Narratives are a fundamental part of our human existence. They’re the key to how we process information. Just as the mind instinctively searches for visual patterns in nature, it also seeks to derive patterns and meaning from information flow. We create stories to help us understand.

We see this in financial markets all the time, though it’s not always a good thing. You’ve heard the talking heads on CNBC. They hop on camera and try to attribute every little market gyration to one news story or another. This type of narrative creation doesn’t make much sense. Most of the day-to-day movement in the markets is just noise.

But pull back a bit and you can see where narratives become useful. For example, why has gold been on a tear since the beginning of the year? Its narrative revolves around the loss of faith in central banks. Investors have stopped believing in their ability to support and stabilize markets and the currency. And so they turned to gold for safety.

With a narrative like this, you have the ability to isolate a core driver. You can find the main point that drives the entire story. Gold is ripping because of a loss of faith in central banks. The loss of faith is the key driver. Other factors aren’t important.

Defining drivers is essential to proper analysis because it gives you an idea of what to pay attention to. If the key driver changes, you know the entire narrative will change. This shields you from noise and let’s you focus on what’s important.

You can take this concept and apply it to any investment thesis. An asset will move based on one or two key drivers, often wrapped up into a nice little narrative.

An area where investors frequently fail to do this is with equities. They mainly focus on peripheral factors without ever nailing down true drivers. Maybe it’s because value investing is so popular? Investors believe they can create alpha by analyzing asset depreciation or tax rates or some other small factor. Now sometimes these are the main drivers, but not usually. Investors tend to forget the forest by focusing too much on the individual trees.

One great example of this is Apple. You’ll often catch investors analyzing the effect of the company repatriating its cash reserves, or the potential of its entrance into the automobile market. These things may be fun to talk about, but they are not the real drivers of the stock price…

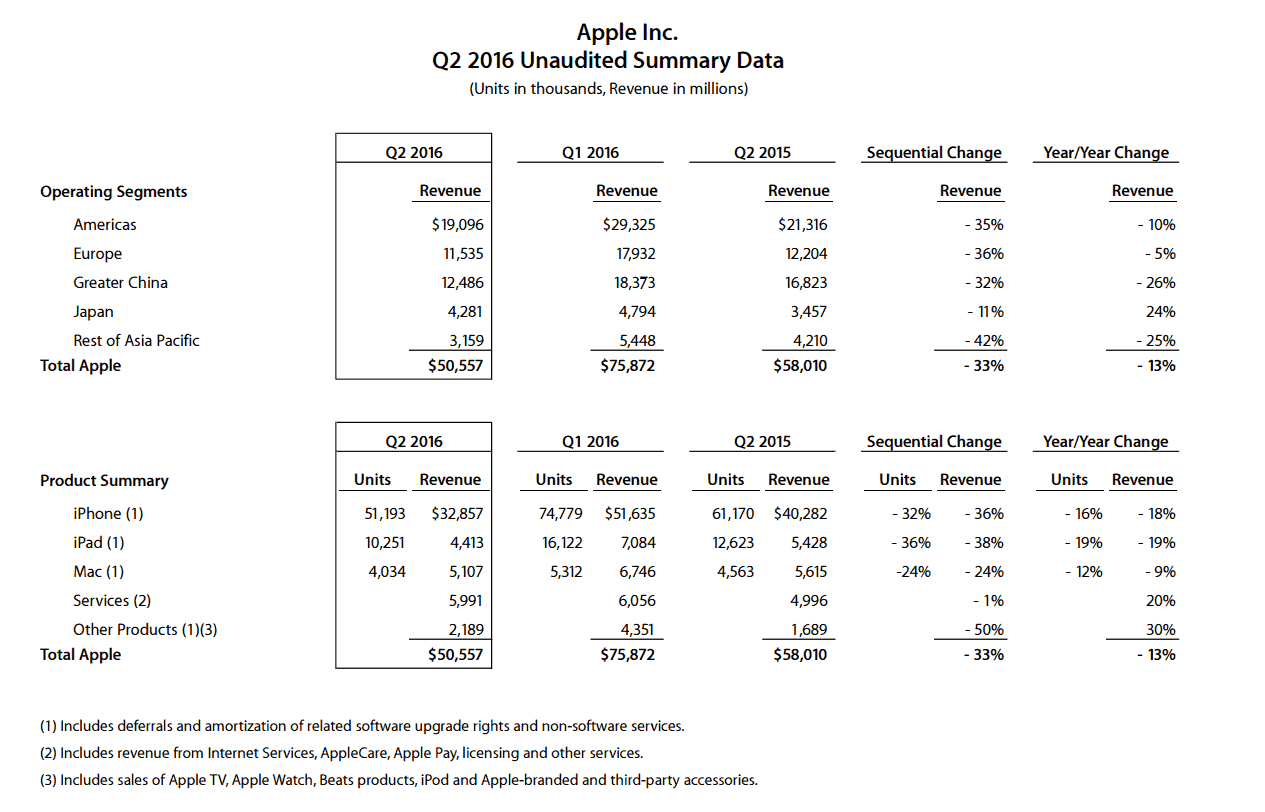

Apple’s stock price depends on iPhone growth. Take a look at their most recent sales breakdown:

Out of the $50.6 billion in revenue Apple made in Q2, $32.9 billion came straight from the iPhone. That’s over 65%… the business clearly depends on this one product.

But if you look at year-over-year sales, they’re decreasing. There was an 18% drop in iPhone revenue from 2Q 2015 to now. This was far worse than analyst estimates and is a large cause for concern given that the iPhone drives the company’s share price.

The problem is that the smartphone market is maturing. Most people who want a smartphone already have a smartphone. Revenue in Q2 of 2015 for the Americas, Europe, and Japan is less than it was in Q2 of 2014. This is a blatant sign that these markets’ demand has matured.

And with no new demand, Apple is left to compete against itself for upgrades. But according to CEO Tim Cook, the underwhelming Q2 report was due to a significantly slower iPhone upgrade rate.

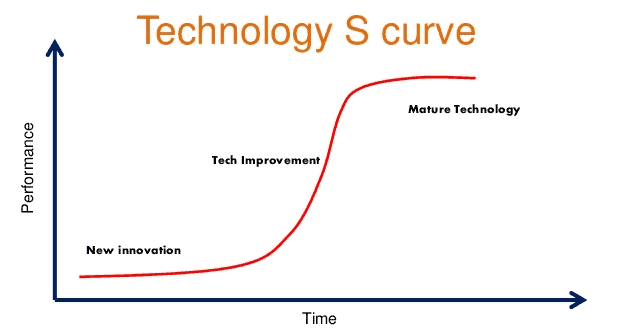

Why are upgrades slowing? It’s because not only is the smartphone market maturing, but smartphone technology itself is maturing. It comes down to the technological S-curve. As Benedict Evans explained:

A technology often produces its best results just when it’s ready to be replaced — it’s the best it’s ever been, but it’s also the best it could ever be. There’s no room for more optimisation — the technology has run its course and it’s time for something new, and any further attempts at optimisation produce something that doesn’t make much sense.

The development of technologies tends to follow an S-Curve: they improve slowly, then quickly, and then slowly again. And at that last stage, they’re really, really good. Everything has been optimised and worked out and understood, and they’re fast, cheap and reliable. That’s also often the point that a new architecture comes to replace them. You can see this very clearly today in devices such as Apple’s new Macbook or Windows ‘ultrabooks’ — they’ve taken Intel’s x86 and the mouse and window-based GUI model as far as they can go, and reached the point that everything possible has been optimised. Smartphones are probably at the point that the curve is starting to flatten…

Smartphones have gotten as good as they’re gonna get. This is why users aren’t rushing to upgrade like they used to. What are you getting with newer models? A slightly better camera? A fingerprint scanner that is a bit faster than the old one? There’s not much that’s really worth the upgrade anymore.

It’s inevitable. Every technology goes through this same process. The hardware matures and causes the upgrade cycle to lengthen, thereby choking off growth. We saw it happen with both PCs and tablets. Smartphones are no exception.

So how is Apple management trying to solve this maturity problem?

They’re going all-in on China.

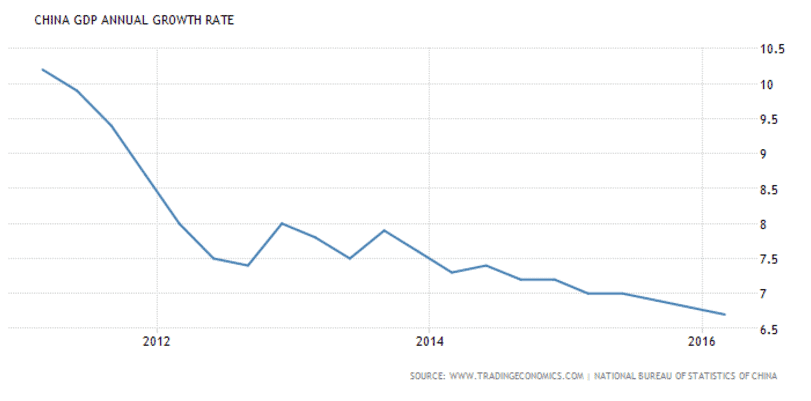

China is the last hope for the tech giant’s iPhone growth. Its economy is big enough to move the needle on Apple’s bottom line. But if you’ve been following the macro situation in China even a little bit, you know the picture is “lukewarm” at best. And “mad max” at worst.

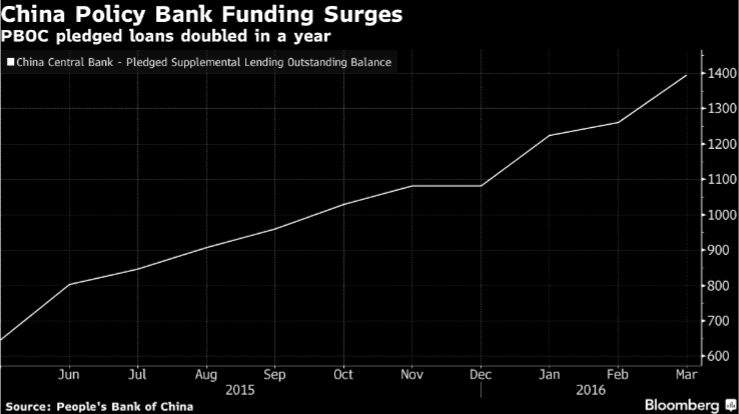

China has been spastically hitting the credit needle in a desperate attempt to juice stagnating growth.

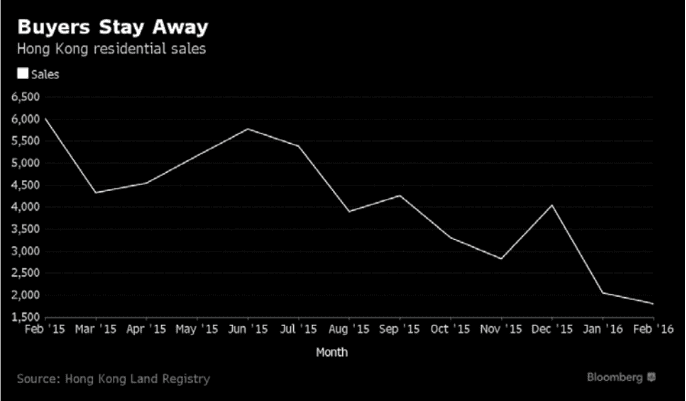

Pledged loans continue to rise with no end in sight. But it’s just not helping anymore. The property market has cooled off despite the liquidity injections.

And the stock market is in the gutter.

While growth hasn’t had an uptick in forever.

This deteriorating macro picture is already showing up in Apple’s earnings.

In the recent Q2 report, revenue from China actually dropped 26% year over year. The China growth strategy is clearly not going as planned.

Carl Icahn recently closed a large position in Apple for this very reason. Not only was he concerned about China’s growth, but also their excessive regulation. As Icahn explained:

“You worry a little bit — and maybe more than a little — about China’s attitude. [The government can] come in and make it very difficult for Apple to sell there … you can do pretty much what you want there.”

China recently shut down both Apple’s iBooks store and iTunes Movies. Their relationship with the company is quickly souring, making sales even tougher.

In a feeble attempt to placate the crooked Chinese regime, Tim Cook recently plowed a billion dollars into Chinese ride-share company Didi Chuxing. But from what we know about the Chinese government, this is most likely a sucker’s play. Since the advent of the modern internet, the Chinese have been copying U.S. IP and banking off it while banning US companies from operating in the country. We don’t expect them to “soften up” on Cook just because he put a billy into one of their companies.

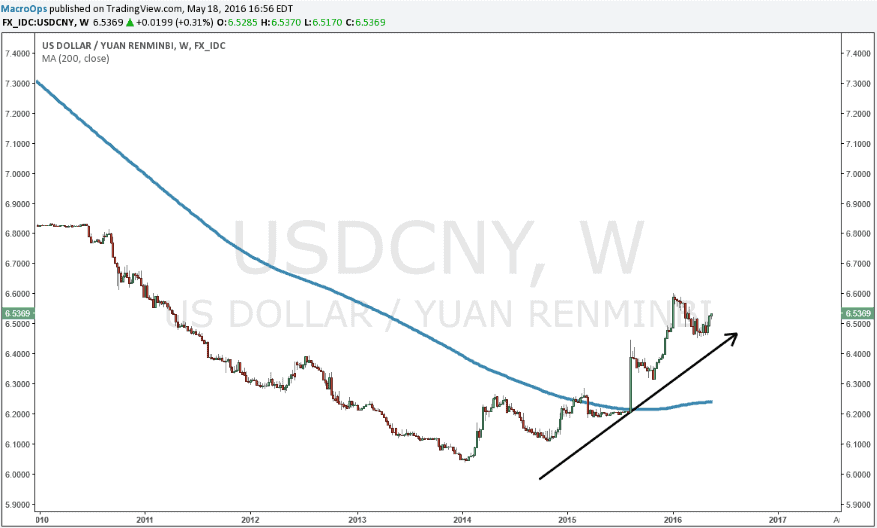

And we can’t forget about USD strength either. That trend has not gone away by any means. The Chinese devaluation of the yuan is also still very much on the table.

The Reminbi put in a decisive higher low and continues to weaken against the United States dollar.

One thing’s for sure. A weakening yuan will not bode well for Chinese iPhone sales. Apple is incredibly exposed to foreign exchange risk in China.

It’s funny because as the Apple story continues to become more bearish, we are now seeing Warren Buffett jump into the foray with a $1 billion stake in the company.

Buffett in tech stocks? Seems backwards right? Normally he avoids tech companies because they don’t have defensible positions. Their moats aren’t big enough. Our team at Macro Ops absolutely agrees with him on these points. Technology changes too quickly to have a significant moat.

Buffett’s mantras of “Invest in things that don’t change” and “If you won’t own it for 10 years, don’t own it for 10 minutes” don’t work too well in the tech space where disruption seems like an everyday occurrence. And the pace of this disruption is only accelerating. Good luck trying to predict tech trends 10 years out. It’s not even a stretch to say that Apple becomes irrelevant in the next decade… that’s just the nature of the market these days.

With his mentality, Buffett’s Apple investment is surprising. But so is his other tech investment in IBM. It’s true that both companies have significant cash flows, but they’re also both on the decline. Especially IBM who missed the entire cloud revolution as companies like Amazon blew by them. Most of IBM’s “engineering” has been of the financial sort with share buybacks pumping up their executive bonuses. They’re a far cry from the dominant tech company they used to be.

Fortunately, you can make better investments than Buffett in the tech space. At this point, Apple looks like a stock we wouldn’t touch with a 10-foot pole. Its brutal transition from growth stock juggernaut to blue chip value has been a tough one.

Now we don’t recommend shorting stocks like Apple because there is cash flow and the valuation is fair. But we absolutely don’t want to be long the stock either. Apple is what we call a “dead money” stock. It’s a lumbering sleepy giant that churns and grinds sideways for years and years. Think of Microsoft after the ‘99 bubble deflation.

Your money will be better put to work elsewhere. Something that has the potential to move a lot and actually pay you a respectable dividend yield.

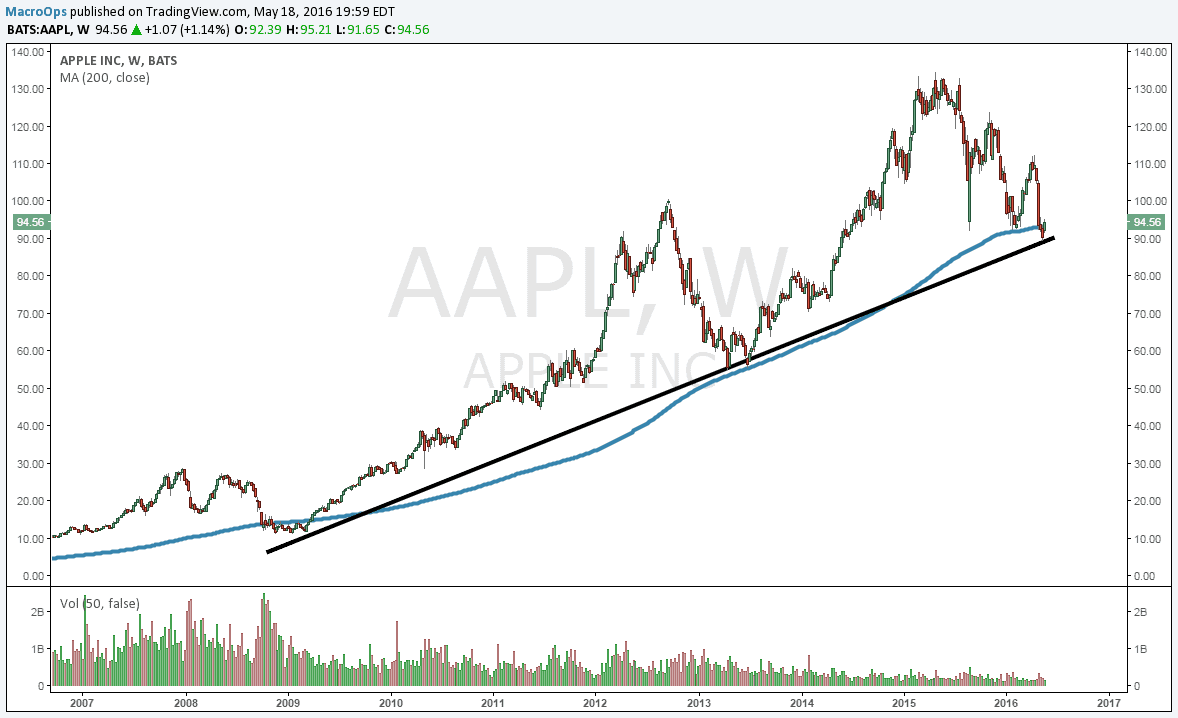

To top it off from a technical perspective, Apple has broken down from an 18-month topping pattern and is about to challenge its long term trend line.

Remember to always focus on key drivers because they will reveal clarity in a complex situation. For Apple, free cash flows or tax issues are not important to the stock price. With a maturing smartphone market and their only potential source of growth (China) nearing economic armageddon, Apple’s stock price is due for a long grind sideways frustrating both bulls and bears.