The following is an excerpt taken from our latest weekly note that was sent to Macro Ops Collective members.

We’re going to cover a lot in this week’s report. We’ve got trade wars, trade wars, and some more trade wars… Regulatory action against tech giants… A look at sentiment and technicals which are setting up for a significant bottom… And finally, we’ll walk through the major macro indicators to dispel the nonsense being peddled about an impending recession… Oh, and then we’re going to cover some trades that are teeing up… Pour yourself a fresh cup of joe, strap in, and let’s get cracking.

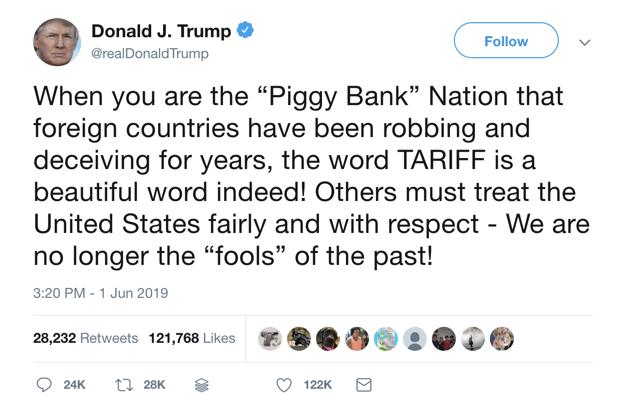

I don’t know about you but I want me some of whatever President Trump is smoking. The Donald has been non-stop these last few days.

Growing bored with an escalating trade-war with China he — apparently on a whim — decided to start one up with our Mexican Neighbors in an effort to get them to do something about their porous borders. Despite the fact that we just signed a major trade deal (USMCA or New Nafta) with them last December which took over a year of negotiations to hammer out.

Not wanting to stop there he then decided to remove India’s “special trade status” which exempted the country from US tariffs and followed that up with an effort to hit that thieving Australia with tariffs of their own before being talked back amid fierce opposition from military officials, as well as the State Department.

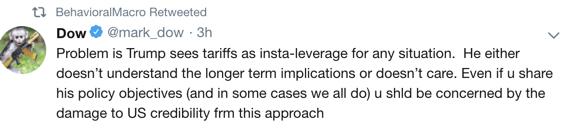

It looks like Trump has become besotted with the total discretionary authority that tariffs give him. No checks and balances, no going through Congress; he can wield near instantaneous economic force from his smartphone. Macro Hedgie Mark Dow summed up the implications of this well, tweeting:

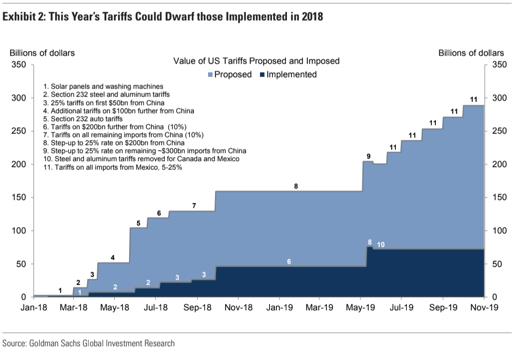

Goldman Sachs shared their revised expectations of the trade war’s impact this weekend, writing:

We now expect a 10% tariff rate by July on both the final $300bn of Chinese imports (60% subjective odds) and on all Mexican products (70% odds for the first 5%, and just over 50% odds for the step-up to 10%).” For China, this represents a middle ground between our previous assumption of a delay following the G20 summit in late June and the full 25% across-the-board tariff proposed by the US Trade Representative.

Additional tariff rate increases or an across-the-board auto tariff are also possible but not our base case. We still expect deals with China and Mexico to lead to a removal of the tariffs, but not until late 2019/2020.

We don’t have an edge in figuring out what the Trump admin or those on the other side of his trade fury will do. GS’s expectations are as good as any. They calculate that this base case will impact inflation, where they see it “climbing from 1.57% in April to 2% in August and to 2.3%-2.4% in early 2020” and dinging GDP growth in the second half by roughly 50bps.

Precise numbers aren’t that important here, in my opinion. What matters more is how this continues to widen the Cone of Uncertainty, not only for investors but for participants in the real economy. This is where the real risks lie, which are two-fold. These are (1) that this trade war escalates and creates a bear market of unnecessary stupidity which, due to the financialization of the economy, then leads to a recession and/or (2) private fixed investing (capex) collapses due to an inability for businesses to plan which then leads to a profits recession in accordance with the Levy-Kalecki framework.

As an example. Here’s some comments included in the recent Dallas Fed Manufacturing Survey (emphasis mine).

Primary Metal Manufacturing

- The possible increases in tariffs related to China will negatively impact our agriculture customers and put further pressure on a segment that is already experiencing cyclical lows.

Nonmetallic Mineral Product Manufacturing

- There are many unknowns due to tariffs.

Machinery Manufacturing

- There has been a sharp decline in orders, and pricing has taken a huge dive as well. Competition has pushed pricing to near-guaranteed losses.

- With all the tariff fees pouring into the U.S. Treasury, when should we expect a tax break?

- We are seeing steady business that should begin to grow again if a China trade deal is reached.

- China tariffs were already causing significant price increases, and the latest escalations will raise our costs even more—probably our prices, too—and make us less competitive on the world stage where we export 70 percent of what we produce.

Computer and Electronic Product Manufacturing

- Trade talks with China could have a longer-term impact but have no impact at this point.

- Growth is robust and would be even stronger without current supply chain and labor constraints, but we aren’t complaining.

- With our government’s intention to resolve issues with Iran and China and also introducing the “Deal of the Century,” it adds warranted risk to our future business that we can’t ignore.

- There is significant uncertainty.

Transportation Equipment Manufacturing

- We are changing our business model to increase volume, with pricing based on wholesale margins versus retail margins. This change is to be phased in over six months.

- Our primary customer is the U.S. government. We continue to be concerned regarding the volatility of the decision-making processes at the higher levels.

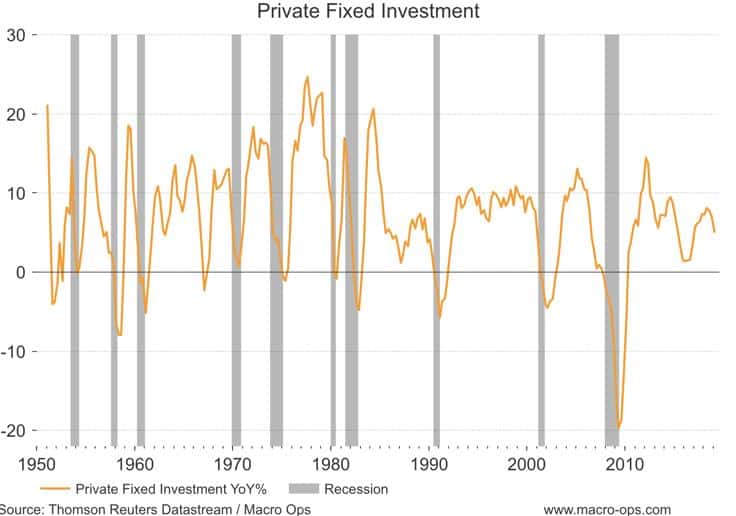

Net investment is what drives profits over the long-term. Growing regulatory and trade uncertainty makes operators less willing to make long-term investments. Private fixed investment is still growing at a healthy clip of 5% in the most recent quarter. But it’s also rolled over from its most recent high reached in Q2 of last year. If the trade war escalates and we see this number continue to fall then we’ll maybe want to start battening down the hatches.

The Regulators are Encircling the Tech Giants

Here’s a few sections from a recent article by Reuters (link here).

(Reuters Breakingviews) – At some point, antitrust investigations of Google and Amazon.com AMZN.O become a no-brainer. As a step in that direction, the Federal Trade Commission and Justice Department, which police U.S. competition issues, have divvied up responsibility for the tech giants, according to news reports. That could create ammo for future fights. Facebook FB.O ought to worry too.

… Splitting jurisdiction between the FTC and DOJ – which have overlapping remits – is a logical way to clear the decks. It avoids overloading one agency, duplication of work, and bureaucratic infighting. It will also leave each to explore different approaches to big questions like how troves of data on users and suppliers affects competition – something on which regulators worldwide are feeling their way.

Politics also raises the stakes, notably at the DOJ, which was already scrutinizing social media firms for alleged bias against conservatives after pressure from President Donald Trump. Antitrust scrutiny of Google has been informed partly by competitors’ complaints, including those by Oracle ORCL.N, whose Co-Chief Executive Safra Catz served on Trump’s transition team.

In the past, U.S. regulators have failed to make a dent on Google and software giant Microsoft MSFT.O, and they may achieve little again. These investigations could, however, establish important precedents that, a few years from now, inform more dramatic skirmishes.

The popular high-growth tech names are getting hammered on this news. This thread does a good job of laying out the implications of this. Basically, high-growth tech/SAAS plays have been the ONLY game in town these last few years. They’ve become hedge fund hotels where positioning concentration has reached ridiculous levels + when you couple that with the rather low volatility and high momentum we’ve seen in many of these names, you get a ‘fire in a crowded theatre’ type scenario where a bunch of weak hands end up clambering for the exit at the same time.

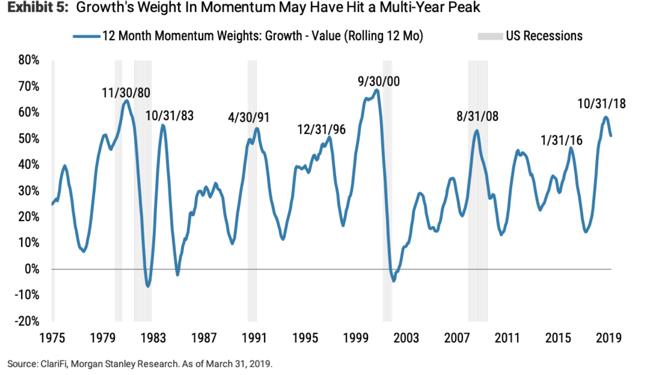

I wrote about the shift that’s underway from growth to value in last month’s MIR (link here). [For access to this content sign up to the Macro Ops Collective by Monday June 9th!]

Here’s one of the charts from that report showing the cyclical swing between growth/value on a momentum basis.

We’ll be looking to put out shorts in a few of these Icarus stocks in the coming weeks.

Slowing Growth but NOT a recession…

It’s been a few weeks since we’ve taken a macro fundamental look at the US market. And since I’ve seen a lot of screaming and hollering about an impending recession I thought I’d dust off a few of our mainstay recession indicators to see if that’s a high-probability risk. The short answer is, of course, no.

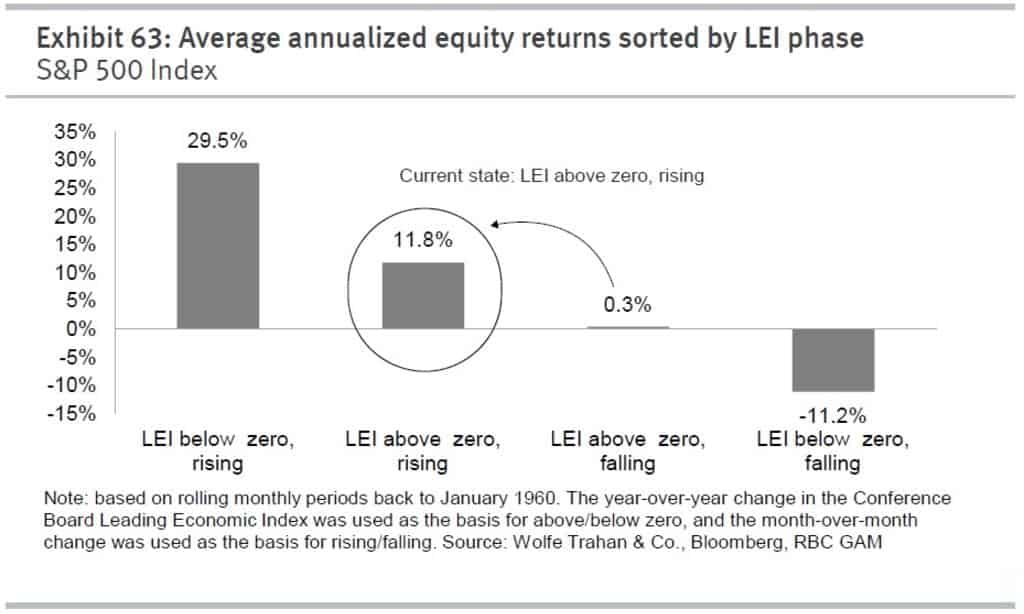

Let’s start with the Conference Board Leading Economic Indicator (LEI). The LEI is a composite of 10 leading economic and market indicators. You can read more about it here.

The LEI has given an advance signal of all eight recessions since its inception in 1959. It peaks on average of 10.5 months before a recession comes. The graph to the right shows the average returns per state of the LEI.

The chart below, which exhibits the LEI on an absolute and YoY basis, shows that the indicator is still heading up and to the right, though at a more muted pace.

Let’s turn now to labor. There’s a lot of ways to slice the jobs market but we’ll look at two of the stalwarts that I prefer — the other labor indicators I keep an eye on tell the same story.

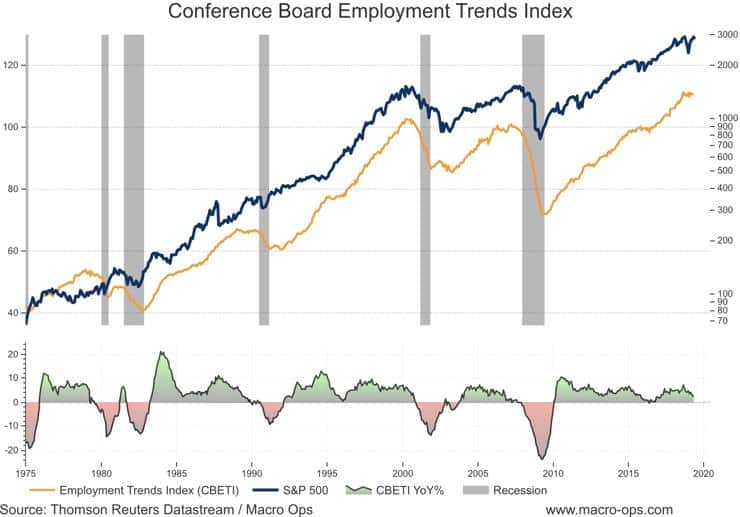

The first is the Conference Board Employment Trends Index which, like the LEI, is an aggregate of eight labor market indicators (you can read more on it here).

The chart below shows that it peaked on an absolute basis back in August of last year and has flat-lined since but is still positive on a 12-month basis. We shouldn’t be worried though until this indicator turns negative.

Then we have Temporary Help Service Payrolls on a monthly, quarterly, and yearly basis. After a brief soft-patch at the start of the year, the data is back in the black showing positive growth. This indicator will turn over and begin to bleed a lot of red before a recession rolls around (see 00’ and 07’).

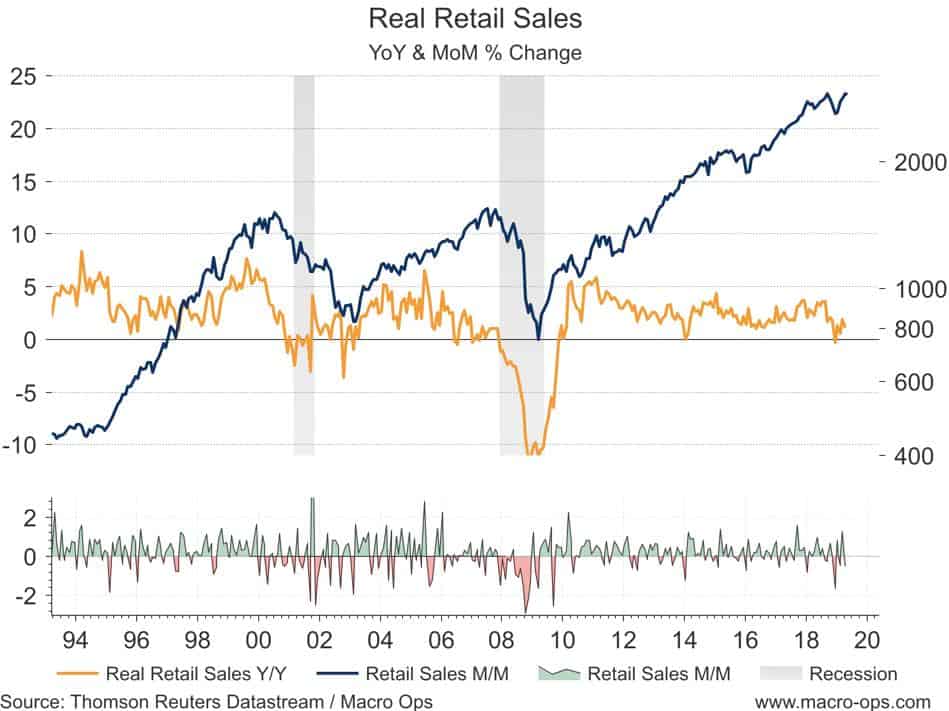

Inflation-adjusted Retail Sales are another reliable leading indicator for the economy and though growth has slowed it’s still positive. If it rolls over and continues lower from here then we’ll have to start getting concerned.

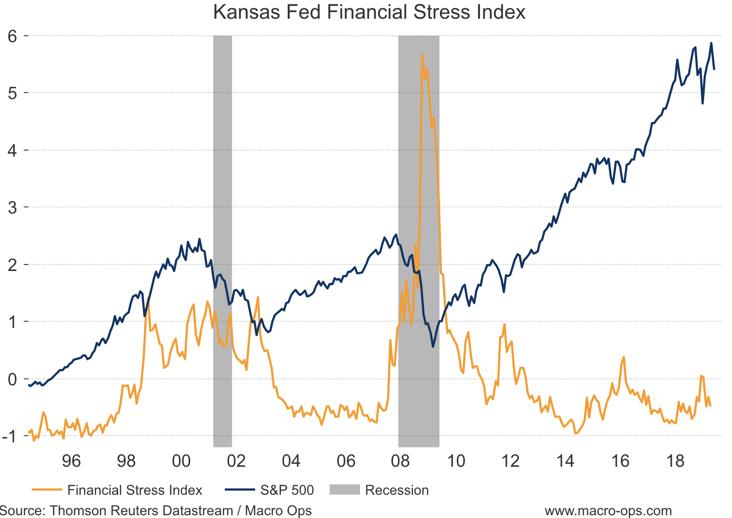

Lastly, let’s take a look at financial conditions (aka. liquidity). Like the labor market, there’s a lot of ways to gauge liquidity. We’ll look at a few of my favorites like this one, the Kansas Fed Financial Stress Index (KFSI) which is comprised of 11 financial market variables (read more here).

The KFSI is very muted, showing easy financial conditions. This indicator will turn and spike higher in the lead up to a recession, as it did in the summer of 07’ and 99’.

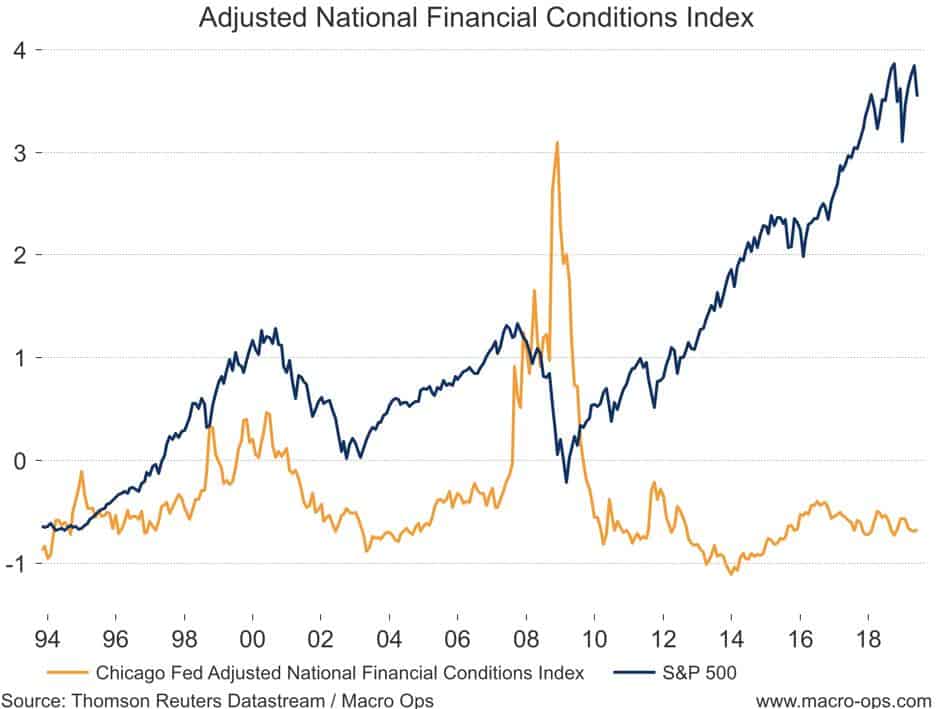

The Chicago Fed Adjusted National Financial Conditions Index (ANFCI) summarizes 105 indicators of financial activity (read more here). Like the KFSI, this indicator is trending sideways and near very low levels, showing easy financial conditions despite the recent bout of market volatility.

So we have uptrending LEIs, a strengthening labor market, positive real retail sales, and easy financial conditions. The bears will say “what about the inverted yield curve!?”.

A yield curve inversion does have a reliable track record of predicting recessions but my answer to that is threefold (1) an inverted curve should not be dismissed, but we need to look at the evidence in its totality and not just select one data point that confirms our bias (2) the signaling utility of parts of the curve may be somewhat less reliable this cycle, as I’ve noted here and (3) parts of the curve are still positive, such as my go-to, the 10-2s.

With all that said, our base case is that growth will continue to slow (we predict real GDP growth for the year to come in around 1.5%).

Slowing growth is not a recession and a low growth / low inflation economy is not a bad environment for risk assets as Stanley Druckenmiller has pointed out numerous times.

The major thing we look at is liquidity, meaning as a combination of an economic overview. Contrary to what a lot of the financial press has stated, looking at the great bull markets of this century, the best environment for stocks is a very dull, slow economy that the Federal Reserve is trying to get going… Once an economy reaches a certain level of acceleration… the Fed is no longer with you… The Fed, instead of trying to get the economy moving, reverts to acting like the central bankers they are and starts worrying about inflation and things getting too hot. So it tries to cool things off… shrinking liquidity… [While at the same time] The corporations start having to build inventory, which again takes money out of the financial assets… finally, if things get really heated, companies start engaging in capital spending… All three of these things, tend to shrink the overall money available for investing in stocks and stock prices go down…

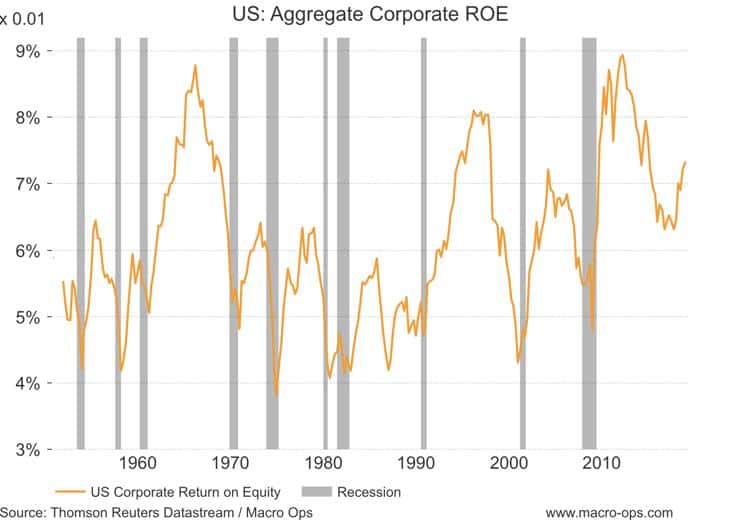

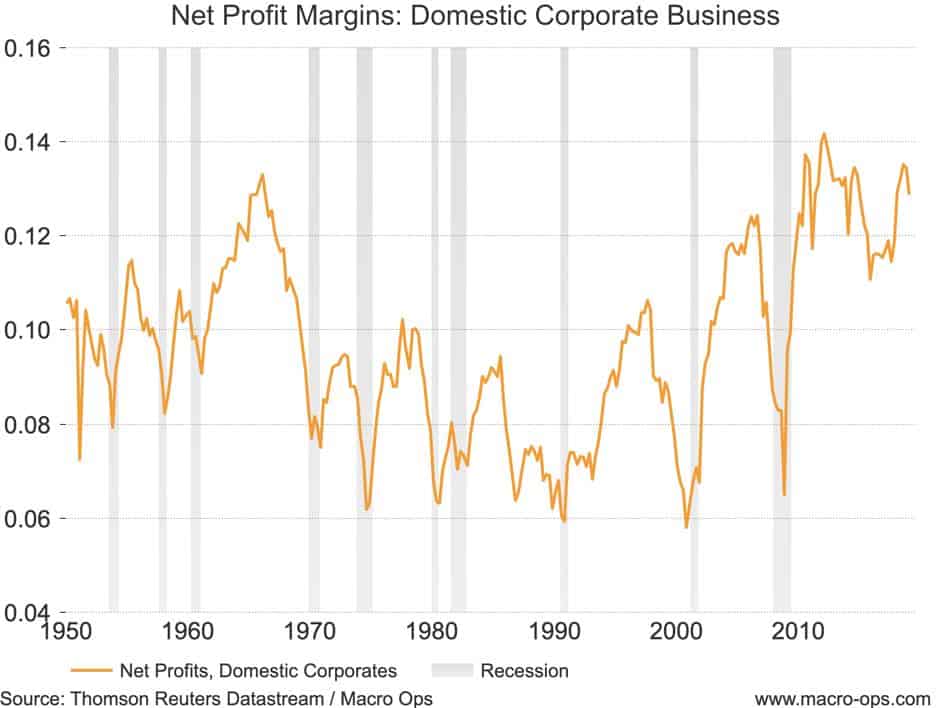

Oh… I also want to point out the trend in US Profit Margins and Return on Equity (ROE). Both are important to watch as they directly drive equity valuations.

Starting with ROE, we can see that following an extended contraction that began in 12’ it’s actually begun to trend back up after bottoming in 17’. ROE will typically compress in the lead up to a recession.

Net US Profit Margins also peaked in 12’ but are still holding up pretty well. Like ROE, we will see margins compress in the lead up to a recession.

In our next piece, we’re going to cover the Market Trifecta: Fundamentals, Technicals, and Sentiment.

We’ll discuss how consensus earnings growth expectations have been walked down to much more manageable levels, then I’ll show you how key markets are nearing major support levels, and finally finish with a look at sentiment and positioning which is indicating that we’re nearing a significant bottom (ie, a big buying opportunity is setting up).

I’m seeing a LOT of wildly asymmetric trading opportunities that are teeing up. We have energy and shipping names trading for 1x normalized FCF, major FX pairs that are about to break out of significant compression zones, and bonds which are keyed for a big reversal. I’ll write more about these in a coming note for Collective members.

That’s all I got for now. If you would like full access to all of our research including the exact trades we are taking to navigate through the Trump tariff fiasco sign up to The Macro Ops Collective!

The Macro Ops Collective is our flagship research offering that will close down for new subscribers on June 9th at 11:59PM.