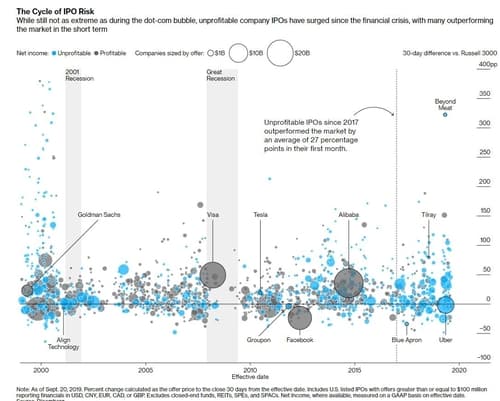

- We’ve seen a surge in the number of unprofitable companies IPO’ing over the last few years. But it still pales in comparison to the bonanza we saw at the height of the tech bubble (chart via Bloomberg).

- “What has been will be again, what has been done will be done again; there is nothing new under the sun.” ~ Ecclesiastes