We hope you enjoyed your extended weekend with friends and family. You might be thinking, “does Value Hive take a day off?” The answer is no! In fact, we’re writing this intro on Monday morning.

We don’t snooze so you can stay up-to-date on all things value investing.

This week we’re diving into two of my favorite fund manager letters. But before we do that, check out our two most-recent podcasts:

Also, if you have the time, please subscribe and leave a rating/review of the podcast on Apple Podcasts. It goes a long way in spreading the word about the show.

This week’s letters:

-

- Laughing Water Capital

- Greenhaven Road Capital

- Hayden Capital

We’ve also got a video from Charlie Munger’s Daily Journal meeting.

Let’s get after it!

—

February 19, 2020

Presidential Fun Facts: It’s President’s Day, so why not some fun trivia? You know the rules. No Googling. First person to email the correct answer will get $5 cash and bragging rights for an entire week. Are you ready? Here it is:

George Washington had a set of false teeth. They weren’t made from wood. What were they made from?

Good luck!

__________________________________________________________________________

Investor Spotlight: Off-The-Beaten-Path Letters

GIFs by tenor

GIFs by tenor

I’m excited to dive into these letters. Each manager has their unique spin on markets, investing and the concept of value investing. There’s a lot to learn from reading their thoughts.

Matt Sweeney kicks us off.

Laughing Water Capital: +20.9% in 2019

Matthew Sweeney’s Fund, Laughing Water Capital (‘LWC’), returned 20.9% in 2019. Since inception, the Fund’s returned 93.6% net of fees. This equates to an 18.4% compound rate of return. That’s darn impressive.

As Matt notes, the Fund’s underperformance shouldn’t be shocking. He says, “In a year when greater than 90% of SP500 returns came from multiple expansion, our relative underperformance should not be a surprise.”

Laughing Water sticks to simple, timeless investing principles. According to the letter, the Fund buys shares of good businesses that are, “led by incentivized management teams while they are dealing with some sort of optical, operational, or structural problem that we deem to be temporary.”

Let’s review three of LWC’s holdings:

-

- Aimia, Inc. (AIM)

- Avid Bioservices (CDMO)

- Hill International (HIL)

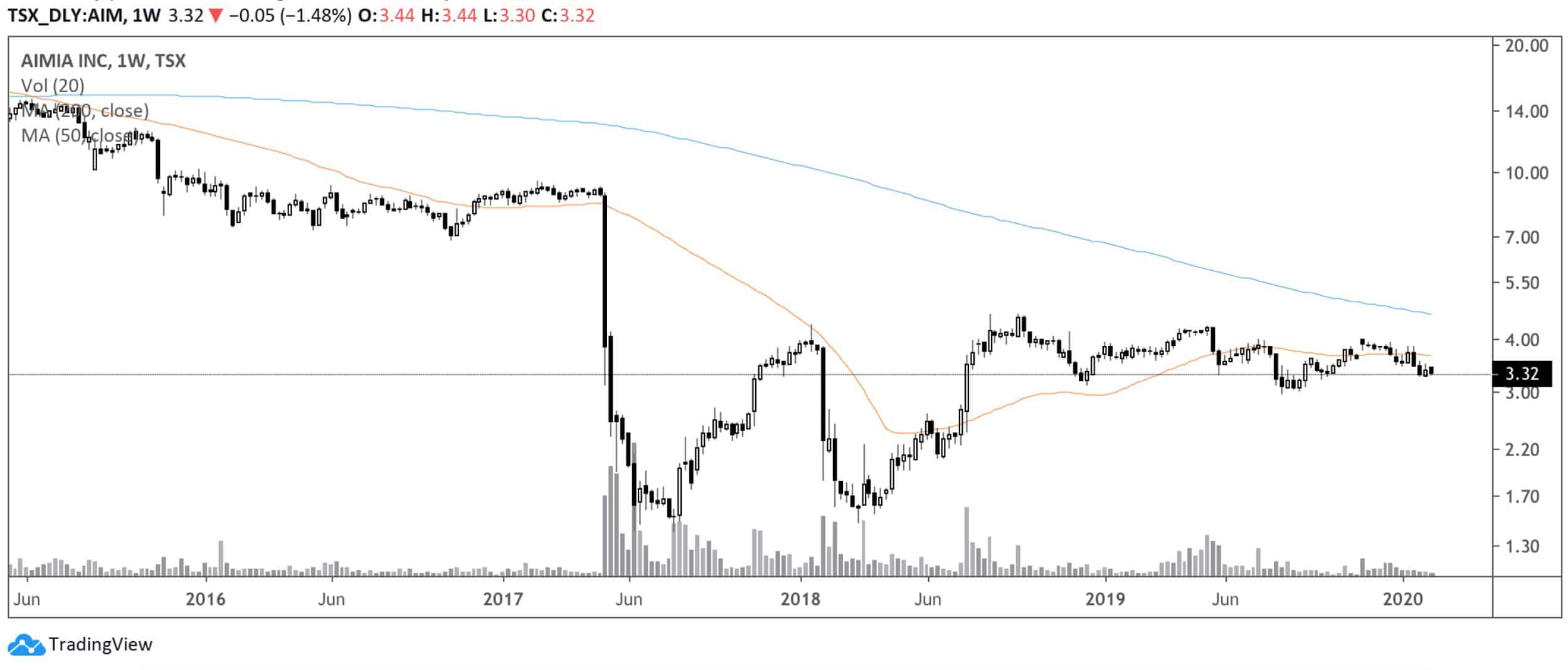

Aimia, Inc. (AIM.TO/GAPFF)

Aimia Inc., operates as a data-driven marketing and loyalty analytics company worldwide. It operates in two segments, Coalitions, and Insights & Loyalty Solutions. – TIKR.com

Here’s LWC’s reasoning for their initial investment:

“Our investment was based on the value of these assets, as well as the belief that an underperforming and improperly incentivized board of directors would be replaced in the near future.”

New management will take the helm in March. So what’s to like about the current price?

For one, you’re getting the loyalty business for next to nothing. The company has a $235M market cap with $203M in cash and no debt. Granted, the company’s lost money each of the last three years. But remember, you’re not paying much for that operating business.

Here’s the chart …

Avid Bioservices (CDMO)

Avid Bioservices, Inc., a contract development and manufacturing organization, provides process development and Current Good Manufacturing Practices (CGMP) commercial manufacturing services focused on biopharmaceutical products derived from mammalian cell culture for biotechnology and pharmaceutical companies. – TIKR.com

LWC lists reasons why CDMO is a great business (from letter):

-

- Recession proof business

- Powerful industry tailwinds

- Growing client list

- Significant competitive advantage

What more could you want?

Here’s what LWC sees over the long-term with CDMO (emphasis mine):

“Quarter to quarter and even year to year shares are likely to remain volatile as the business matures, but zooming out it is not difficult to imagine situations where a few years from now the company’s cash flow matches today’s revenue level. That might be 3 years from now or it might be 7 years from now, but given Avid’s existing pipeline, extremely high switching costs, and impossible to duplicate regulatory track record, this outcome appears likely.”

Let’s take a look at the chart …

Hill International (HIL)

Hill International, Inc. provides project and construction management, and other consulting services primarily for the buildings, transportation, environmental, energy, and industrial markets. – TIKR.com

There’s a few reasons LWC remains optimistic about HIL:

-

- Recent improvements in backlog

- Potential listing on Russell 2000 index

- Improved balance sheet and operating structure

It feels like a special situation given the Russell 2000 catalyst. Here’s LWC’s take:

“Given that being added to the index means forced buying without regard to price, and given that operationally the business is performing very well means there are unlikely to be many sellers, shares could re-rate considerably higher in the not too distant future.”

Think of it like the opposite of traditional spin-off/SPAC dynamics.

Here’s the chart …

Honorable Mentions

The letter details four other investments. But to spare the length, we won’t dive into those here. Check out the letter for more details:

-

- Iteris (ITI)

- Recro Pharma (REPH)

- Par Technologies (PAR)

- Clear Media (100:HK)

———————————-

Greenhaven Road Capital: +15.5% in 2019

Scott Miller’s fund, Greenhaven Road Capital, returned ~2% in Q4 and 15.5% for the year.

Miller spent the first part of his letter discussing what the fund doesn’t own. There’s a few commonalities, such as:

-

- Not owning a stock in the S&P 500

- Not owning a stock that’s bid up due to bond-like dividends

As Miller notes, “Ultimately, fundamentals do matter and trees do not grow to the sky.”

Here’s what Miller does own in the partnership (top 5 holdings):

-

- KKR & Co. (KKR)

- Par Technology (PAR)

- SharpSpring (SHSP)

- Digital Turbine (APPS)

- Kaleyra, Inc. (KLR)

We’ll pull Miller’s thesis for each stock along with the price charts.

KKR & Co. (KKR)

Greenhaven’s Take: “Rather, we own shares of the entity that benefits from management fees and incentive fees for all of the KKR funds in the market. While the absolute returns of the underlying funds may suffer as assets grow, management fees are guaranteed, and KKR manages 30+ strategies. Some portion of the various strategies will almost definitely generate incentive fees as well. We can argue about how many of the funds and how much per fund, but even if lower returns do happen, owning the corporate entity/general partner still makes sense.”

Here’s the chart …

Par Technology (PAR)

Greenhaven’s Take: “PAR is a business in transition, actively investing in and growing its “good” business, a restaurant point of sale (POS) system. The POS system serves as the spine of a restaurant, and PAR is actively adding functionality and revenue streams from areas such as payments, inventory management, data analytics, and mobile order management (integrating with UberEats, etc.). PAR should aggressively grow the number of locations using the software and the revenue per location over the next three years. “

Here’s the chart …

SharpSpring (SHSP) *Board Member — Little Details*

SharpSpring, Inc. operates as a cloud-based marketing technology company worldwide. The company offers SharpSpring, a marketing automation solution for small and mid-size businesses. It markets and sells its products and services through sales teams and third party resellers. – TIKR.com

Here’s the chart …

Digital Turbine (APPS)

Greenhaven’s Take: “Digital Turbine serves as a neutral third party that works with wireless carriers to preinstall apps on new cell phones, then sells the slots to app-driven companies like Uber, Amazon, and Netflix. The company saw 30% revenue growth in the core U.S. market where they work with four major carriers including Verizon and AT&T. Their growth is even faster in international markets. This past quarter, APPS announced a Telefonica partnership that will launch in the next six months.”

Greenhaven’ Largest Concern: Large companies going directly to phone carriers, circumventing APPS.

Here’s the chart …

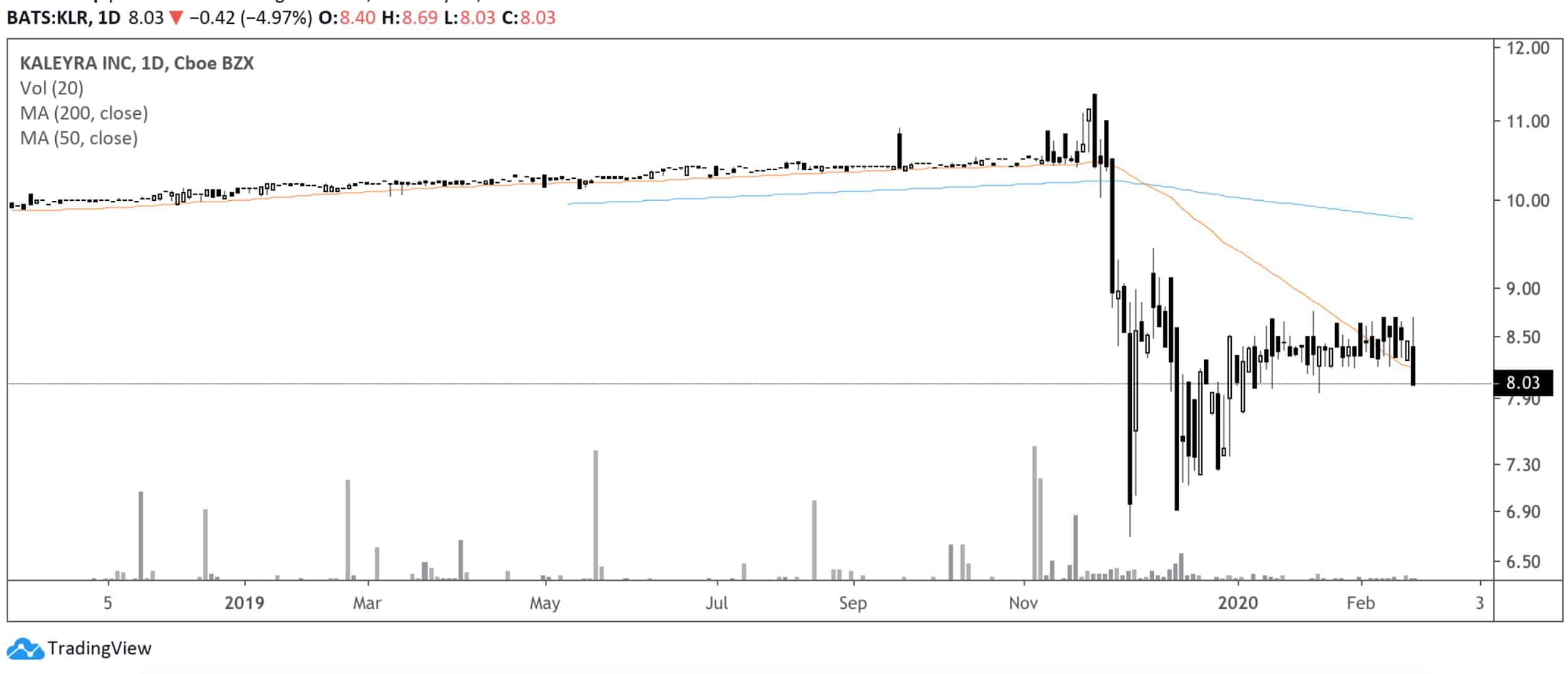

Kaleyra, Inc (LKR)

Greenhaven’s Take: “The real question for our investment at this point is: Can shares appreciate above $11.70? The current share price is $8.40, which implies a valuation of 1.5X revenue. This is a significant discount to its peers (Twillio is at 9X revenues and Sinch, a more relevant comparable, is just under 3X). The investment bank Cowen has an $18 price target on KLR shares and Northland has a target of $17. We are effectively getting paid to look at the next three earnings releases while not assuming the risk of a price decline. Kaleyra is profitable, and grew revenues in excess of 40% last quarter. A share price in the teens does not appear wildly implausible with a modicum of positive news.”

Here’s the chart …

Honorable Mentions

Miller disclosed two new investments:

-

- Balwin Properties (BWN.JO)

- Elastic Software (ESTC)

Check out his letter for his deep dive into those names.

———————————-

Hayden Capital: +41.06% in 2019

Fred Liu returned a whopping 16.8% in Q4 and 41.06% in 2019. Those are fine numbers!

Where did Fred’s returns come from? According to the letter: Asia. Liu explains:

“As of today, ~55% of our investments are headquartered in Asia, ~38% in the US, and the rest split between Europe and Cash. Even with that, most of our American companies derive a significant portion of their earnings from abroad, while our Asian and European companies are predominantly domestic.”

Liu didn’t spend much time discussing his seven holdings. He mentioned two names:

-

- Sea Limited (SE)

- Carvana (CVNA)

Yet what the letter lacked in idea specifics, it made up with knowledge bombs.

Here’s a list of my favorite quotes from the letter:

-

- “Sometimes I describe businesses like these, who are in an earlier-stage of their business lifecycle, like “children”. Even from a young age, you can usually tell when an exceptional child has qualities that set them apart from their peers (KPIs, usage metrics, etc.).”

- “For example, you can see below that out of the 29 investments we’ve made since Hayden’s inception, the top 20% of positions (6 investments) accounted for over 100% of our gains (108% to be exact)5 . We’re wrong often, and that’s okay.”

- “Studying investors such as Charlie Munger, Hillhouse, Himalaya, Nomad Investment Partnership, Prescott General, among others sparked the realization that it’s a handful of investments that really drive the long-term outperformance of these funds.”

The letter is well worth the read. Also, if anyone knows Fred, I’d love to get him on the podcast.

__________________________________________________________________________

Resource of The Week: Long Live Charlie Munger

GIFs by tenor

GIFs by tenor

Pull up a chair, grab some popcorn, it’s Munger time!

CNBC aired a two-hour long live-stream of Munger’s Daily Journal meeting. You can watch the replay here.

It’s a great way to spend an afternoon or evening.

__________________________________________________________________________

Tweet of The Week: That Bat Flip Though …

Warren Buffett tells us to invest in our sweet spot. This is what it feels like when you wait for that perfect pitch:

Girls, bruh. That swing. The bat-flip… pic.twitter.com/lAY0NXcGv2

— Rex Chapman🏇🏼 (@RexChapman) February 15, 2020

That’s all I got for this week. Shoot me an email if you come across something interesting this week at brandon@macro-ops.com. Have a great Christmas holiday.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!