If I had a dollar for every time someone on Twitter mentioned inflation, I’d be on a beach sipping margaritas without a care. “Inflation? Never heard of her!”

Prices are rising for necessities like gasoline, eggs, meat, and mortgages. These price changes then ripple across the entire economy.

Consumers spend less, leading to contracting/declining business growth and even less spending.

Inflation becomes a wrench thrown in the gears of the “Economic Machine.”

The consequences of inflation affect asset prices, investing strategies, and forward returns.

At MO, we believe it’s a lot more important to know where you stand than to try and predict where you’re going. And if you can accurately diagnose the current environment then you can more effectively weigh potential paths forward.

That’s why we created this Primer on Value Investing Research and Inflation Effects. Think of it as your map to navigate a potentially sticky, higher-for-longer, inflationary environment. And if The Druck is right, get comfy. Because we may be spending the next decade here.

This Primer breaks down inflation analysis from value investors such as Buffett, Klarman, and Aswath Damodaran. We’ve pulled what we think are the most essential parts from each source and added current examples where appropriate.

We’ve included the original source material too so you can go deep down the inflationary rabbit hole if you so choose.

Consider this a living document. We’ll add sources, insights, and analysis over the coming months, so please don’t hesitate to reach out and contribute.

Understanding Inflation’s Effect on Asset Values

Before we dive into hot takes from investing legends, it’s crucial to set our base understanding of inflation and its effect on asset values. Let’s start with Inflation Theory 101 via Itamar Drechsler and Alexi Savov. (You can read their deck here.)

Here’s how inflation affects asset prices according to academic theory:

- Nominal Bonds: Prices decline since payouts are fixed

- Stocks: Stock prices are neutral since inflation is the rate at which firms increase prices

- Real Estate/Commodities: Value should be neutral to inflation

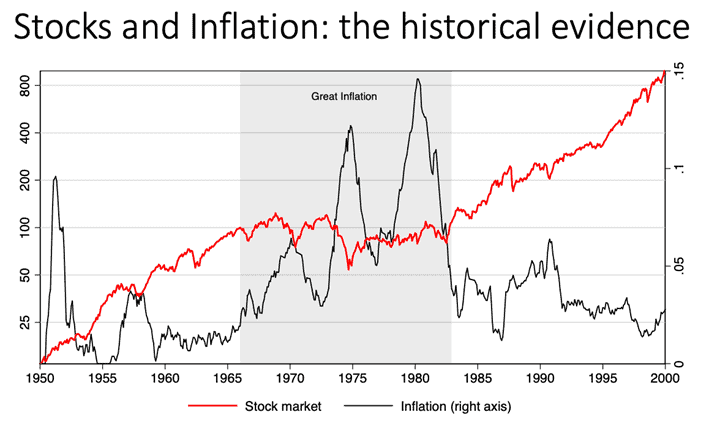

We care about stocks, so let’s see how they performed during The Great Inflation of 1965-1982.

Inflation’s Effect on the Stock Market

Stocks went nowhere during the 17-year inflationary period between 1965-1982:

This data differs from the academic theory that claims stocks pass-through inflation via higher prices.

So what happened? Let’s dive into how inflation affects the primary driver of stock returns: future cash flows.

How Inflation Affects A Company’s Cash Flows

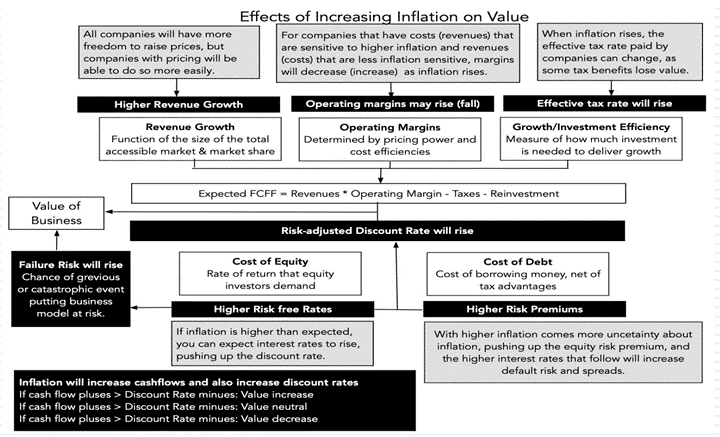

As a reminder, the value of any stock is the sum of all future cash flows discounted at an appropriate interest rate (think: return hurdle).

I love this graph from Aswath Damodaran showing how increasing inflation affects equity value:

We can split the above diagram into two parts: Revenue, Margins, and Taxes and Discount Rates. Let’s break each piece down into a more digestible format.

How Inflation Affects Revenue, Margins, and Tax Rates

- Revenues: Companies can “get away with” raising prices since prices for other goods/services are also rising.

- Operating Margins: Margins may rise (or fall) if a company’s COGS are highly indexed (or not) to inflation.

- Tax Rates: Effective tax rates rise as higher inflation leads to lower perceived value of tax benefits

Inflation isn’t a blanket “good” or “bad” for stocks. It’s company-specific. Can a business increase prices while maintaining its margin profile because its COGS inputs aren’t susceptible to inflation? If so, inflation is great for that company.

Let’s examine the other side of the value equation: Discount Rates

Higher Risk Premium = Lower Expected Values

It’s easy to get overly academic about discount rates. Here’s the most important thing to know about them:

A discount rate is an investor’s expected return hurdle to allocate capital to an idea.

Inflation acts as an amplifier to an investor’s discount rate. Here’s what I mean. The last decade saw historically low interest rates (0-2%).

Investors required lower return hurdles than alternative investments like bonds or corporate debt. Return hurdles declined because investors asked themselves, “can I generate at least a 2%+ return on this investment at the current price?”

That’s a low hurdle, so the answer (in most cases) was yes. However, the opposite happens in high inflation environments.

Higher inflation raises discount rates because it increases the return hurdle on an investment. Today’s market is a perfect example. Investors can lock in 4% returns on 2-year government paper.

So your hurdle rate automatically jumps from 2% to 4% before considering a public equity’s investment risk.

And as we saw above, higher inflation brings higher corporate risk as the cost of capital increases and investors have less certainty about the future. I like how US Economist Peter Bernstein puts it:

“When inflation is low, you feel that you know more about the future, and are much more willing to take risks.”

Here’s a helpful short-hand distillation of the above points:

- Higher Inflation = Higher Discount Rate

- Higher Discount Rate = Higher Return Hurdle

- Higher Return Hurdle = Lower Equity Values

Think about it this way. Investors could buy Bank Certificates (i.e. CDs) yielding 11% in 1980. How cheap would stocks have to be in that environment to warrant the risk of investing in public companies?

Here’s Aswath’s explanation on how inflation impacts equity values:

“In periods when inflation is higher (lower) than expected, individual companies can benefit, be left unaffected or be hurt by inflation, depending on whether the benefits of inflation (higher revenue growth and margins) are greater than, equal to or less than the costs of unexpected inflation (higher risk free rates, higher risk premiums, higher default spreads and higher taxes).”

Warren Buffett calls inflation a “far more devastating tax than anything that has been enacted by our legislatures.” Here’s his example of the “inflation tax” assuming a 5% inflation rate:

“The inflation tax has a fantastic ability to simply consume capital. It makes no difference to a widow with her savings in a 5 percent passbook account whether she pays 100 percent income tax on her interest income during a period of zero inflation, or pays no income taxes during years of 5 percent inflation. Either way, she is “taxed” in a manner that leaves her no real income whatsoever. Any money she spends comes right out of capital. She would find outrageous a 120 percent income tax, but doesn’t seem to notice that 6 percent inflation is the economic equivalent.”

I want to cover one more aspect of inflation, expectations.

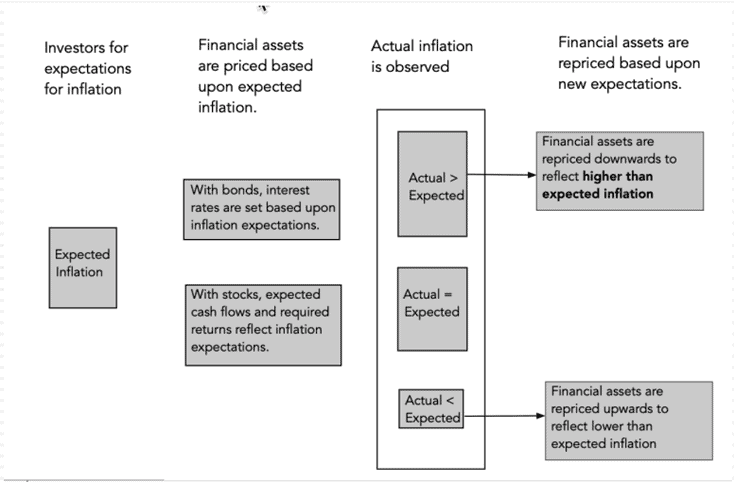

Second-Order Effects: When Actual Inflation is Less Than Expected Inflation

Inflation affects a company’s cash flows and its value/price. However, the real driver of asset prices isn’t inflation itself but expected inflation. And the varying degrees of expectations miss/deliver.

Check out Aswath’s chart below on how expectations regarding inflation drive asset prices:

It’s not high inflation that’s bad for stocks, but rather unexpected high inflation. Aswath expands on this idea in his Invest Like The Best podcast with Patrick O’Shaghnessy:

“Expected inflation to me is the more benign part of inflation. The part of inflation that’s deadly is unexpected inflation, which is inflation coming in higher or lower than expected. When inflation is unexpected, you’ve not had a chance to adjust to it.

We fell back on, “Inflation’s always been low,” because that’s the only thing we knew. So, I think it’s the unexpected inflation that I think is so damaging. What we’re seeing in markets right now is markets are trying to adjust to what’s the true inflation going to be. I mean, we all agree that the 8%, 9% that we’re seeing is probably too high a number, that some of it is supply chains, COVID excuses that were given early on.

But we all also I think finally agree that we’re not going to go back to 1% or one and half percent inflation, which is what we had in the last decade. The question of where we fall between the one and a half and the 8 or 9% is what’s driving markets. If inflation subsides back, the most benign scenario, goes back to 2%, which is supposedly the fed’s target, that’s the most benign scenario. But that scenario is becoming a lower and lower probability scenario the further we get into this process. At this point, the question is, will it go to 3? Will it go to 4? Will it go to 5? And adjusting from a 2% expectation to a 5% expectation is devastating for all financial assets. It’s not just stocks. It’s not just bonds. In any type of financial asset.”

By this point we have an academic understanding of inflation and how it impacts various asset classes. We also know how inflation actually affects companies and stock prices.

Given inflation’s “fantastic ability to consume capital,” we should do everything in our power to avoid investing in businesses that can’t withstand inflation.

But how do we do that? How can we invest so that we’re insulated from the damages of high inflation?

The following section answers those questions.

How To Invest In High Inflation Environments

First, let’s invert the question: “what would be the worst investment to make during periods of high inflation?”

The “worst” high-inflation investment would look something like this:

- Low gross and operating margins

- Most (if not all) of its COGS are highly anchored to inflation rates

- Cannot raise prices without severe customer substitution/trade-off

- Won’t generate cash flow until years into the future

- Requires additional (higher cost) capital to survive

- Product/Service is a discretionary purchase

These are your loss-making, nice-to-have software management tools (ASAN, EXFY, etc.), your furniture retailers (RH), restaurants with commodity-driven variable cost structures and operating leases, and fast-growing companies with promises of distant free cash flow generation.

As we’ll see below, you do not want to own companies in these industries during high inflation:

- Retailing

- Household/Personal Products

- Telecom

- Food Beverage

- Biotech and Life Sciences

I want to say something important here. It’s not that these aren’t good businesses. Some of them will become great, cash-gushing money printers. But they’re not great for the high inflation environment we’re in and might be in for the next decade.

So, what do you want to own?

Something like See’s Candy, a confectionery company. Let’s go back to Buffett. Listen to how he describes See’s Candy and why it’s a great asset to own during high inflation:

“See’s Candies does not take much in the way of expenses to operate, and doesn’t require heavy capital expenditures in order to consistently grow its profits every year.

Because consumers are loyal to the See’s brand, they eagerly absorb any pricing increases even during economic uncertainty and/or inflation.

With that valuable asset which is not accounted for on the balance sheet, See’s Candies is able to see its revenues grow as it increases prices while other expenses also rise.

But because those expenses are minimal, and See’s doesn’t take much capital to continue to mint free cash, its damages experienced from inflation are minimal, and the company is able to earn fantastic compounding rates of return for investors.”

See’s relied on three main factors:

- A capital-light operating model with minimal capital required to expand revenues

- Price inelastic customers willing to absorb price increases (brand power)

- Revenues rise with expenses resulting in minimal inflation damage

We can further extrapolate See’s success to identify characteristics that increase odds of survival (and even thriving) during high inflation environments:

- Non-discretionary good or service

- Currently generates positive free cash flow/earnings

- Mid-to-high gross and/or operating margins

- Subscription/recurring revenue model businesses (must be non-discretionary!)

- Some real asset attributed to the business (real estate or commodity)

- Value-biased businesses

We want to invest in businesses with high margins and COGS that aren’t tied to inflation. They should also have an ability to raise prices without consumers noticing/complaining/trading-down.

These businesses need to generate cash today and trade at a modest-to-cheap valuation.

Additionally, we want to invest in businesses that sell/leverage hard assets (like oil or real estate) — basically any business that sells the high-inflation COGS in another business’s expense line.

A Quick Word on Subscription/Recurring Revenue Models

Recurring/subscription-based businesses are only great inflation hedges if consumers deem it a non-discretionary purchase decision. In fact, the best subscription businesses are stickier than long-term debt.

Vista Equity Partners CEO Robert Smith calls these recurring revenue companies “better than first-lien debt.”

Smith continues his analogy, saying:

“You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.”

However, as Gavin Baker of Atredis Management explained in his 2020 Medium post, “There is no such thing as truly recurring revenue. Some revenue is just more recurring than other revenue.” Double-check to see if that subscription really is a mission-critical/non-discretionary expense.

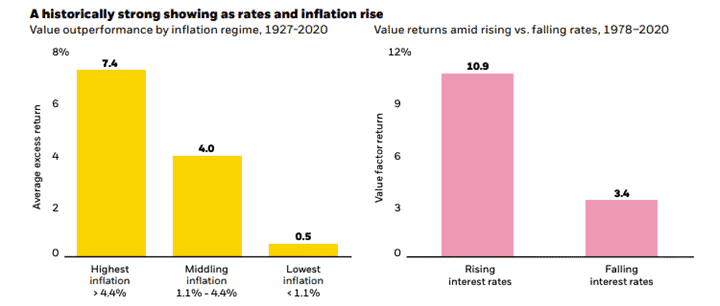

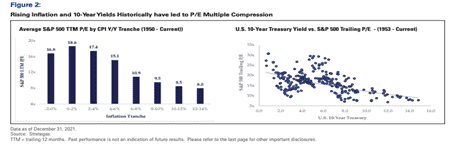

Data Tells All: Value Outperforms During High Inflation

BlackRock published a report highlighting the importance of buying value over growth during high inflation periods:

As BlackRock notes, Value dramatically outperforms during high inflation and rising interest rate environments.

One reason for Value’s outperformance is the fact that high inflation periods bring multiple compression (P/E ratios shrinking). Boston Partners highlighted this correlation in an inflation whitepaper (read here).

Boston Partners also explains how interest rate changes disproportionately affect growth stock valuations: “Growth stocks are longer duration assets compared to their value counterparts as a significant portion of growth company cash flows are further into the future. Like the bond market where 30-year bonds will lose more value if rates rise 1% compared to 1-year notes, growth stocks will lose more value relative to shorter duration value stocks in a rising rate/inflation environment.”

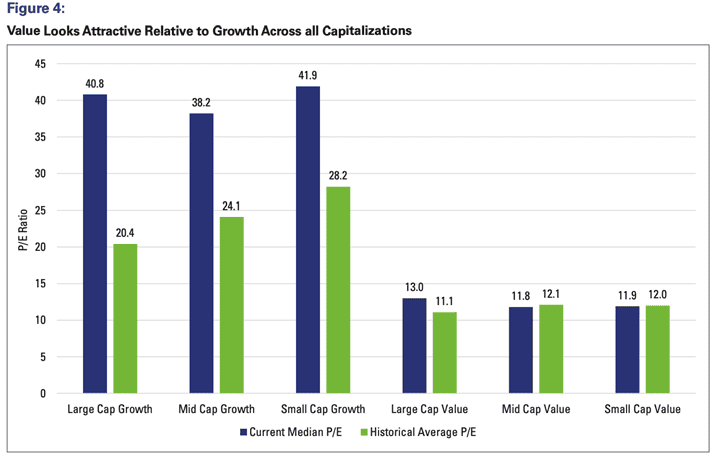

Boston Partners also found that the “Value over Growth” dynamic applied across all market capitalizations (see below).

If you believe in base rates, the above chart should scare you away from investing in high multiple businesses during inflationary environments.

What Industries Offer The Best Returns?

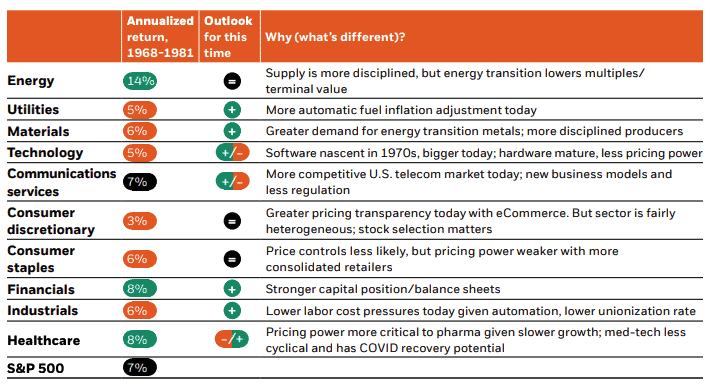

BlackRock noticed that three industries outperformed all others during high inflation periods: Energy, Financials, and Healthcare.

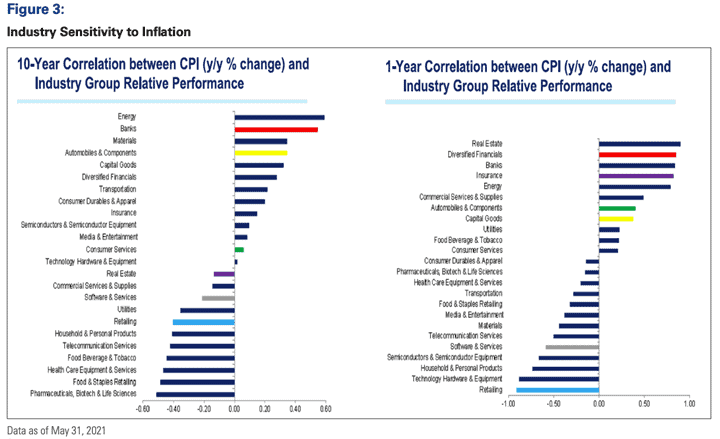

Boston Partners confirmed this data, highlighting Energy, Banks, and Materials as the three highest-returning industries based on CPI correlation (see below).

GMO takes this analysis a step further and suggests that there are only three main drivers of investment outperformance during periods of high inflation:

- Cheap real assets (think value stocks)

- Oil (and oil stocks)

- Coal (and coal stocks)

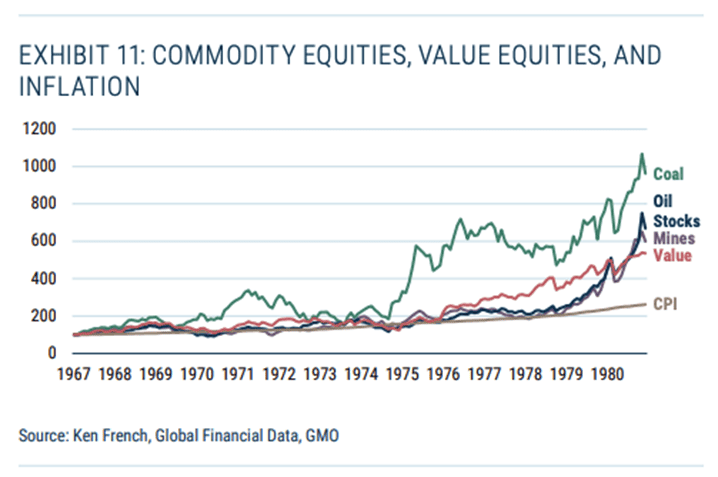

Here’s a quote from GMO the whitepaper titled Part 2: What to Do in the Case of Sustained Inflation: What if We’re Wrong?:

“During the last bout of significant inflation, commodity equities were a good store of value (unlike the underlying commodities), and so were value stocks in general. Why? Effectively, you were buying cheap real assets. This is like being offered inflation insurance at a discount. So if you are worried about inflation and looking for a store of value, or you are trying to build a robust portfolio that can survive lots of different outcomes, then buying cheap equities looks like a great place to start.”

They also have the performance data to back it up (see below).

The Value Investing Research Guide To Inflationary Investing

What worked over the past ten years may not work for the next ten. Our job as investors is to align our approach with the regime. And to do that we need to know what approaches work in which regimes.

Hopefully, this short primer helps you be a little bit better at both.

Markets are incredibly fascinating. The puzzle pieces are always moving and shifting, like inflation!

And for us at Macro Ops, we get the added benefit of being able to play this incredible game with you.

It’s a joy to wake up every day and jump into the Comm Center (our private slack) where all our Collective members are working hard to solve these “page sixteen” puzzles together.

The truth is that markets can be a lonely game. Macro Ops fixes that.

And now we have a community that makes this endeavor more enjoyable and fulfilling than we ever thought possible.