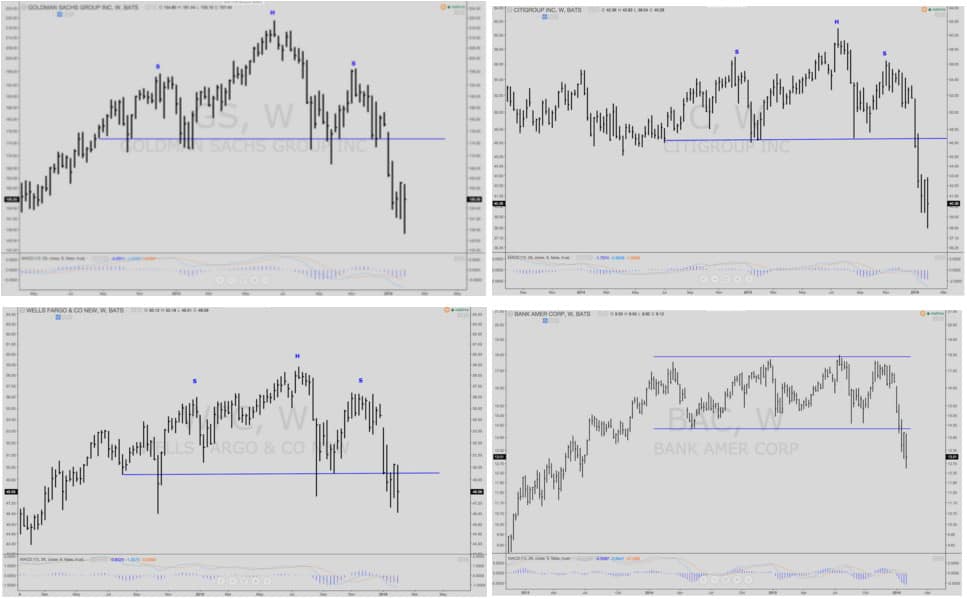

U.S. financials have been taken to the woodshed over the last month.

Many bank stocks are either in a bear market, or very close to one. They look disastrous from a technical standpoint. As you can see in the charts below, various banks have formed long-term topping (bearish) patterns that indicate a likelihood of further downside.

|

Bank Name – Ticker |

Percentage (%) off 52-week High |

|

JP Morgan Chase (JPM) |

-18.05% |

|

Bank of America (BAC) |

-29.30% |

|

Citigroup (C) |

-34.48% |

|

Wells Fargo (WFC) |

-18.16% |

|

Goldman Sachs (GS) |

-28.52% |

This has come as a surprise to many… as the popular narrative at one time was that banks would benefit from the Fed raising rates. There was also plenty said about how much safer and well capitalized bank balance sheets had become.

And with many of the big banks trading under book-value, it became a consensus trade to go long financials after the Fed raised in December. Seems like a logical bet, right?

Unfortunately, the dynamics currently driving the collapse in banking stocks are a little more complex than the narrative above.

But before diving into the real drivers, let’s quickly review the banking business.

Banks take money from depositors and pay them a low rate of interest in return. These deposits are liabilities on the bank’s balance sheet. The liabilities need to be matched with assets. Assets vary from higher yielding loans (money lent out to customers), to mortgage backed securities, and even treasury bills.

The way banks make their money is on the spread between the interest paid to depositors and the yield collected on assets. This spread is called the net interest margin, or NIM for short. Without NIM, banks would not exist… it’s their lifeblood.

Many thought a rate hike would be bullish for banks because it “should” increase NIM — thus boosting earnings.

This mechanism works because even though a rate hike increases both the yield on a bank’s assets and the interest paid to depositors, there is normally substantial lag between the two. Banks can generally keep the deposit rate low for an extended period of time while the yield on their assets increase from raised rates. This translates into higher NIM.

This mechanism makes sense and is not where the banks’ problems come from. The rate hike may indeed cause higher NIM in the short-term.

Instead, the real problems in the sector have to do with two broader issues that pose a risk to future NIM.

These are:

- The market’s belief that the Fed is tightening into a weakening economy and that it’s making a horrible policy error.

- The market’s belief that the Fed will be forced to reverse course and bring rates back to the zero bound or even go negative.

The first belief is centered around the fear that the global economy is weakening. This is something we’ve written quite a bit about and strongly agree with. And if this is the case, then increasing the cost of borrowing is likely to have disastrous effects. The outcome would do far more harm to the financial sector than any benefits accrued from a measly 25bps rate hike and its effect on NIM.

The second belief is all about the market losing faith in the competency of the Fed. The Fed was forecasting four additional rate hikes this year, with another four in 2017. The market is currently only pricing in one rate hike in 2016. The Fed’s word doesn’t mean much anymore.

And this is more than just an example of the Central Bank’s failed policy of forward guidance. It’s also an example of the market calling the kettle black and realizing that this business cycle is overextended. The market is betting that the Fed walked itself into a corner with its own policies.

The recent backlash from the markets and prominent economists against the Fed’s possible mistake has seemed to have had an impact. Some FOMC members have since suggested that perhaps the Fed’s planned rate trajectory is a bit aggressive considering the broader weakness across the globe.

The Foundation team believes there’s a high probability that the US will actually see negative rates long before another increase. This poses a big threat to banks.

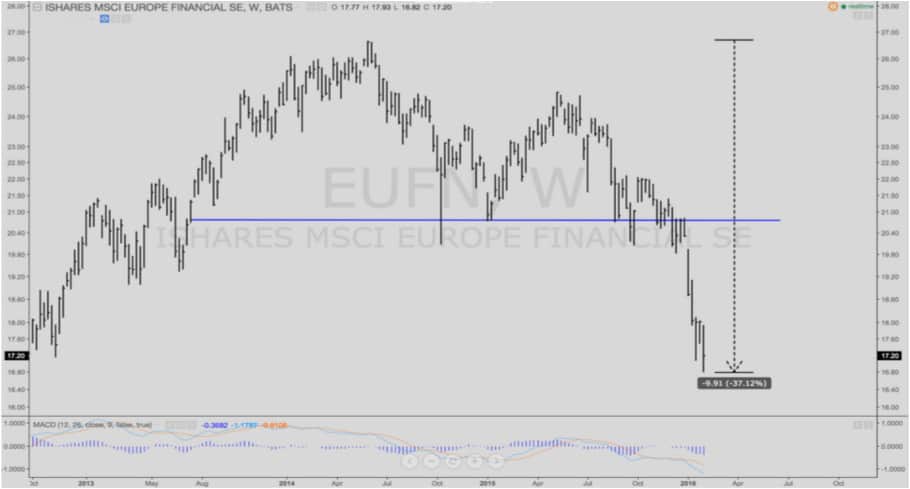

The damaging impact of negative interest rate policy (NIRP) can be seen in Europe, where many of the continent’s largest banks are trading near multi-year lows.

Negative rates eat away at NIM. They’re an abomination to the basic tenets of capitalism. Their disastrous impact is also exacerbated by new regulations determining the type and quantity of assets a bank must hold. This kind of environment forces banks to buy negative yielding assets while charging depositors to hold their money. That’s not a great combination for a bank’s bottom line.

In a NIRP environment, operating a bank becomes a negative-carry trade with no real upside. It’s not an appealing business model.

So this is where financials now find themselves. Essentially, they’re forced between a rock and hard place.

On the one hand there’s the potential for a short-term increase in profits from higher rates. But this comes at the cost of a higher probability of global economic turmoil.

On the other hand is a contraction in NIM that would come from the Fed reversing its policy and kicking the can down the road. This would result in the high possibility of NIRP and the destruction of the basic tenets of banking.

Both of these scenarios are terrible for banks. Staying away from their shares seems like a pretty good idea to us. And going short a select few seems like an even better one.