Village Farms International (VFF.TSX) operates five high-tech greenhouses across Canada and the United States. The company has ~500 acres of growing area and sells 80%+ of its products to North America’s foremost “big box” grocers and retailers.

Today, VFF leverages its greenhouse produce scale to grow the highest-quality, lowest-cost cannabis through its 100% owned subsidiary, Pure Sunfarms. The cannabis subsidiary does 40% gross margins while booking 8 consecutive quarters of positive net income. In addition, VFF is the best-positioned greenhouse operator to benefit from the US’s changing regulatory cannabis stance. The company has 130 acres of greenhouse growing space in the Permian Basin that can easily convert to cannabis production.

The company’s founder, Michael DeGiglio, continues to run operations as CEO and personally owns 12% of the business. Interests are aligned.

And if that wasn’t enough, the company recently announced its option to buy back ~5% of the current shares outstanding. In other words, the management team also sees the intrinsic value gap.

Our Variant Perception: The company is shifting its business from low-margin grocery produce to higher-margin cannabis products. Unfortunately, investors that examine the financials only see a low-margin grocery business. Moreover, VFF is transitioning its cannabis business to mainly retail sales compared to historically more significant wholesale orders. Retail sales offer higher margins and potential for brand affinity with customers.

If VFF executes well, the coming years will look nothing like the past. After falling 25% on a positive earnings report, investors can buy this business for <2x 2022 sales and 14x 2022 EBITDA.

The TL;DR version of our Bull Pitch comprises three simple ideas:

- VFF is one of the largest and longest operating vertically integrated greenhouse operators in North America

- VFF owns a majority stake in Pure Sunfarms, which is Canada’s most successful cannabis company, with margins north of 40%

- VFF has a massive facility in texas ready to grow cannabis once laws change, which means a ton of upside optionality once the inevitable happens

Are you ready to learn more? Let’s go!

Profitable Produce Business Allows VFF To Wait For US Regulation Changes

VFF is a unique greenhouse operator. Unlike most of its competitors, the company didn’t rush to convert 100% of its greenhouse assets to cannabis. In contrast, VFF’s competitors ran to the market, building cannabis-specific greenhouses or converting existing assets to make cannabis before demand materialized.

Those that built cannabis-specific greenhouses burnt cash while waiting for demand to hit. Some had to close down the entire operation.

What separates VFF from everyone else is its grocery produce business. The company has a durable, profitable grocery business to “kill time” as it waits for cannabis demand and regulations to change. Moreover, it didn’t have to build its cannabis infrastructure, which would’ve cost millions of dollars. VFF has all the greenhouse infrastructure it needs to profitably compete on a global scale.

VFF’s Immense Greenhouse Production Assets

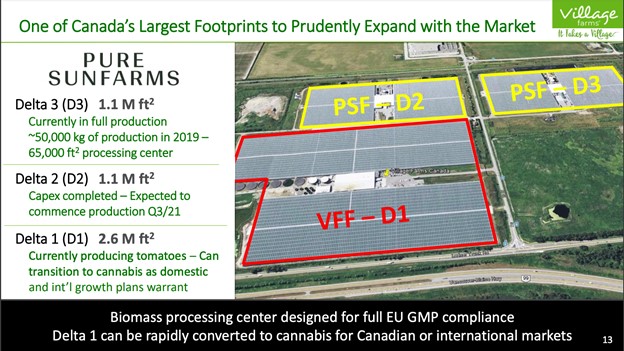

A great example of the company’s massive greenhouse scale is its Delta 1, 2, and 3 production facilities (see below):

Delta 3 (D3) is the only greenhouse in full cannabis production mode. Delta 2 (D2) should start production during Q3 2021. Combined, VFF has ~2.2M sqft of cannabis production space in Canada. The company can transition its Delta 1 (D1) facility to produce cannabis if they want to. That’s an extra 2.6M sqft of production without any additional capex spending.

That’s what they have in Canada.

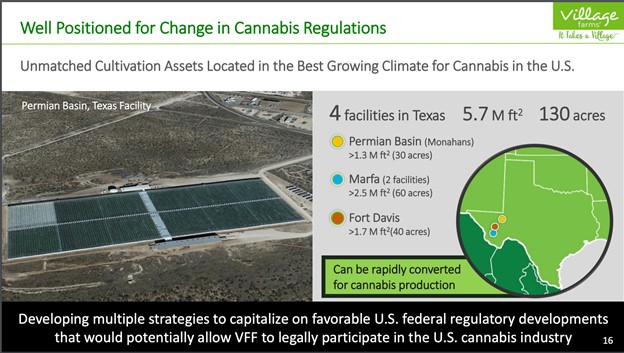

The company has an additional 5.7M sqft of greenhouse production space via four facilities in Texas’ Permian Basin (see below):

I can’t think of a better-positioned company to capture the shifting US regulatory environment around cannabis. As soon as the US regulations change, VFF can open its 5.7M sqft production facilities to meet newfound demand. All without spending a dime on building new greenhouses.

Messy Current Financials Muddy Long-term Cash-Generating Ability

The company’s current financials are messy and riddled with one-item expenses that reduce its reported gross/EBITDA margin. There are two reasons for this. First, the company’s produce business is a historically low-margin business, and tomatoes (VFF’s “cash crop”) are in the middle of a ten-year price glut.

Second, VFF booked higher COGS in its Pure Sunfarms (cannabis) business. This is because they transitioned to selling mainly Cannabis 2.0 retail products compared to its wholesale segment. The switch to branded retail required an initial investment in manufacturing, packaging, and distribution.

Over time as the company transitions to mostly a cannabis business, it should capture higher gross and EBITDA margins. For example, during Q1 2021, VFF’s cannabis business generated a 40% gross margin and 13.6% EBITDA margin.

Playing The Brand Game In A Commodity Market

VFF has a clear strategy with its Pure Sunfarms business: create a strong brand affinity in an otherwise commodity market to maintain industry-leading margins.

The company is the lowest-cost producer in space. So imagine the margin durability if they can attach a solid brand to that cost advantage. VFF’s founder, Michael DeGiglio, commented on the power of brands in his Q1 earnings call (emphasis mine):

“I want to take the opportunity here to touch on the consistent brand performance of Pure Sunfarms to date as well. There is a perception that due to the inability to market and advertise, it is impossible to build a brand in Canada. But we clearly disagree, and we think our track record of market share performance proves us out. As you know, our brand is more than a name or logo, it’s how the customer perceives that name or logo, what the customer associates with the name or logo. It’s what drives repeat purchases of existing products and entices purchases of new products based on previous experience with that brand.

And we believe our track record of leading market share performance over the long-term is a reflection of a real brand. The Pure Sunfarms brand, the brand that equates to a premium quality product at an everyday price.

Still, we are not resting on our laurels. The market is evolving. Customer preferences are evolving, and the Pure Sunfarms team remains laser-focused on continuing to elevate its already premium level quality, develop new processes to enhance our products and new products that will continue to resonate with our customers.”

It’s too early to raise any brand trophies, but we’re seeing positive signs from Ontario. Since its launch in Q4 2019, Pure Sunfarms maintains the #1 brand in Dried Flower products.

Valuation: Buy Produce/Canadian Cannabis, Get Rest For Free

VFF has one of the most attractive valuation scenarios we’ve seen in the cannabis space. The company trades at ~2.7x NTM Sales. At first, this doesn’t scream cheap. But look what you get for free at the current price:

- US cannabis segment growth

- Canadian cannabis growth

- 16.6% Stake in DutchCanGrow Joint Venture

- 6.6% Stake in Altum International

You’re not paying for VFF to legally participate in the US cannabis industry nor open its Delta 1 production facility in Canada to meet demand.

VFF owns 16.6% of DutchCanGrow, a Netherlands-based cannabis business. The venture is currently on a waitlist to receive a production license. We’re paying $0 for this venture.

The company also owns a 6.6% stake in Altum International, one of Asia-Pacific’s leading cannabinoid platforms. Altum generates sales through three main channels: consumer brands, commercial inputs, and retail sales.

Altum launched various CBD products, supplies craft breweries and coffee bars with CBD-infused beverages/edibles, and opened Asia’s first dedicated CBD consumer outlet store.

Again, we’re getting Altum for free at the current price.

VFF also boasts one of the most robust balance sheets in its industry. The company has roughly as much cash in the bank (CAD 131M) as total liabilities (CAD 35M).

Risks & Concluding Thoughts

There are a few ways we can lose money on this investment. First, the company could continue to dilute shareholders as they have in the past (nearly doubled share count since 2015). Granted, VFF issued most of those shares to acquire Pure Sunfarm, which proved an intelligent capital allocation decision.

Second, VFF’s Pure Sunfarm brand could lose market share/favor with customers.

Finally, the company’s produce business hits a downturn, and they need to raise debt to finance its cannabis production business.

VFF is the best-positioned cannabis producer in the industry and is poised to capture demand growth from changing US regulations. In addition, the company’s existing greenhouse infrastructure assets allow it to easily transition to producing cannabis without spending millions in capex.

At scale, VFF’s cannabis business can generate 40% gross margins and double-digit EBITDA margins while offering the lowest-cost product.