Westwing Group AG (WEW) is a home decor and furniture e-commerce business. The stock has at least 170% upside from the current price and is well-positioned to take share in an industry at the inflection point of its J-Curve adoption cycle.

Along with its structural tailwinds, the company is in the process of transforming its inventory to own-brand products. These products command 8-10% higher contribution margins. Over time, this translates to a significantly larger customer base buying higher-margin products, creating massive revenues and cash flows.

At the current price, Mr. Market is assuming WEW will generate no revenue growth over the next five years. We believe that this expectation couldn’t be farther from what will happen during that time frame.

Most investors will ignore this business. First, it’s German-listed, making most US-based investors unaware of the company. Second, value investors see a stock at new all-time highs thanks to a virus that pulled forward years of consumer growth and demand. Finally, German-based investors won’t show interest until they see consistent profitability and dividend history.

WEW is a highly addictive shopping experience unlike anything else on the Internet. Customers note that shopping at WEW feels like flipping through a personalized, curated home decor magazine filled with everything the customer wants based on what they like and previously purchased.

WEW is a highly addictive shopping experience unlike anything else on the Internet. Customers note that shopping at WEW feels like flipping through a personalized, curated home decor magazine filled with everything the customer wants based on what they like and previously purchased.

The company’s self-reinforcing curation model creates long-term users. 85% of the company’s sales come from customers who visit the site 100 times or more during the year. This addictive customer behavior makes sense.

The more that customers use the platform, the better the platform can refine the customer’s taste. More refined curation incentivizes the customer to return to the platform and buy more products.

New customers will find it hard to switch once WEW’s personalized curation kicks in. Moreover, increased purchase data allows WEW to identify its consumers’ most popular products and create own-brand versions at lower prices with better margins.

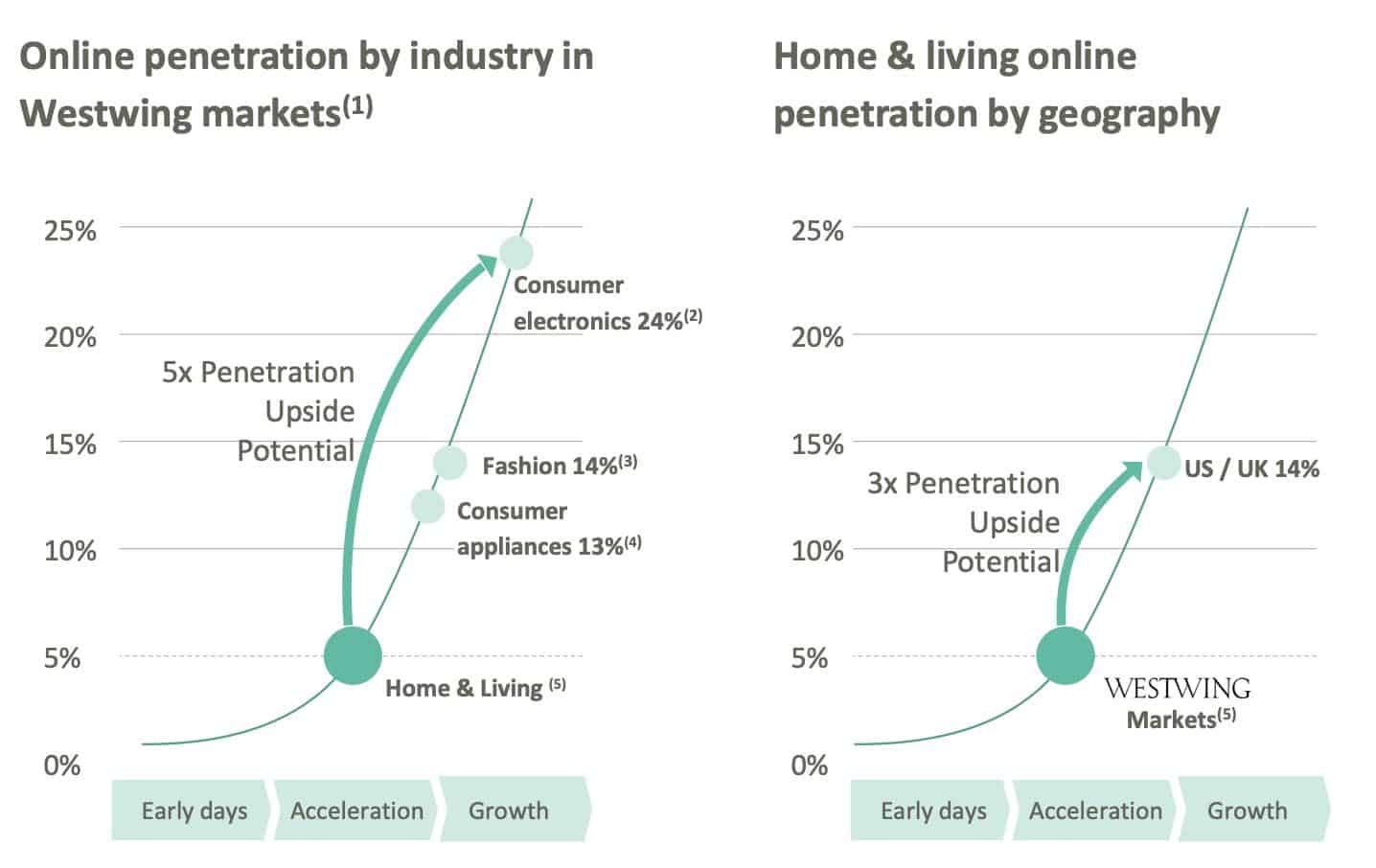

Finally, home & decor products sit at historically low e-commerce penetration rates (5%). A mere re-rating to consumer electronics penetration rates results in 5x growth. Moreover, WEW’s geographic markets are historically underpenetrated in home & decor online shopping. Re-rating to US/UK comps offers another 3x growth rate.

By 2025, WEW could generate over EUR 900M in revenue, 90M in EBITDA, and command a EUR 2.35B market cap. That’s 170% higher than the current stock price. Our base case, which assumes zero top-line revenue growth and steady-state EBITDA margins, is roughly the current share price.

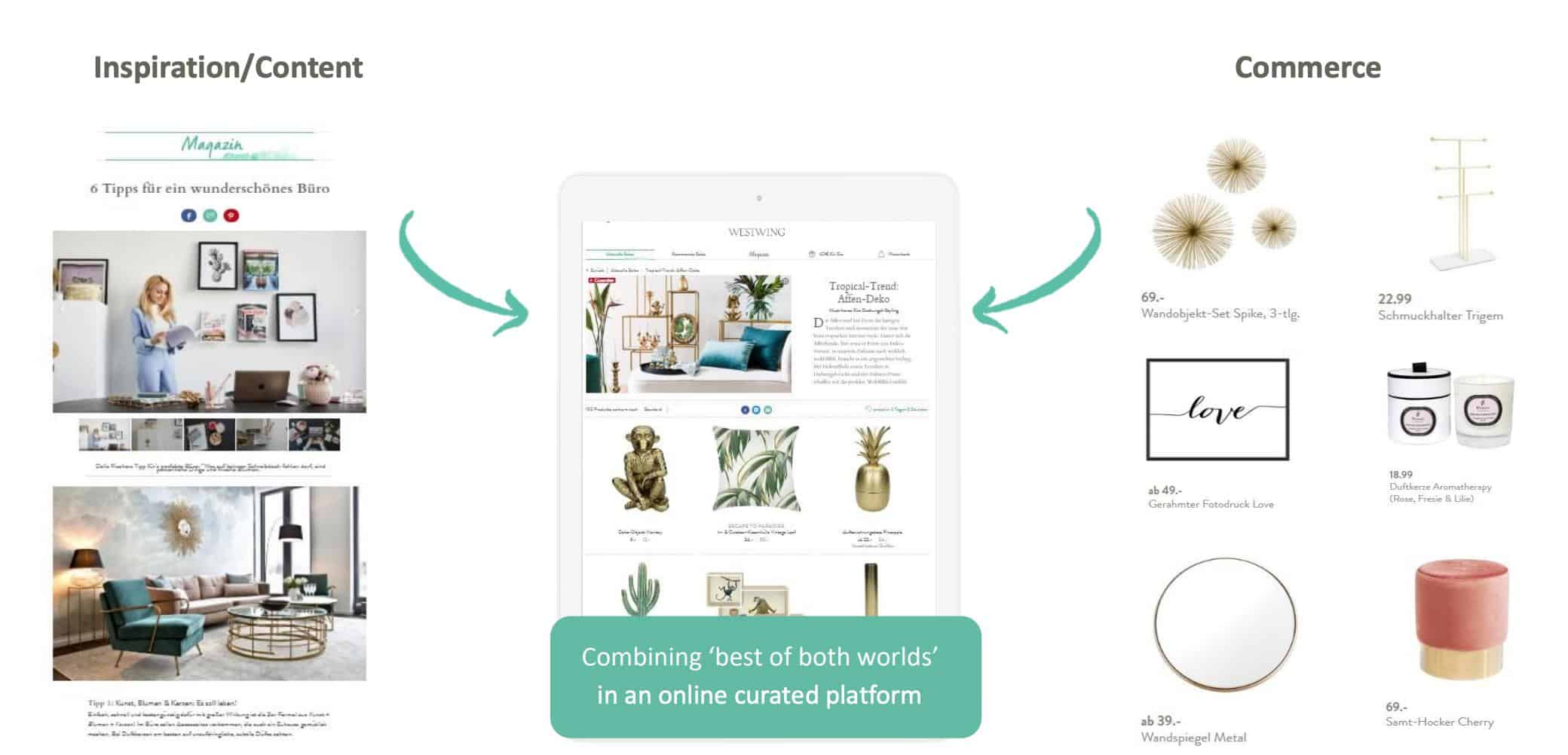

The Best of Both Worlds: Content & Commerce

WEW combines the best of both Inspiration/Content and e-commerce capabilities. Users don’t want to shop for home decor items the same way they shop for other goods. Furniture and other home items require “taste” and should match the rest of the home’s style.

It’s difficult for traditional e-commerce platforms to accommodate taste. Sure, you can search by type of product or make/model, but that’s not what home decor shoppers want. These shoppers desire style, a theme, and patterns that help express who they are. They want to be inspired.

Pinterest (PINS) is an excellent example of curating users’ boards based on what they’ve pinned in the past. Like WEW, PINS is perfect at capturing inspirations, leading their users to try new clothes, hairstyles, etc.

WEW does the same thing for home decor and furniture in an immersive, personalized online shopping magazine.

Inspiration leads most home decor purchases. Yes, you need a coffee table. But you don’t want just any run-of-the-mill table. You want something unique. A table that makes guests ask, “wow, where did you get this?”

A personalized online shopping magazine enables users to scan designs they love, then choose one that best fits their space. Each incremental purchase then makes the personalized curation feed that much better the next time they use it.

Hitting The J-Curve Inflection of Home & Decor E-Commerce

Despite COVID-19’s rapid user adoption acceleration, home & decor e-commerce penetration rates remain drastically low compared to other consumer goods and country-specific rates. Take consumer goods, for example. Consumer electronics sport a 24% online penetration rate, fashion commands 14%, and consumer appliances capture 13% of sales online.

Home & decor penetration rates, on the other hand, sit at 5%. Home & decor online penetration rates can 5x before reaching consumer electronics.

The other J-Curve inflection rests in geographic e-commerce adoption rates. WEW’s target markets have ~5% online penetration rates for home & decor shopping. Compare that to the US/UK’s online home & decor adoption rate of 14%. Again, there is plenty of room to grow in WEW’s target markets.

Low product and geographic online penetration rates act as dual rocket boosters to help WEW expand GMV, revenue, and profits.

Low product and geographic online penetration rates act as dual rocket boosters to help WEW expand GMV, revenue, and profits.

But there are a few reasons why online penetration rates remain historically low.

First, people that buy home & decor products are usually older than those purchasing consumer electronics. This means it takes WEW’s target customers longer to adopt new ways of purchasing these goods than, say, a new gadget for a teenager.

Second, home & decor shopping is inspiration-based, making it difficult to find a go-to online store to buy pieces. Customers might love the look of a lamp at one store yet want to buy their couch from another brand/style. Hopping from one site to the next to find what fits the room’s style creates friction for the end-user, incentivizing them to shop in-store.

Finally, home & decor products aren’t economically friendly for most e-commerce platform business models. Cliff Sosin of CAS Investment Partners calls these items “un-Amazonable.” You can listen to him explain the concept in our podcast. Large-sized furniture products need specialized logistics operations while margins compress as shipping costs eat away a traditional e-commerce platform’s profits.

Yet, it pays to capture the Home & Decor e-commerce market. US Home & Decor renders $250B in annual revenue (as of 2018). That dwarfs WEW’s EUR 117B addressable market.

WEW has captured a mere 0.5% of its addressable market despite massive COVID-led growth. Such a small market share means the company has plenty of room to expand.

Westwing’s Strategy: Capture Customers & Up-sell Own Brand Products

WEW generates massive amounts of data on its customers’ purchase habits. The data allows the company to see what its customers are buying, what they aren’t buying, and what’s most popular. WEW can then use this purchase data to create own-brand, high-demand products to sell directly to their customers on the online shopping magazine.

Let’s use an example. There’s a new, West Elm-looking chair that customers can’t stop buying. WEW sees this in their purchase data and decides to make their version of the product. The own-brand version is higher-margin for the company (usually 8-10 contribution percentage points) because they can cut out the middle man (third-party brand). That margin expansion is a big deal when you consider how quickly the company is growing its customer base.

The company currently generates 25% of its revenue from own-brand products. Over time, WEW expects to generate 50% of its sales from own-brand products. That’s serious operating leverage.

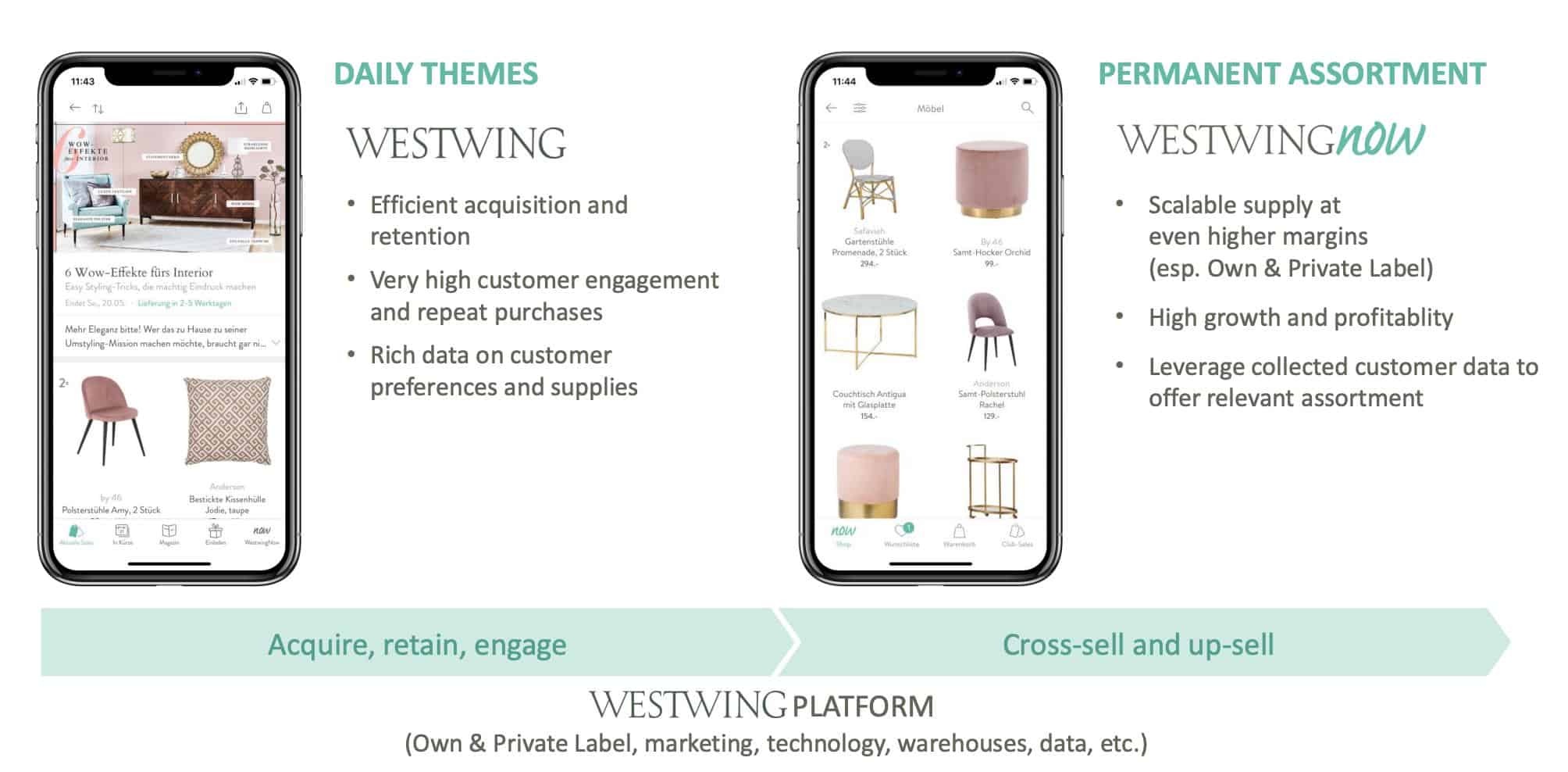

The company uses a two-step process to acquire, retain, and upsell its customers. First, WEW captures customers through its Westwing Daily Themes. Daily Themes allows customers to find new ideas and inspirations from myriad tastes and styles. WEW sends Daily Themes in an elegant emailed newsletter as well as on their website and mobile app.

The key to WEW’s business model is converting Daily Themes users into repeat customers that buy all their home decor through WestwingNow. WestwingNow showcases its bestsellers and all their own-brand/private label products in a beautifully designed shoppable experience. Each product comes with fast delivery and industry-best customer service.

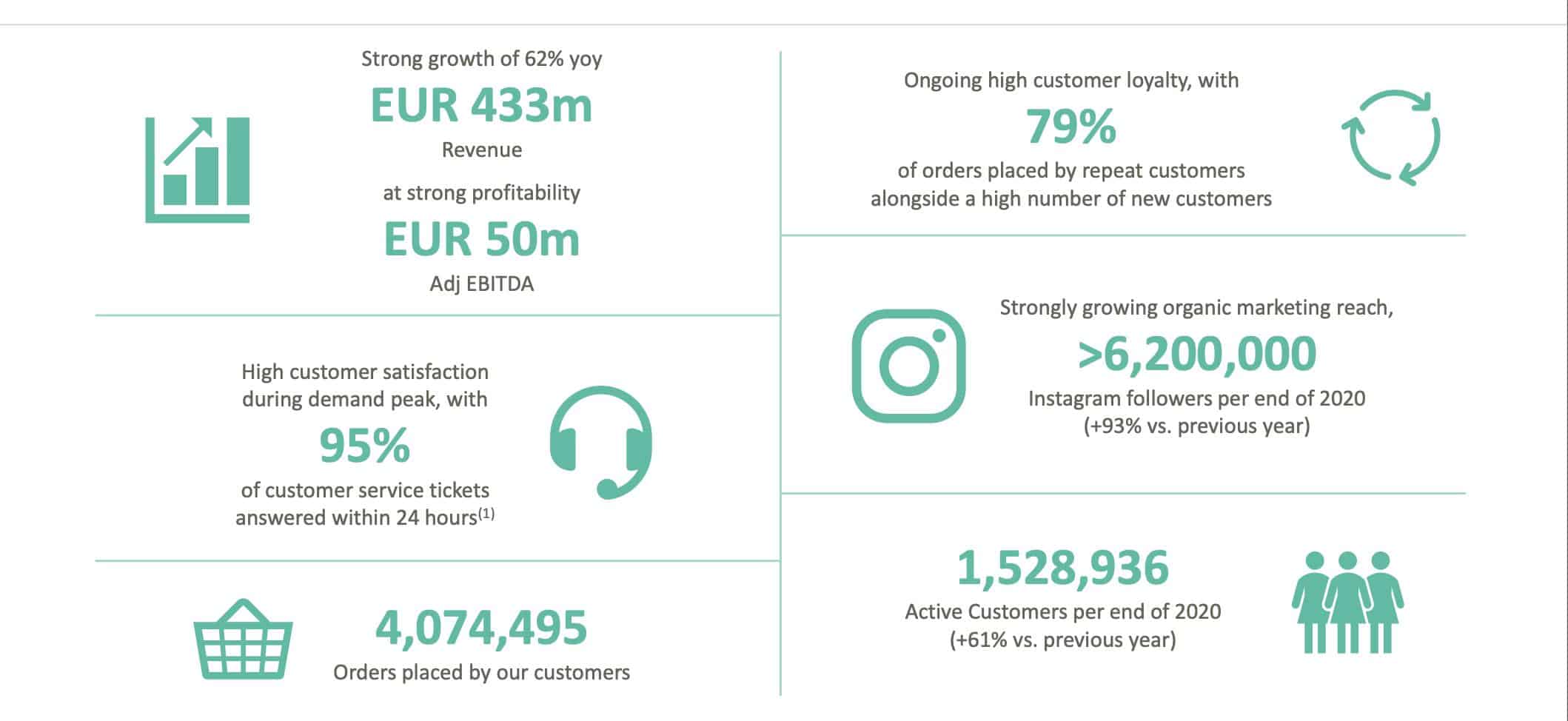

WEW grew its customer base 61.2% in 2020, from 949K to 1.53M. Moreover, the company now has over 5M Instagram followers. Customers stay with WEW for a long time. 80% of the company’s sales come from repeat customers.

And as of last year, the company generated 85% of its revenue from customers who visited their platform more than 100 times. Again, addictive customer behavior. Many WEW users report that the Westwing Platform is the first place they go when they wake up in the morning.

The biggest challenge for WEW is capturing more customers as they adopt an online-first home decor shopping habit. Fortunately, the company has two ways low-cost ways to grow its customer base:

- Engage with 5M+ existing Instagram users

- Promote the Westwing brand with high-profile people/influencers

Last year the company worked with Alex Riviere (800K Instagram followers), Nico Santos (singer/songwriter), and Sylvie Meis (1.4M Instagram followers) to promote the WEW brand and own-brand products.

Through its influencer partnerships, the company can quickly reach over 7M people at the lowest cost possible.

Thinking About The Future: What Will WEW Look Like In Five Years?

Let’s keep this simple. The company has ~0.5% of its market share. Can it reasonably double its current market share over the next five years? And how would they do it? WEW would have to grow revenues ~20% per year for the next four years to reach EUR 913M in revenue or 0.80% of its addressable market.

At steady-state, the company expects to generate 10% EBITDA and 7% FCF margins. That gets us EUR 91M in EBITDA and EUR 64M in FCF.

What would a reasonable buyer pay for this business in the public markets? Take a look at some industry comps:

- Wayfair (W): 49x EBITDA

- Amazon (AMZN): 22x EBITDA

- Zalando (ZAL): 31x EBITDA

- Overstock: 24x EBITDA

Let’s assume a buyer would pay ~25x EBITDA for WEW. That gets us EUR 2.275B in enterprise value. Add back EUR 76M in net cash on the balance sheet, and you get EUR 2.35B in market cap or EUR 115/share. That’s a 170% upside from the current price.

EUR 117/share could very well end up becoming our base case if the company continues to execute. Between 2013 and 2020, Wayfair (W) grew revenue by at least 30% per year. Plus, the market has shown that it will pay a premium for high-tech, curated e-commerce platform businesses. Buying WEW today feels a lot like buying Wayfair in 2013.

All The Ingredients For Aggressive Expansion

Let’s review the main catalysts:

- EUR 117B industry at the inflection point of its J-Curve adoption rate

- Tech-savvy millennials entering their prime buying years will use online-first experience

- Own-brand products will represent 50% of total GMV at scale

- Highly addicted customer base with 80% purchases from repeat customers

It’s hard to overemphasize how well-positioned WEW is to capture the massive shift in home & decor consumer shopping … but I’ll try. The company has superfan customers. 85% of their customers visit the WEW site more than 100 times a year.

Each time a customer visits and buys a product, their individually curated online shopping experience improves. Each improvement incentivizes the customer to return to the platform, where they buy more products.

Each time a customer visits and buys a product, their individually curated online shopping experience improves. Each improvement incentivizes the customer to return to the platform, where they buy more products.

The true gem in this business is the ability to cross-sell own-brand products at 8-10% higher incremental contribution margins. Investors can drool over Active Customer Growth, but doing so misses the point. Over time, WEW will sell more own-brand products, which will allow them to generate above-average profits.

Those higher profits enable the company to reinvest back into their technology advantage to deliver the most curated content to their users constantly.

This year’s numbers don’t matter, and you can’t read into the COVID-19 pull-forward in customer growth and profits. What matters is what the business looks like in five to ten years. And right now, the company has all the ingredients to become a significantly larger and more profitable business.