Our Value Investing Letter Recaps keep things simple.

Each email focuses on three value investing hedge fund letters, three ideas, all digestible in three minutes.

Within each idea we answer four main questions:

- What does the business do?

- Why is it a good bet?

- Why does the opportunity exist?

- What is the prize if you’re right?

Quick housekeeping note that nothing you read is investment advice and please do your own due diligence before investing. Also, I do not own any of the below-mentioned securities as of this writing.

Finally, we get each investment letter from r/SecurityAnalysis, which you can find here.

This week we analyzed Lazard (LAZ), two small community banks (MFBP and CZBS), and Box.com (BOX).

Let’s get after it (all emphasis added).

Top 3 Value Investing Letters You Need To Know About

1. O’Keefe Stevens: Lazard Asset Management (LAZ)

This is O’Keefe’s first appearance on the Hedge Fund Investor Letter Recap series. Dominick D’Angelo runs the advisory firm and pitches LAZ in their Q3 letter, which you can read here.

What does LAZ do?

“Lazard (LAZ) has two business segments, an asset management business focused predominantly on equity investments and an Advisory segment where they assist clients with M&A, Restructuring, and other strategic initiatives. Over the past three years, Advisory and Asset management revenues have been roughly 50/50.”

Why is it a good bet?

“Our goal was to gain exposure to an asset manager with an equity focus over a company focused on growing its Fixed Income and Alternative Investments base. Lazard’s investment strategies are tilted toward value investments. This style gives us confidence that assets may go from a net outflow to a net inflow as the value rotation continues. Additionally, the risk of owning unprofitable, pie-in-the-sky ideas is reduced when investing with Lazard …

Lazard’s Financial Advisory business, specifically the restructuring business, is set to see an uptick in demand. Rising interest rates and tight capital markets force companies with debt-laden balance sheets to reorganize. The countercyclical nature of this segment can help offset lost revenues in other segments that perform poorly during periods of stress.”

Why does the opportunity exist?

“As with most active managers, fund outflows have occurred over the past several years, while fees have decreased marginally from 51bps to the high 40s. Aware of this headwind, Lazard’s active management fees remain below a typical active manager’s.”

What is the prize if you’re right?

“The company has raised the dividend from $0.36 in 2006 to $2.00 in 2022, paying out special dividends along the way. The company has also repurchased over 25m shares over the past three years.

The capital-light nature of this business should result in increasing dividends and buybacks. Finally, we believe Lazard could be an acquisition candidate by either an Asset Manager or Investment Bank.”

Further Research Material

2. Cedar Creek Partners: Citizens Bancshares (CZBS) and M&F Bancorp (MFBP)

Cedar Creek is another first-timer to the Value Investing Letter Recap series, and they’re coming like a wrecking ball. Their Q3 letter, which you can read here, highlights a “once in forever” investment opportunity in tiny community banks.

What do CZBS and MFBP do?

“M&F Bancorp (MFBP) is a North Carolina based bank that has run rate earnings as of the second quarter of $1.85 per share. As we write this the stock is $17.50. There are less than two million shares outstanding …

Citizens Bancshares (CZBS) is an Atlanta, Georgia based bank with similar characteristics. Its shares have jumped a bit due to the write up on twitter I mentioned above. Citizens has roughly 2 million shares outstanding. Shares traded last at $23 per share.”

Why is it a good bet?

“[Re: MFBP] A buyer is paying under ten times earnings for a bank with the potential to see earnings potential triple if it acquires a bank earning $7 million after merger synergies, or roughly $6 million currently …

[Re: CZBS] Earnings for the first half of 2022 were about $1.60 per share, but that is inflated due to a $1.8 million grant. Q2 EPS excluding the grant were roughly $0.55 per share. Thus, Citizens is also trading at around ten times its earnings run rate …

M&F Bancorp and Citizens have relatively small securities portfolios that have to be marked to market and large cash and deposits at other banks. Citizens had $360 million in cash and deposits versus its $832 million of assets. A ridiculous 43% of assets. That is a lot of capital that can be deployed at higher rates, whether 4% Treasury bills or 7% mortgages. M&F Bancorp had $135 million in cash versus $450 million in assets. While still an attractive amount, it is 1/3 less percentage wise than what Citizens had.”

Why does the opportunity exist?

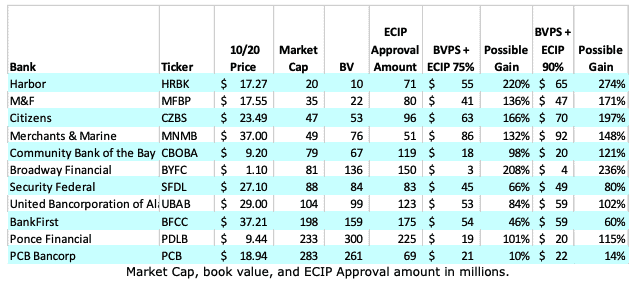

“Thanks to funding through the Emergency Capital Investment Program (ECIP) these two banks received capital equal to two to three times their book value (or market value). This funding is in the form of perpetual noncumulative Preferred stock.

Thus, the banks have more capital than most banks and are thus able to withstand negative events to a greater degree. Since the funding is in the form of low yielding Preferred stock, the common stockholders have nearly all the upside from the increased earnings potential of the additional capital.”

What’s the prize if you’re right?

“When we first started buying M&F and Citizens their future P/E was under two times using this approach, which meant we were expecting a 5-6x return within three or four years. Since both have nearly doubled in price, future expected return is now 2-3x over four years.

We would stress that the timeframe assumes organic growth. An acquisition can bring the increased earnings almost immediately. Thus, we have a base case of 2-3x in four years, with an upside scenario of 2-3x in one year …

A simple discounted cash flow comparing the preferred to the market price of bank preferred with a hypothetical 7.5% yield will result in a fair value of 10-25% of face value, thus the bank (i.e. common shareholder) is essentially being gifted 75-90% of the face value of the preferred.”

Further Research Material

3. Whitebrook Capital: Box.com (BOX)

Basil Alsikafi is the portfolio manager at Whitebrook Capital, another first-time guest to the Investor Letter Recap series. This quarter, Basil pitches BOX, a stock the fund’s held for the last three years.

You can read Whitebrook’s Q3 letter here.

What does BOX do?

“Three years ago, Box was an enterprise software company focused on document collaboration. The company’s competitive advantage was born from its security and governance capabilities that allowed it to succeed in regulated industries and the superior number of integrations with other services that made it easy to use a single file across functions.”

Why is it a good bet?

On almost all fronts, the Company is stronger today than it was then …

The Company’s growth has accelerated on the back of pricing changes by its competitors (now charging for storage for large enterprises) and the greater demands put on information workers and therefore the requirements of their document storage. Their competitors’ offerings, particularly the free ones, were always great for ~85% of use cases, but as the world’s workforce started working hybridly/remotely, the boundaries of those offerings were run into more often and Box’s extended capabilities in comparison have become more obvious …

Moving forward, as investors, we can expect the Company to continue this motion, offering higher margin services on top of the infrastructure they’ve already built while increasing the compellingness of the platform.”

Why does the opportunity exist?

“There was significant opportunity in its sales and marketing expenditures which were relatively inefficient. The Company was overly dependent on partners to penetrate larger enterprises and generally struggled to sell to the mass enterprise market despite its superior product.

From a financial perspective, the company had line of sight to operating profit breakeven and robust free cash flow generation when excluding the cost of stock based compensation, but had a history of missing Street expectations …

The company had a difficult time delineating to investors what differentiated the company from Microsoft’s OneDrive and Sharepoint, Google Drive, Dropbox, and a host of less sophisticated sync and share offerings.”

What is the prize if you’re right?

Their capital allocation has also improved, now buying back stock andusing M&A to add features to their platform … Over the near term, despite their flawless execution over the past year or so, I believe they’re likely to miss headline earnings because of their outsized exposure to the Japanese Yenand the extent of that foreign exchange rate adjustment. I continue to like the stock over the medium term however and we continue to hold.”

Further Research Material

Wrapping Up This Week’s Value Investing Letters: What To Read Next

Thanks for reading, and I hope you learned something. If you enjoy this series, let me know by shooting an email or retweeting on Twitter.

Also, please let me know if there’s an investor letter I should read that I didn’t cover here.