Our Value Investing Letter Recaps keep things simple.

Each email focuses on three value investing hedge fund letters, three ideas, all digestible in roughly three minutes.

Within each idea we answer four main questions:

- What does the business do?

- Why is it a good bet?

- Why does the opportunity exist?

- What is the prize if you’re right?

Quick housekeeping note that nothing you read is investment advice and please do your own due diligence before investing. Also, I do not own any of the below-mentioned securities as of this writing.

Finally, we get each investment letter from r/SecurityAnalysis, which you can find here.

This week we analyzed CACI International (CACI), Sea, Ltd. (SE), and News Corp (NWSA).

Let’s get after it.

Top 3 Value Investing Letters You Need To Know About

1. Upslope Capital: CACI International (CACI)

Upslope founder George Livadas makes a second appearance in our Q3 Value Letter Recap series this week. The fund returned -4.7% in Q3 and is down -4.2% YTD.

You can read his Q3 letter here.

This week we discuss one of Upslope’s latest buys: CACI.

Let’s dive in.

What does CACI do?

“CACI provides specialized technology and consulting services, primarily to U.S. defense and intelligence agencies. The U.S. Army is CACI’s single largest customer …

CACI’s business is mostly split across Expertise (providing talent to government agencies – e.g. software engineers) and Technology (design and delivery of specific technology-oriented services and products, including for example, battlefield hardware). The company offers its services and products in support of both day-to-day agency operations and specific missions.”

Why is it a good bet?

- “Long-term Geopolitical & Other Tailwinds – like other components of Upslope’s defense basket, CACI should benefit from an attractive defense spending environment for years to come. CACI should also benefit from IT modernization efforts in U.S. government agencies, as well as its strength in cyber/electronic warfare offerings.

- Strong Management – CACI’s CEO has been in-role since 2019 and previously served in various COO capacities for the company since 2012. His communication is unusually straightforward and clear, and his focus on “free cash flow per share” (despite underwhelming comp incentives) is notable. He is also a significant shareholder, owning $20mm+ of stock (and only one modest sale – in 2020 – during his history at the company).

- Attractive Financial Profile – CACI has a track record of solid organic growth (typically around mid-single-digit %) with limited cyclicality, supplemented with tuck-in acquisitions (for which there continues to be a long runway). ROIC is modest (HSD%) but stable. The balance sheet is nearly under-levered at ~2.5x net – providing flexibility for additional acquisitions or share buybacks.

- Healthy Earnings Backdrop – given strong geopolitical tailwinds, bipartisan support for defense, and a sizable gap between rising defense budgets and recent outlays (which typically come through on a lag and correlate with revenues for CACI/peers), the earnings outlook for CACI should be solid in the periods ahead. Such a healthy outlook is unusual in the current market/economy.

Why does the opportunity exist?

“High portion (~30%) of fixed price contracts (mitigant: solid track record of managing costs and, more importantly, significant diversification by project), lumpy organic growth, labor availability/challenges, M&A execution risk (very acquisitive and larger deals could present heightened risk), and potential government budget headwinds (depending on November elections and potentially driven by elevated inflation/rates longer-term).”

What is the prize if you’re right?

“Even if estimates do not come up, valuation on consensus figures today is modest, suggesting limited downside: 7%+ FCF yield, 11x EBITDA, 14x EPS. Notably, CACI peer ManTech was recently taken private by Carlyle Group at a premium valuation (5% FCF yield, 16x EBITDA, 26x EPS). The deal was announced in May 2022 and closed in September.”

Further Research Material

2. Hayden Capital: Sea, Ltd. (SE)

Fred Liu runs Hayden Capital, which invests primarily in fast-growing, e-commerce based businesses. The fund is down 18.9% in Q3 and 70.6% YTD. You can read Fred’s latest letter here.

This quarter Hayden dives deep into one of its larger positions, Sea Ltd. (SE).

Let’s explore the name.

What does SE do?

“[SE’s business evolution from] predominantly a republisher of mobile games, which just happened to be reinvesting all its profits into a fledgling ecommerce business – to one that now is the leading ecommerce platform across all of the Southeast Asia region with over 50% market share, in addition to self-developing one of the top grossing games of the past two years.”

Why is it a good bet?

“The company expects to achieve profitability via a combination of 1) increasing revenues via raising commission and advertising take-rates (essentially 100% incremental margins), while 2) reducing costs, especially marketing and logistics. To cover the remaining ~$1.3BN HQ costs, this equates to needing to find another ~16% of margin in order to become profitable over the next year …

This accelerated profitability timeline is impressive (it requires some real organizational flexibility) and makes the company stronger in the long run. But there’s a cost in the near-term. Growth over the next year is likely going to be slower than the previous budget, since this profitability will be achieved by reining in marketing spend while monetizing the platform quicker …

As long as Shopee is able to pull these two levers, it shouldn’t have a problem being profitable on its core business within the next 12 months. Afterwards, that would just leave the Brazil investment, at a current ~$1.1BN annualized. With the recent Shopee break-even target of 2023, it sounds like the company is confident that the SE Asia business will be able to make enough profits by next year-end, to cover the Brazil losses.”

Why does the opportunity exist?

“2022 has been tough for the company, with the entire region now reopened after Covid restrictions the past few years. This means consumers are spending more time inside brick & mortar retail, while record global inflation has been a drag on household budgets as well. We can see via alternative data providers, that these macro factors are hurting competitors (Lazada and Tokopedia) as well, with some even exhibiting negative year-over-year growth in some months …

Meanwhile, Shopee is facing these headwinds as well, but managing to hold its own and is performing better (orders grew +18% y/y in 3Q 2022). It now offers fewer discounts than peers, while still maintaining stronger user retention and order growth. It seems that despite the industry headwinds, Shopee is still growing its market position, and is proving out the stickiness of its user base (which was a big debate among investors just a few years ago).

However, Shopee is also facing some company specific headwinds as well. The capital market environment has changed drastically over the past year, and the company is being forced to reach profitability several years before it originally intended.”

What’s the prize if you’re right?

“Sea Ltd is valued at ~$32BN in market cap today18. The company has ~$7.3BN in cash as of last quarter, of which $4.2BN is likely reserved to pay the convertible debt that matures in a few years. That leaves ~$3.1BN of excess cash.

The market is currently debating how much (if not all) of the cash will be spent, before the business can be self-sustainable. For the sake of being conservative even further, let’s assume the entire excess cash balance will be spent on the road to break-even.

That means that after stripping out the Garena and Sea Money businesses, the market is currently valuing Shopee at ~$23BN. The market’s expecting Shopee profits to be ~$2.2BN at that point, implying ~10.7x 2025 EV / EBITDA for the ecommerce business …

In fact if Shopee were to be valued in-line with those at ~25x 2025 EV/ EBITDA, that would imply that Sea Ltd’s overall valuation should be $31BN higher, or +97% versus today’s price.”

Further Research Material

3. Irenic Capital Management: News Corp (NWSA)

This is Irenic Capital’s first appearance on the Value Letter Recap Series. And they’re doing things a bit differently.

The firm didn’t release a quarterly letter (at least not one that we could find). But instead, offered a pitch deck on their latest investment: News Corp (NWS/A). You can download the slide deck here.

So instead of highlighting written text, I’ll post pictures of slides that answer our four main questions below.

Let’s get after it.

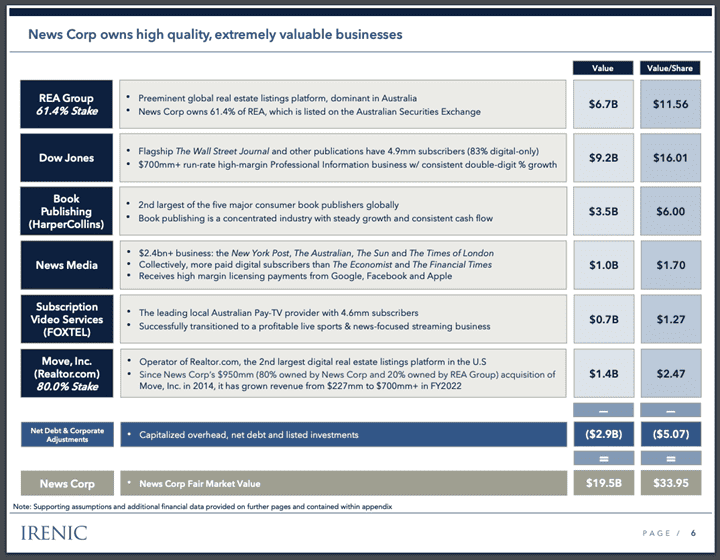

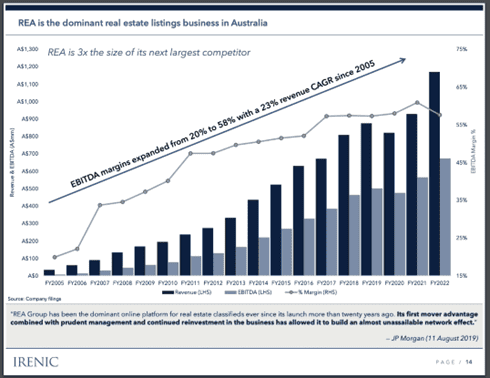

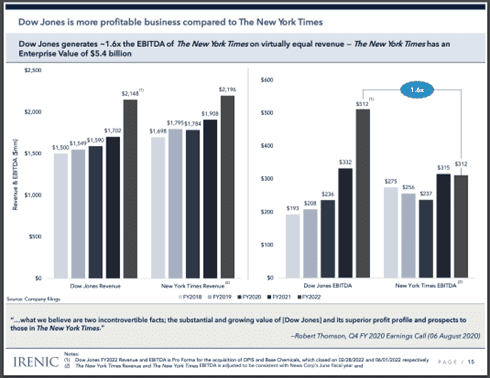

What does NWSA do?

–

Why is it a good bet?

–

Why does the opportunity exist?

–

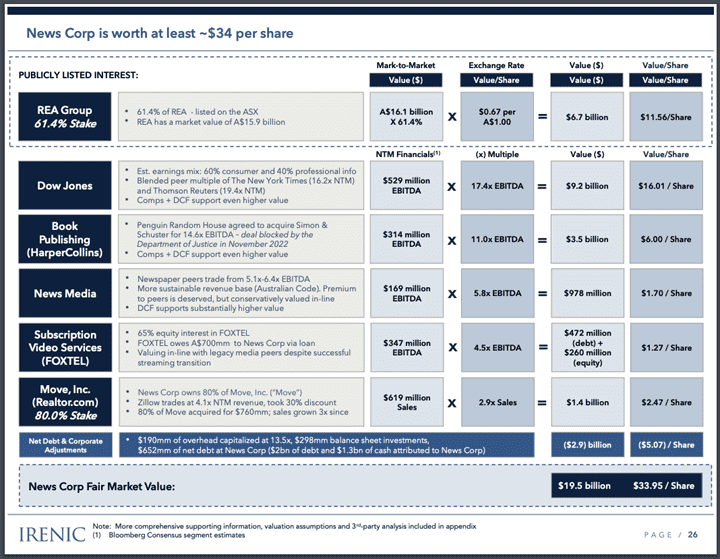

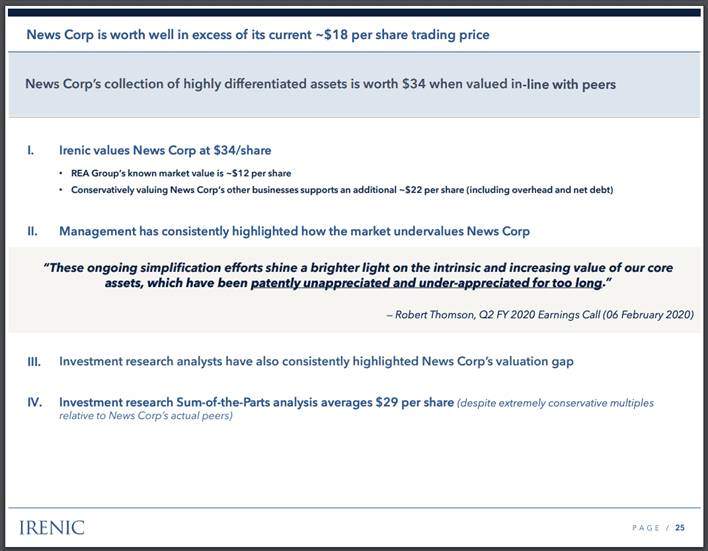

What is the prize if you’re right?

Further Research Material

Wrapping Up This Week’s Value Investing Letters: What To Read Next

Thanks for reading, and I hope you learned something. If you enjoy this series, let me know by shooting an email or retweeting on Twitter.

Also, please let me know if there’s an investor letter I should read that I didn’t cover here.