Does the recent rally in gold give bulls the “All Clear” that it’s finally safe to come out?

HELL NOOOO… IT’S A TRAP!

With a brutal four year decline and the loss of more than a third of gold’s value, the gold bulls have taken quite a beating. But ever the believers in bullions’ long-term efficacy as a “store of value” in a world dominated by central banks, the gold bulls have remained hopeful… the true believers are, if anything, devoted.

They’ve taken this rally as a sign that vindication is finally at hand, as they clamor to scoop up shares of miners and gold ETFs.

Even big name investor, Stanley Druckenmiller, has begun pounding the table for gold, saying he’s been “backing up the truck” to purchase shares of miners for his personal fund.

Though the Foundation team sympathizes with those that view gold as a safe haven and don’t like what central banks around the world are doing to savers, now is not the time to be buying the stuff. It’s still too early and the yellow metal has further to fall.

Here’s the deal. Gold has no utility. It doesn’t pay a dividend and isn’t vital in any way to the economic system. Factories can’t run off it, people can’t eat it, and it’s not used to build anything of use. It is just a shiny rock that is occasionally used to make jewelry. Buffett put it well when he said:

Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.

The only time you want to be long gold is when you think more people will want to buy it from you at a higher price in the future. Gold is and always should be a trade, and never an investment. It’s a “fear hedge”. The only thing that drives demand for gold is fear. This is important and it’s something gold bugs have been getting wrong. It’s the fear of inflation that drives gold… nothing else.

Gold, like all commodities, is priced in US dollars. Because of this, it’s sensitive to the strength of the dollar.

It tends to rally when the fear of inflation creeps up and threatens to eat away the value of the world’s reserve currency. People move their money into hard assets like gold with the expectation that its value will increase by at least the rate of inflation.

A particularly interesting example of this was gold’s most recent bull market. It began rallying in 01’ during the unwind of the tech bubble, which coincided with a major reversal in the dollar. The dollar depreciated as the Fed slashed rates, and this in turn jump started gold’s impressive rise. The gold bull market then picked up steam in 09’ after the great financial crisis when QE and TARP were introduced and inflation expectations soared. People were predicting the death of the dollar. And so the dollar sold off and gold rallied as a result.

But inflation never came. Not only were the cries about runaway inflation off, but they were completely wrong. Deflation, not inflation, became the primary concern… and a stronger dollar the result. This caused the gold bull market to end and left us with the long-term downtrend that we’re now experiencing.

The growing deflationary pressures on much of the world and the stronger dollar are big (and often poorly understood) drivers behind the recent collapse in commodities. This is why gold will not start a bull market anytime soon. Because now, more than ever, deflation is becoming a reality. And the macro drivers behind a stronger dollar couldn’t be more obvious.

The world is awash in debt (which is deflationary), emerging markets are enveloped in a budding currency war (which is USD bullish), and the world is collectively short $11 trillion in a carry-trade that has yet to unwind (which is extremely USD bullish).

So it’s not a bull market in gold that traders should be looking for, but the start of a more violent downtrend before the yellow metal eventually finds a bottom… which is a ways off.

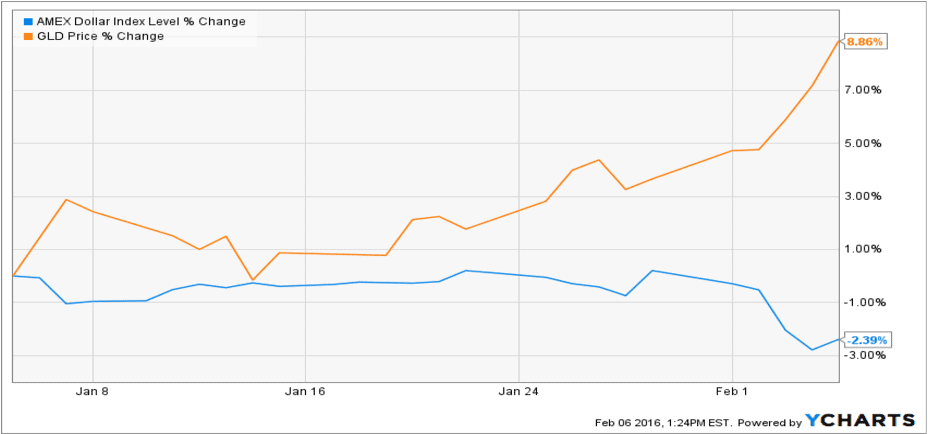

So what to make of the recent rally in gold, then? Two words… noise and re-positioning. The majority of this retracement was due to meaningless repositioning in the dollar (shown in the chart below). Long dollar had become a crowded trade. The trend became overextended in the short term and the current retracement came about as a healthy shakeout of weak hands.

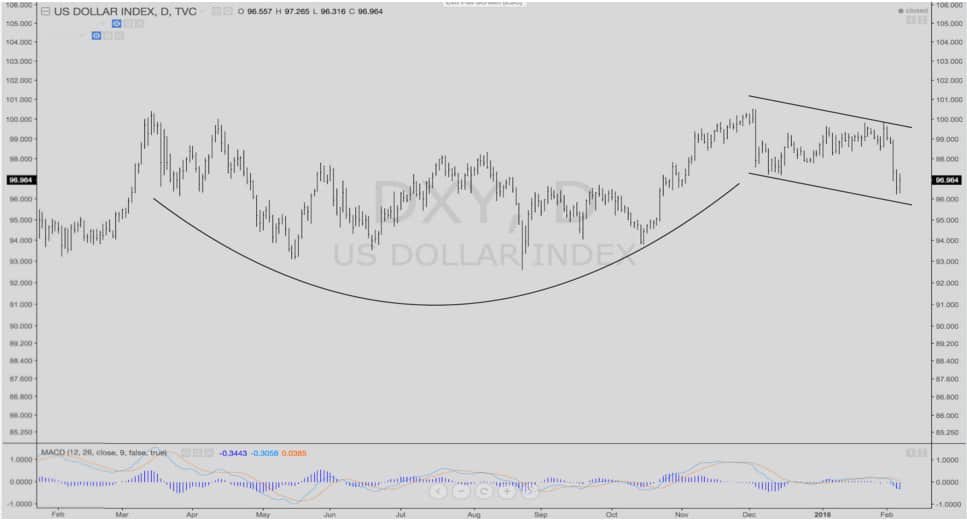

We wouldn’t be surprised to see even more short-term dollar weakness before it begins the final leg of its epic bull run. And as others have pointed out, the dollar could be nearing the completion of a large, 12-month, cup-and-handle pattern. This type of pattern is very bullish for USD.

Lastly, when viewed within the broader context of the downtrend in gold, the recent rally is meaningless. It’s just a normal bear market retracement (aka noise). The chart below shows how this type of vertical retracement has happened four other times over the last two years of the downtrend. And every time shortly thereafter, gold fell to a new low. This time will be no different.

There are few things more destructive to a trader’s financial well-being than bull traps. The traps work for a reason; they are real damn enticing! The most bullish looking short-term price action happens in a bear market, not a bull. But these are hope jags and nothing else.

There will be a time to “back up the truck” on gold and other commodities. But that won’t be until the Fed is forced to unleash extremely unorthodox inflationary policies to fight off the coming deflationary tidal wave. And then, and only then, will the gold bugs — or what’s left of them — finally get their day in the sun.

Until then, remember that bottoms are a process, and not an event. When gold finally does bottom… the price action won’t look nearly as nice as it does now.