Our Value Investing Letter Recaps keep things simple.

Each email focuses on three value investing hedge fund letters, three ideas, all digestible in roughly three minutes.

Within each idea we answer four main questions:

- What does the business do?

- Why is it a good bet?

- Why does the opportunity exist?

- What is the prize if you’re right?

Quick housekeeping note that nothing you read is investment advice and please do your own due diligence before investing. Also, I do not own any of the below-mentioned securities as of this writing.

Finally, we get each investment letter from r/SecurityAnalysis, which you can find here.

This week we analyzed Magellan Financial (MFG.ASX), BJ’s Wholesale Club (BJ), and Arrow Electronics (ARW).

Let’s get after it.

Top 3 Value Investing Letters You Need To Know About

–

1. East72: Magellan Financial (MFG.ASX)

Andrew Brown runs the East72 fund, which we’ve featured many times in these Value Letter Recaps. One of our prior ideas, Manchester United (MANU), delivered exceptional returns after buyout rumors.

So whenever East72 releases a letter, we read it. Check out their latest Q4 letter here.

This week, we’re analyzing the fund’s latest long idea: MFG.ASX

What does MFG.ASX do?

Via TIKR.com: “MFG is a publicly owned investment manager. It invests in global equities and global listed infrastructure markets across the globe.”

Why is it a good bet?

“Retail funds management takes a long, long, long time to die.

In the early – mid 2000’s funds management businesses crudely changed hands with rules of thumb: 1% of fum for institutional, 3% for “masterfund/wrap” and 5% for “pure retail”.

These might have been rules of thumb, but they had a basis in analysis based on simple discounted cash flow metrics centered around fees, client tenure, costs and margin. Effectively, a LTV18 calculation is divided into prevailing FUM.

The three classes of investment customer are certainly morphing into each other, especially the latter two. So retail is not quite as sticky as it once was, as groups of advisers, aided by “best interest” laws and shielded under their professional indemnity insurance by ratings agencies, do see money move around.

However, even a cursory analysis of the company who did it all before MFG – Platinum Asset Management (ASX: PTM) – shows that despite substandard marketing and inconsistent medium term performance (below) there is still a substantial and lucrative business.”

Why does the opportunity exist?

“The jealousy that pervades analysis of MFG stems from the chart below, which shows that from December 2009 when funds were $602million, global equity FUM (measured quarterly) peaked at $85billion in June 2021 – just under 54% CAGR through 11.5 years.

We estimate MFG now has global equity institutional funds (excluding infrastructure) of below $7billion at December 2022 – around one-third of the SJP mandate; we estimate infrastructure funds to be ~$1billion less than this. All but ~$400million of Airlie’s $8.5billion of FUM is institutional. The rapid decline of MFG institutional funds shows the domino-like effect of this type of money.”

What is the prize if you’re right?

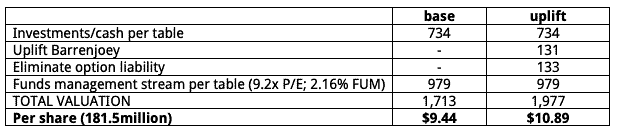

“We conservatively value MFG at $9.44/share based on 31 December 2022 FUM; being more liberal, we see scope to lift this to just under $11/share based on eliminating the option exercise liability and revaluing the Barrenjoey investment to reflect the entry price of Barclays:

Whilst the 31 December 2022 MFG share price is only marginally below our base valuation, we see multiple areas of optionality for MFG to add shareholder value. Our valuations offer nothing for the capacity to generate performance fees, nor the inherent beta to equity markets – which we acknowledge may take time to play out.”

Further Research Material

–

2. LVS Advisory: BJ’s Wholesale Club (BJ)

Luis Sanchez is a familiar name on the Value Letter Recap series. He runs LVS Advisory and has a great Twitter account (follow him here).

The LVS Defensive Portfolio ended 2022 up 3.8%, a fantastic achievement. Its Growth Portfolio declined 35.8% during the year. Check out the full letter here.

This quarter Luiz dissects his latest investment in BJ’s Wholesale Club (BJ).

Let’s dive in.

What does BJ do?

“The business is a discount wholesale club like Costco but focused on a more middle-class income demographic (Costco tends to skew higher income). BJ’s charges an annual membership fee of $55 to $110 and delivers extreme savings of 30% on average compared to traditional grocery and general merchandise stores. This is a strong value proposition for a family that shops once or twice per month for household essentials.”

Why is it a good bet?

“Discount retailers tend to outperform during recessionary periods as well as inflationary periods when consumers are looking for bargains. During the 2008/2009 recession, discounters such as Dollar General posted strong sales comps. We studied several discount retail concepts this summer and determined that BJ’s presents the best longterm opportunity”

Why does the opportunity exist?

“With just 226 store units compared to Costco’s 847 units, BJ’s has a significant opportunity to grow its store base and is currently accelerating new unit openings”

What’s the prize if you’re right?

“Investors appreciate the quality of the wholesale club model and have awarded Costco a 32x price-to-earnings multiple. Despite BJ’s being a ‘Costco clone’, its stock only trades for 17.5x earnings – a near 50% discount(!).

Putting it all together, I believe BJ’s is an attractively priced stock with a business that is high quality, economically durable, and has a long runway to reinvest for growth.”

Further Research Material

–

3. Vlata Fund: Arrow Electronics (ARW)

Vlata Fund is always quick with releasing their quarterly letters, which is greatly appreciated.

I recorded Daniel Gladis’s Q4 letter in my latest Investor Audibles series (listen here). This week, we’ll dig into their latest long idea: Arrow Electronics.

You can read along here.

What does ARW do?

“ARW is usually thought of as a simple semiconductor distribution company, but it also provides an interesting offer of value added services that creates deep ties with its customers. In essence, ARW provides economies of scale by acting as an intermediary between a highly diversified supplier base and a fragmented customer base of more than 220,000 customers.”

Why is it a good bet?

“Arrow Electronics (ARW) is a high-quality company with an attractive return on capital and strong growth in earnings per share.”

Why does the opportunity exist?

“[ARW] is often overlooked by investors because it is a seemingly boring company in the technology sector.”

What is the prize if you’re right?

“[Distributors] can be very attractive if well and efficiently managed. In looking at its long-term results, ARW appears to us to be just such a company. What’s more, we bought its shares at a historically very low valuation.”

Further Research Material

–

Wrapping Up This Week’s Value Investing Letters: What To Read Next

Thanks for reading, and I hope you learned something. If you enjoy this series, let me know by shooting an email or retweeting on Twitter.

Also, please let me know if there’s an investor letter I should read that I didn’t cover here.