Last week we remembered 9/11. We thank those brave men and women who ran into the fray that day — and every day. If you haven’t already, thank a veteran this week.

We’ve got a hard-hitting Value Hive this week. Value stocks are back, a fitness equipment company thinks its a tech business, Elliott Management’s gone activist and more!

Make sure to subscribe to this newsletter so you receive it every week, completely free.

Let’s get to it!

—

September 18, 2019

The More You Know — On this day in 1973, soon-to-be President Jimmy Carter filed a report with the National Investigations Committee on Aerial Phenomena (NICAP) claiming he saw a UFO in 1969. If elected President, Carter vowed to declassify all UFO material to the United States public.

He didn’t follow through with that promise. So I guess we’ll never know exactly what Carter saw that evening.

__________________________________________________________________________

Investor Spotlight: Elliot Management & Spruce Point Management

GIFs by tenor

“We’re not mad, we’re just disappointed.”

That sentence sums up Elliott Management’s activist letter to AT&T (T). The letter outlines poor decisions made my T’s management, as well as a path towards 65% increase in share price.

Why does Elliot have beef with AT&T?

For starters, T’s underperformed the S&P 500 for the last ten consecutive years. Ouch.

Elliot also questions T’s acquisition strategy. The firm highlights three disastrous acquisitions (or attempted acquisitions):

- Failed T-Mobile Merger

- Overpaying for DirecTV

- No clear strategy for Time Warner acquisition

In Elliot’s view, the failed T-Mobile merger opened the door for the (at the time) struggling 4th place contender. AT&T then paid $67B to acquire DirecTV, an asset that’s seen premium subscriber count fall faster than shareholder confidence. Finally, after paying $109B for Time Warner in 2016, AT&T has yet to solidify the purpose of such a purchase.

Light At The End of The Tunnel

All hope is not lost. Elliot sees a path towards 65% share price appreciation over the next two years.

How do they think T will get there? Through Elliot’s handy-dandy four-step program that’s how (see below):

Shareholders should win handsomely if Elliot gets their way at unlocking value.

Spruce Point is Short Church & Dwight (CHD)

Founded by Ben Axler, Spruce Point Management isn’t a name you want to hear if you’re long a stock. In fact, if Axler puts out a short thesis on one of your long ideas, it’s time to check your thesis (and your pants) again.

Here’s a quick hit-list of accolades Axler’s accumulated:

-

- #2 most successful short-selling activist in 2018

- #1 short-seller by Sumzero after 12,000 analyst study

- #13 Most Influential Financial Twitter profile (per Sentieo)

I love studying short-dominant firms. They add a level of in-depth due diligence that is often overlooked with many long ideas. This makes sense though. If you’re wrong on a short idea, the position grows as a percentage of your portfolio.

Spruce’s latest short idea is Church & Dwight (CHD). The company is a serial acquirer of personal care and consumer products. There’s a 99.99% chance you’ve used some of the company’s products before:

-

- OxiClean (RIP Billy Mays)

- Trojan Condoms

- Orajel

- Arm & Hammer

- Etc, etc.

So what’s the dirt?

According to Spruce’s research report, the company’s engaged in “extreme financial engineering, aggressive accounting, and managerial self-enrichment practices.”

Spruce also believes that 6 out of 10 of CHD’s “power brands” are struggling financially. Some of them, the report claims, are complete failures.

Misleading Accounting Practices

Let’s talk about accounting methods for a second (I know, don’t everyone get excited at once!). Spruce notes that by using the equity method of accounting, the company inflates operating margins, working capital and FCF.

How do they do that? The equity method avoids adding in manufacturing aspects of CHD’s business. Adding these expenses in would reduce all the above metrics.

What’s The Downside?

Spruce sees 30-50% downside from current share prices (around $70/share).

__________________________________________________________________________

Movers and Shakers: Peloton’s Going Public

Can’t get enough of your money-losing IPOs? Well you’re in luck!

Peloton (PTON) dropped their S-1 last Tuesday, telling us all about how they’re not just a fitness equipment company.

In their own words, Peloton is “an innovation company transforming the lives of people around the world through [their] ever-evolving fitness platform.” Did you catch all those buzzwords? If you didn’t here they are:

-

- Innovation

- Transforming

- Ever-evolving

- Platform

I can hear the cries for an 11x sales multiple as I type.

Peloton wants to be the one-stop-shop for all things fitness and healthy living. So far their strategy is working. The company has 1.4M subscribers. That’s good for the largest interactive fitness platform in the world.

The company’s growing revenues faster than their head trainer can bike. Revenues grew from $218.6M in 2017 to $915M in 2019 (over 100% 3-year CAGR). On the back of $915M in revenue, Peloton lost $71.3M in EBITDA.

Before you go running to increase margin for your next short, there’s a clear bull thesis to Peloton.

How Your Fitness-Crazed Sister Would Describe Peloton (The Bull Case)

Peloton’s bull case:

-

- Peloton is a high-margin, recurring revenue generator with a fanatical customer base.

- They’ll be able to “turn-on” profitability by reducing their investment in growth.

- Peloton sports low churn ratios and highly-visible revenues.

- If the company can grow, they’ll be able to spread SG&A costs over a wider array of customers (increasing margins).

They’re Just a Bike Company (The Bear Case)

The bear case:

-

- Peloton sells expensive exercise bikes and is going public in the late innings of the market cycle.

- Their niche customer base will dry up once a recession hits. People won’t pay for $2k bikes and $40/month subscriptions during a downturn.

- This would increase churn ratio, which reduce margins.

- The company hasn’t shown signs of profitability yet, losing $100M in 2019.

No matter which side of the fence you’re on, it’ll be interesting to see where the company starts their trading career.

__________________________________________________________________________

Idea Backlog: Einhorn’s Latest Long — The Chemours Company (CC)

GIFs by tenor

Chemours Company (CC) first appeared on my radar after reading David Einhorn’s 2Q 2019 letter. Einhorn hit it big with his first swing at CC — going from sub-$5/share to $57/share back in 2015-17.

CC spun-out of DuPont in 2015. As part of the spin-off arrangement, CC had to pay indemnification liabilities back to DuPont (if you’ve followed GTX you know this pattern).

Einhorn’s bull case was simple. He believed CC owed less in liabilities than the $5B claims touted by bears. He was right. DuPont and CC settled for $335M, well below the $5B claim.

Deja-vu for Greenlight

The bull case is much the same for Einhorn today as it was in 2015.

CC shares declined sharply during 2Q in response to liabilities surrounding fire-fighting foams. Bears suggest this liability will cost the company billions of dollars. Einhorn doesn’t agree.

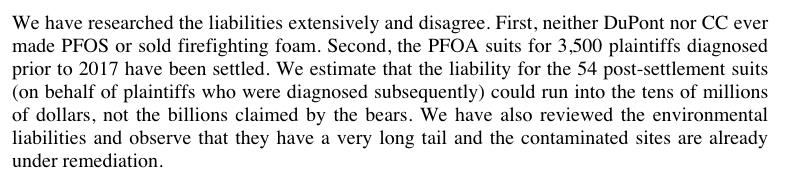

Here’s Einhorn’s take (from the letter):

If Einhorn is right, and the company only owes millions (not billions), what is CC worth?

CC is Very Cheap

The company trades less than 5x earnings. Given the current share price (around $16), you can buy the fluoroproducts business for less than 10x EBITDA and get the rest of the company for free.

Einhorn believes the fluoroproducts business is worth more than the entire company. The segments generates half of the company’s earnings, earnings which Einhorn thinks commands a higher multiple.

Greenlight sees a path towards $10/share in earnings power by 2021. If you subscribe to his bullish narrative, you can buy the company for less than 2x 2021 earnings.

__________________________________________________________________________

Resource(s) of The Week: Damodaran & Clifford Sosin

We’re spoiling you this week with two resources. The first is a video from Aswath Damodaran on WeWork’s valuation. The second is a whitepaper from investor Clifford Sosin at CAS Investment Partners.

Analyzing WeWork’s Value Destruction

The King of Valuation is back, this time with an analysis on WeWork. In the video, Damodaran goes through WeWork’s IPO and provides his own valuation of the company.

Damodaran’s valuation: $14B.

The issue is clear. Even under high growth assumptions, the company isn’t worth nearly as much as SoftBank paid.

At this point I wish the company went public at $47B so I could’ve backed up the truck on shorts. Oh well, there’s always Peloton ;).

Clifford Sosin Wants to Change Banking

When he’s not looking for great investment ideas, Clifford Sosin spends his time trying to change the banking system. In their whitepaper on bank reform, Sosin and Peter Blaustein team up to tackle one of banking’s biggest problems: procyclicality.

The paper goes deep into the weeds on banking, capitalization and regulation. We’ll try to break things down into their first-order concepts.

-

- The Problem: Banking presents high procyclicality from money and finance. Crises amongst banks has a cascading effect on the economy and causes recessions.

- The Solution: Reduce procyclicality from money and finance.

- The Mechanism: Positive Book Equity Recourse Notes (PBERN)

At this point you’re probably asking, “what in the hell are PBERN’s?” Good question.

According to the paper, PBERNs are “10 year constant payment bonds with monthly payments, with the feature that any interest or principal payments payable would be paid in stock at a pre-specified price when (a) the stock is lower than a pre-specified price and (b) tangible equity value is negative.”

And yes, this is out of my circle of competence as well.

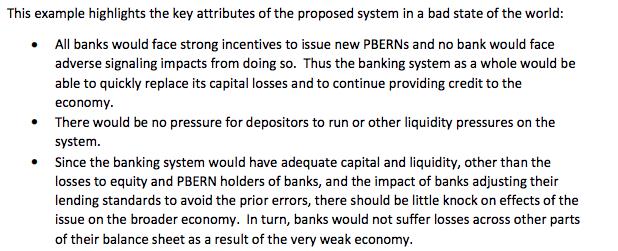

What would this new banking system look like during an economic crisis? Sosin and Blaustein paint us a picture (from the paper):

To conclude, Sosin and Blaustein argue that replacing equity requirements with PBERN requirements would increase the utility in elastic money supply. This would in turn reduce the severity of banking crises.

PSA: Give Cliff a follow on Twitter. His twitter account is like an undervalued, overlooked stock. He posts (and retweets) thoughtful content and is quick to respond to questions.

_______________________________________________________________________

Who Won Twitter? — Value is Back (Steven Wood)

Better to be early than never! As of last week value stocks seem to be in vogue.

Of course this is a ludicrously small sample size. But can the trend continue? Will value once again have its day in the sun?

_______________________________________________________________________

Bonus Round

GIFs by tenor

Like a Marvel movie, it pays to stay until after the credits here at Value Hive. I’ve got two more resources for you this week:

-

- CEO’s Guide to Capital Allocation, BehavioralValueInvestor.com

- What Investors Can Learn From Operators, Adventur.es

We love hearing from the Value Hive community! If you came across an interesting story, a super cheap stock or a funny history tidbit, let us know! We want to hear from you.

Tell Your Friends!

Do you love Value Hive?

Tell your friends about us! The greatest compliment we can receive is a referral (although we do accept Chipotle burrito bowls).

Click here to receive The Value Hive Directly To Your Inbox!