My brain… it cannot process failure. It will not process failure. Because if I sit there and have to face myself and tell myself, ‘You’re a failure’… I think that’s almost worse than death.

…

I create my own path. It was straight and narrow. I looked at it this way: you were either in my way, or out of it.

…

We can always kind of be average and do what’s normal. I’m not in this to do what’s normal.

…

We all have self-doubt. You don’t deny it, but you also don’t capitulate to it. You embrace it.

…

Pain doesn’t tell you when you ought to stop. Pain is the little voice in your head that tries to hold you back because it knows if you continue, you will change.

…

Everything negative — pressure, challenges — is all an opportunity for me to rise.

~ Koby Bryant, RIP

Good morning.

In this week’s Dirty Dozen [CHART PACK] we look confirmed sell signals in equities, revisit the indications of overbought and overloved stocks, and then reiterate our long bond call.

***click charts to enlarge***

- Friday’s bearish engulfing candle may have signaled the beginning of a 5%+ correction in US equity indices. Last week’s price action reversed the overthrow from the 4-month rising wedge after briefly passing above the important 3,300 level — which we talked about here. Some buyers came in right before Friday’s close, creating a decent sized tail. Momentum like that which we’ve seen over the last few months typically does not turn on a dime. So there’s a chance we see a small bounce early in the week. But a move below Friday’s low would portend a continuation of the down move which should play out over the coming weeks.

- It also happens that we’re moving into the meat of earnings season this week. Here are the most anticipated earnings releases via Earnings Whispers.

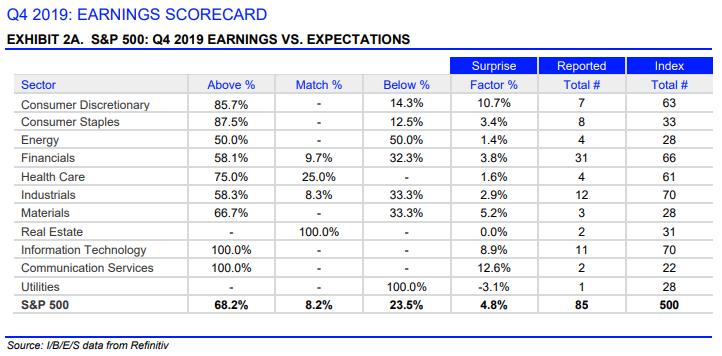

- Earnings are expected to decline by 0.5% this quarter. Of the 85 companies in the SPX that have reported, 68.2% have beat analyst estimates, above the long-term average of 64.9% but below the prior four-quarter average of 73.5%. So far, there have been 77 negative EPS preannouncements issued by SPX companies and 35 positive EPS preannouncements.

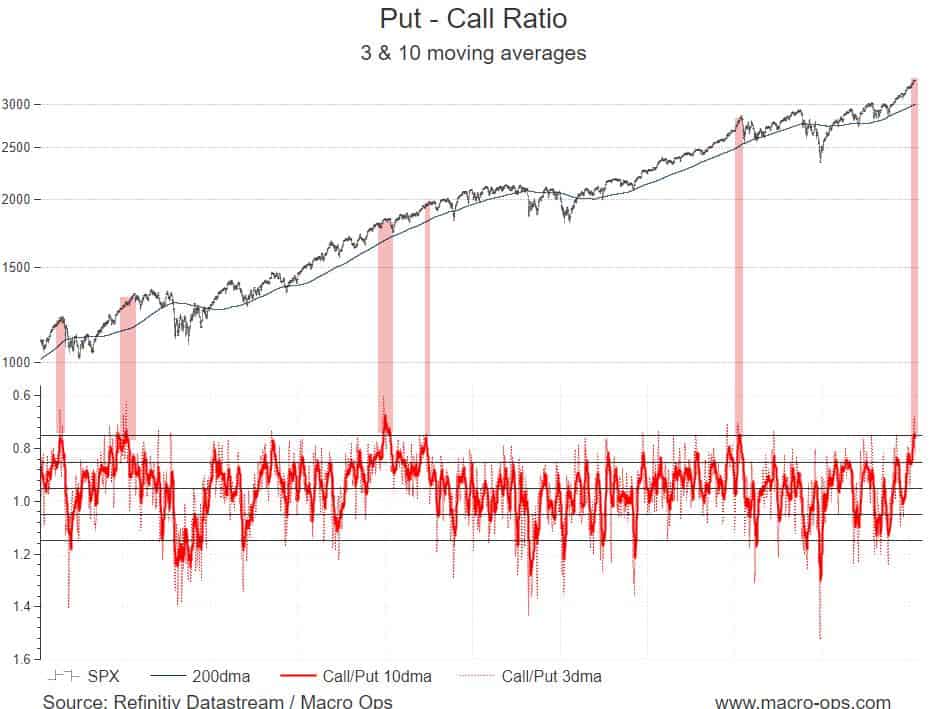

- The selloff is likely to extend to over 5% due to (1) the technical overbought conditions of this trend (2) the buildup in complacent positioning (see chart below) and (3) valuation levels which are now a significant headwind. The 3&10 day moving averages of the Call/Put ratio is over 2std’s above its average — one of the most extreme readings this cycle — meaning investors are buying a lot more calls relative to puts. The highlighted red zones mark past instances where the indicator was near current levels.

- The SPX’s Forward PE is now 19x. This is the highest valuations seen this cycle, with only January 18’ coming close. Valuations are now an increasingly large headwind for stocks.

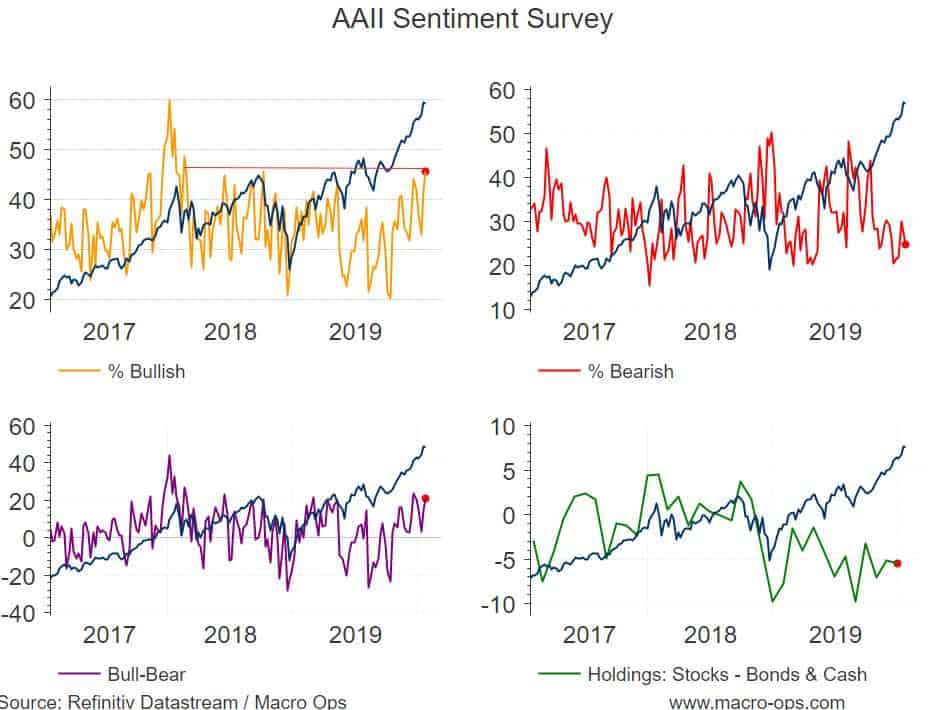

- Retail has finally decided that now is a good time to become incredibly bullish. AAII Bullish Sentiment just hit its highest levels since January 18’.

- And Investors Intelligence shows that “Advisors” last week became their most bullish on stocks since October 18’, right before the large selloff in the equity market.

- This chart from Morgan Stanley shows that cross-asset volatility is back near 15-year+ lows. Low vol regimes lead to high vol regimes. And we’re nearing that point where things can’t get much better.

- The McClellan Summation index (NASI) triggered a sell signal on Friday. Highlighted red zones mark past occurrences.

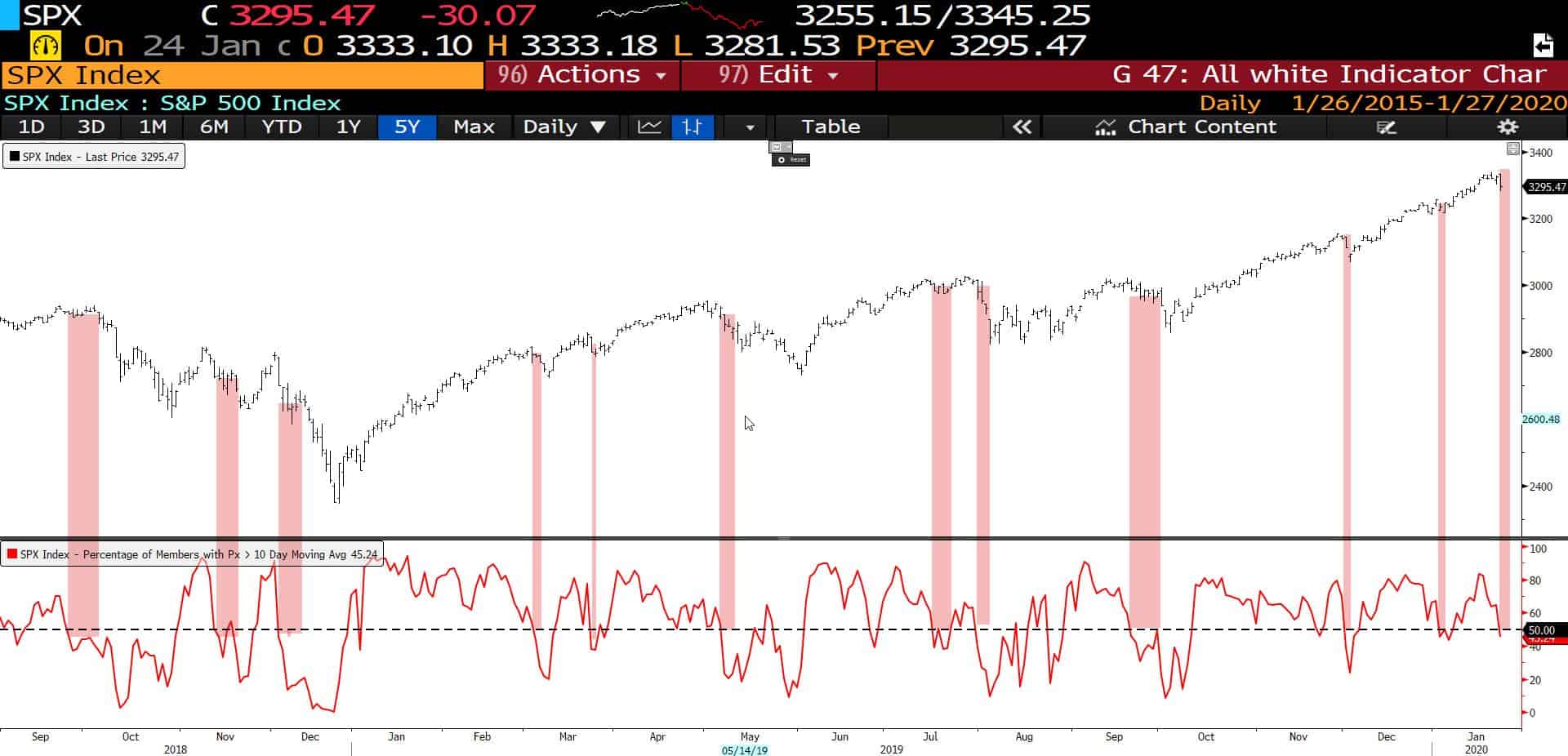

- Breadth has kept me from turning bearish on this rally but that is now starting to change. The percentage of stocks trading above their 10-day moving averages just crossed below 50%. This is a precondition for a larger sell-off.

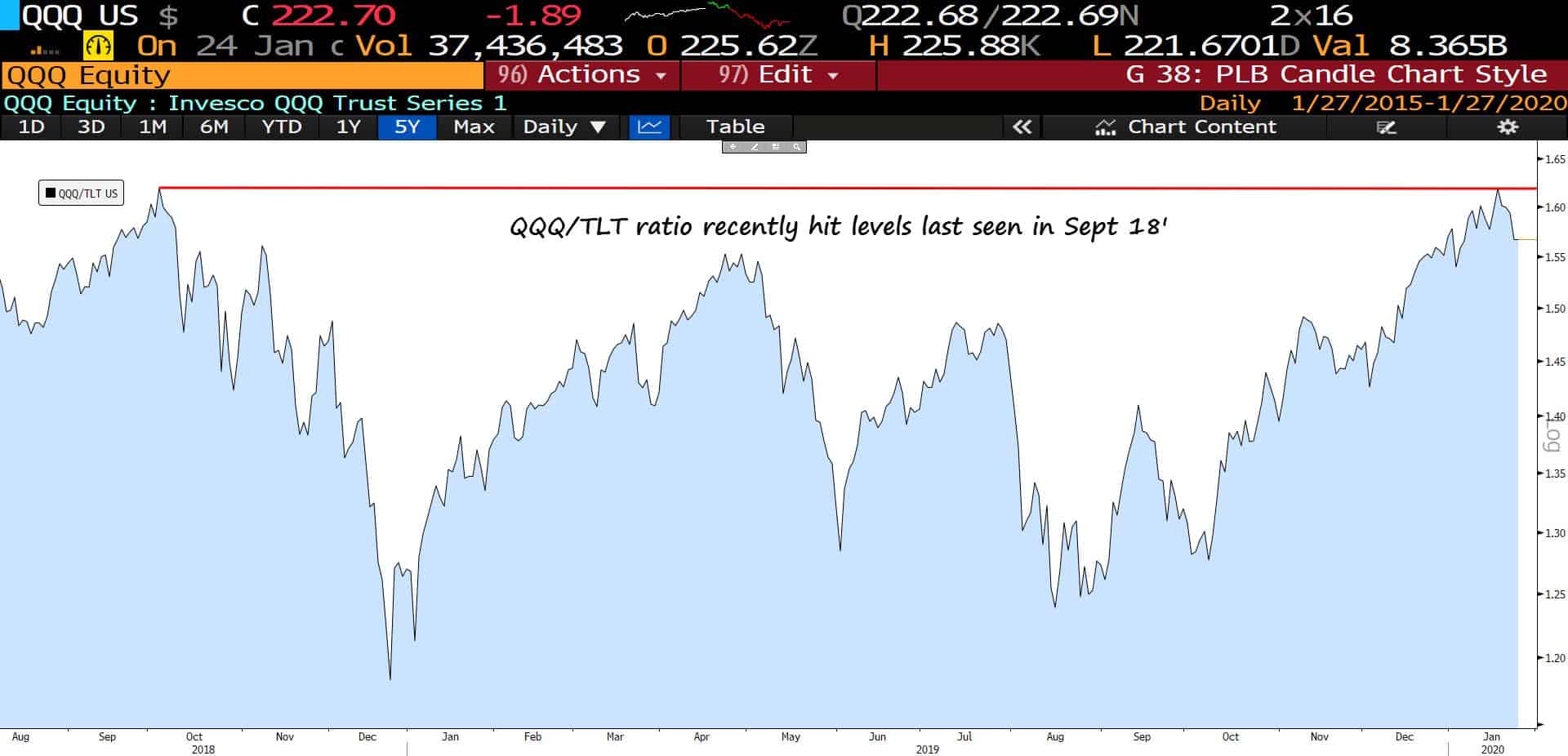

- The Nasdaq / Bond (QQQ/TLT) ratio recently hit its highest mark since the end of September 18’. My money is betting that we see some mean-reversion here.

- Bonds confirmed their breakout from their descending bullish wedge last week (ZB_F, TLT). I recently raised my bond position from 100% of NAV to 200%. Bonds also have copper/gold and positioning in their favor, which I tweeted about last week here.