Today we’re diving into one of the most exciting Brazilian businesses we’ve ever seen at Macro Ops.

“In this huge country, no one can get so close, so quick and with so many solutions, to the customer and seller as we can.” – Roberto Fulcherberger

What is Via Varejo

On the surface, Via Varejo (VVAR, or Via) is Brazil’s largest electronics and furniture retail company. The company has 1,000+ physical stores through its two retail brands (Casas Bahia and Ponto Frio) to serve its 97M customer base (22M active customers).

Yet look deeper, and you find a company transforming from a first-party retailer to a third-party retailing platform. Despite this evolution and growth rates twice the market average, Mr. Market still values the company like a struggling, low-growth appliance retailer. This provides us with over 200% upside from our base case valuation.

Brazil’s e-commerce market made up 4.3% of all retail spending last year. No one else can offer e-commerce customers and partners what Via offers. Here’s why that matters: All future e-commerce penetration growth must flow through Via. That’s valuable.

Via Varejo’s Remarkable Turnaround: From Decline to Digital Dominance

Via is a turnaround story turned growth monster. In 2019, Via generated -4.7% revenue growth, compressed gross margins by 200bps, and made 86% less operating income than 2018.

We can attribute such poor performance to Via’s leadership and direction as a smaller subsidiary inside GPA (Brazil’s most prominent retail conglomerate).

The original founders saw Via’s decline, and in 2019 bought back their majority stake to gain control of the company. Soon after, the family named Roberto Fulcherberger CEO.

Fulcherberger turned the company around, and by 2020, Via was in the black, generating 12% revenue growth and 7% EBIT margins.

How did he do it? First, Fulcherberger transformed Via into a digital-first retailing platform and leveraged its existing physical infrastructure. The result: Brazil’s largest logistics network, a rapidly growing online 3P marketplace, and a leading financial solutions platform.

Via’s 1P and 3P marketplaces each grew by 120%+ with online sales comprising 56% of total sales. In addition, the company’s logistics network includes 27 distribution centers and covers over 1.1M square meters to provide same-day (and soon, same-hour) delivery service.

Via should generate R$ 3.2B in operating income at 8% margins by 2022. Its closest competitor, Magazine Luiza (MGLU3), should generate R$ 2.8B at 6.5% margins. Yet MGLU3 trades at 3.34x NTM sales and a whopping 57x NTM EBITDA. Via, on the other hand, trades at 0.99x NTM sales and 13x NTM EBITDA.

By 2025, we estimate that Via will generate R$ 57B in revenue and R$ 5.7B in EBITDA (10% margin). These estimates assume a ~15% revenue CAGR and 200bps of EBITDA margin expansion due to a more significant percentage of sales from online, 3P channels.

What should a reasonable buyer pay for this business? 15-25x EBITDA seems appropriate. At 15x EBITDA, we get ~R$ 85.5B in Enterprise Value. Subtract the R$ 13B in net debt on the balance sheet, and you get ~R$ 72.4B in shareholder value or R$ 45/share (200% upside).

Via’s Profit-Generating Powerhouse: The 1P Business Model

Via’s core/legacy business is its 1P commerce platform offering electronics, home appliances, and furniture. The company sells its product through four retail brands, Casas Bahia, Ponto Frio, Bartira, and Extra.br. As of Q1 2021, Via had 847 Casas Bahia and 168 Ponto Frio storefronts. The company plans to open an additional 120 stores this year with one new Casa Bahia megastore.

![]() Via’s 1P business is a steady cash cow. Its retail brands carry strong top-of-mind recognition and, in most cases, represent 60%+ market share in any given category.

Via’s 1P business is a steady cash cow. Its retail brands carry strong top-of-mind recognition and, in most cases, represent 60%+ market share in any given category.

For example, Bartira is the largest furniture factory in Brazil and Latin America. The segment makes 750 products per hour and generates 35% of Via’s total furniture sales.

Then there’s Extra.br, Brazil’s first e-commerce website. It offers a platform for sellers, which sells anything from Automotive products to diapers.

By providing the most extensive assortment of products, Via drives loads of organic demand to its site. As a result, Via is Brazil’s largest seller of Playstation 5, Samsung phones, and iPhones. As of 1Q 2021, 1P commerce drives 90% of total GMV.

The company’s dominant 1P business allows it to invest in its 3P platform, its primary focus in 2021 and beyond. At 10% of total GMV, Via’s 3P Marketplace has a long runway for rapid expansion.

Here’s CEO Roberto Fulcherberguer’s explanation of the company’s shift:

“So this is the year of the marketplace at Via. 2021 is certainly the year of marketplace at Via. Our omnichannel approach is a very strong point, and it will be at the service of the marketplace.”

It’s important to note that Via’s 1P business only gets better the more products it offers. This makes intuitive sense. The company’s core products (furniture, home appliances, cell phones, etc.) aren’t highly recurring purchases. Adding more products increases customer frequency, which in turn increases LTV and higher unit economics.

Via’s 3P Platform: Leveraging Existing 1P Commerce Channels

Via has an elegantly simple 3P marketplace model with two levers: Distribution Channels and Logistics Network.

The company opens its distribution channels (I.e., its primary brands). In addition, it allows third-party sellers to list products on its site. Sellers love using Via’s distribution channels because they know they’ll reach the widest audience possible (97M customers).

The company opens its distribution channels (I.e., its primary brands). In addition, it allows third-party sellers to list products on its site. Sellers love using Via’s distribution channels because they know they’ll reach the widest audience possible (97M customers).

Moreover, Via offers the best logistics network for 3P sellers. The company has 27 Distribution Centers (DCs), 1,000+ physical stores to act as local, last-mile hubs, and 300K last-mile delivery partners.

As a seller, Via’s logistics network is a no-brainer. The company covers 100% of cities and offers same-day (and same-hour) delivery. This strong value proposition to sellers shows in the data.

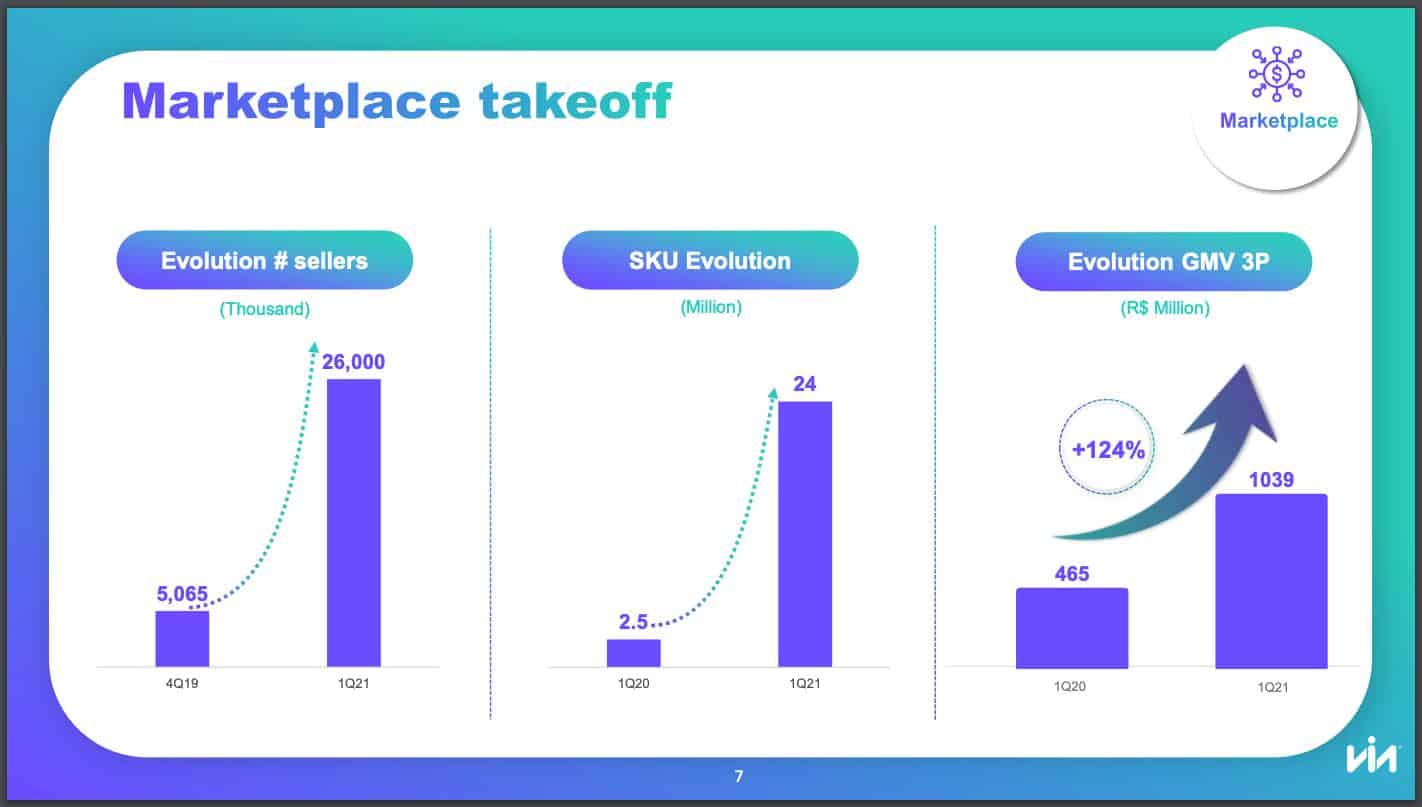

The company 5x’d the number of sellers on its platform, from 5,000 to 26,000 since 1Q 2021. During that same time, Via 12x’d its SKU count from 2.5M to 24M. All this translated to a 124% increase in 3P GMV to R$ 1.03B.

One interesting wrinkle in Via’s logistics network is its potential outsourced subscription model. Beginning in 2H 2021, the company will offer a Consumer-to-Consumer (C2C) delivery platform.

The platform will allow consumers to hire Via’s logistics services for light or heavy products, donate, transport, or dispose of any product. The company will also offer an ultra-quick delivery service this year similar to a “fast-food” approach.

BanQI: Unveiling Via’s Comprehensive Financial Solutions Suite

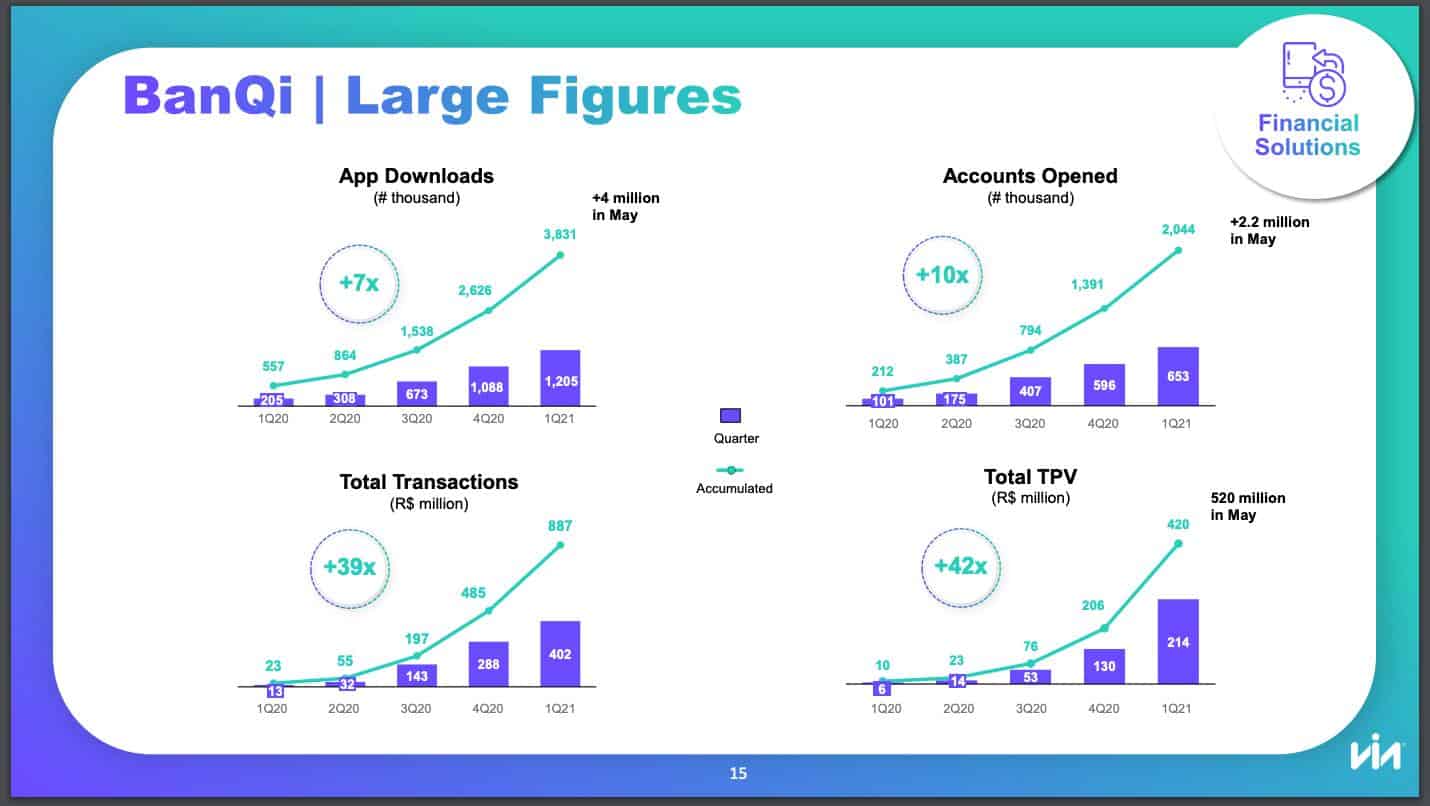

banQI is Via’s financial solutions platform offering installment plans/booklets, credit cards, and other direct consumer credit. The company views banQI as a low-cost customer acquisition platform. For example, it costs ~R$ 15 to open a digital account.

banQI is Via’s financial solutions platform offering installment plans/booklets, credit cards, and other direct consumer credit. The company views banQI as a low-cost customer acquisition platform. For example, it costs ~R$ 15 to open a digital account.

Over the last three months, the company’s opened 800K+ banQI accounts to reach a whopping 2.2M digital accounts opened since launch. Growing banQI digital accounts is highly accretive as banQI customers buy ~2x more products per year than non-banQI customers.

The company plans to offer personalized loans and other consumer-specific financial products to the ~43% of Brazilians without a bank account or the 67% without access to a credit card.

Big Picture: World of Commerce Flows Through VVAR3

Gavin Baker said it best when he wrote, “The future was always going to be omnichannel. Pundits have been prematurely predicting this for many years, but it is finally happening.”

Via knows this better than any other Brazilian player. Its 1,000+ retail stores complement its massive 27 distribution centers to create an unmatched hub-and-spoke delivery system. Via’s omnichannel benefits also bleed to its 3P sellers too.

Soon, the company will allow 3P sellers to sell merchandise in existing Via retail stores. Between its 1P/3P marketplaces, its logistics network, and financial solutions offering, Via has created a one-stop shop for consumers and sellers.

Soon, the company will allow 3P sellers to sell merchandise in existing Via retail stores. Between its 1P/3P marketplaces, its logistics network, and financial solutions offering, Via has created a one-stop shop for consumers and sellers.

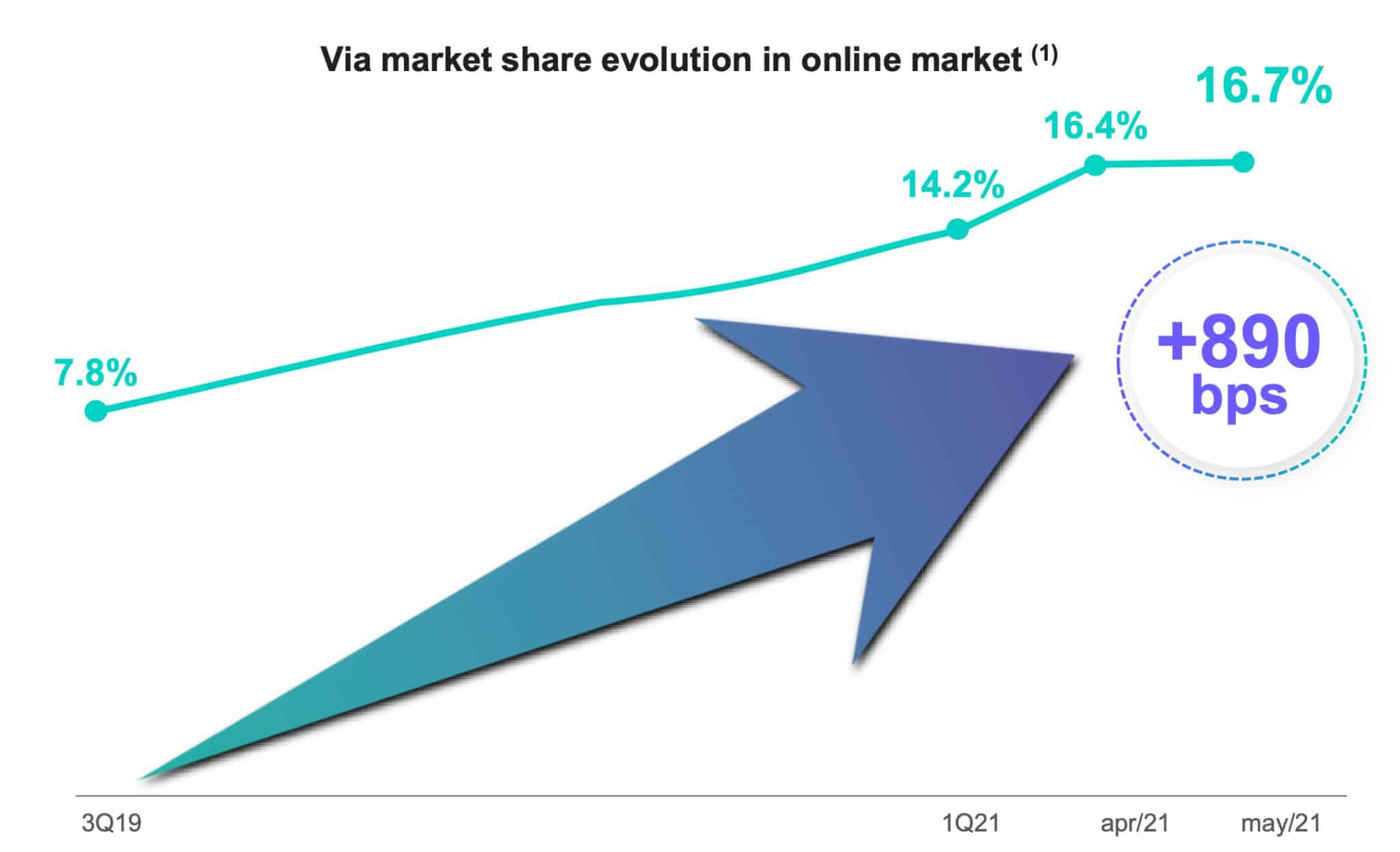

Yes, the competition is fierce and includes names like Mercado Libre (MELI), Amazon (AMZN), and Magazine Luiza (MGLU3). But here are the facts… Since 3Q 2019, Via has more than doubled its online sales market share (from 8% to 17%), grown twice as fast as its e-commerce industry peers (119% vs. 72% 1Q 2021), and expanded gross margins 200bps.

If anything, Via seems to benefit from increased competition.

As the nation’s leading marketplace platform, all future e-commerce growth must flow through Via. In addition, no other retailer has a comparable logistics network or existing customer base that Via offers.

As such, we see a world where Via generates R$ 57B in revenue and $5.7B in EBITDA by 2025 while making conservative assumptions about revenue growth (15% CAGR) and EBITDA margin expansion (200bps). Assuming a modest 15x EBITDA multiple, Via would command an R$ 85.5B Enterprise Value and R$ 45/share in shareholder value.

Over the next five years, online sales will represent 2/3rds of the company’s GMV. In return, Via will complete its transformation from a first-party appliance retailer to Brazil’s most dominant online marketplace platform.

In five years, investors will look back and wonder how a business like Via could trade for less than 1x EV/Sales.