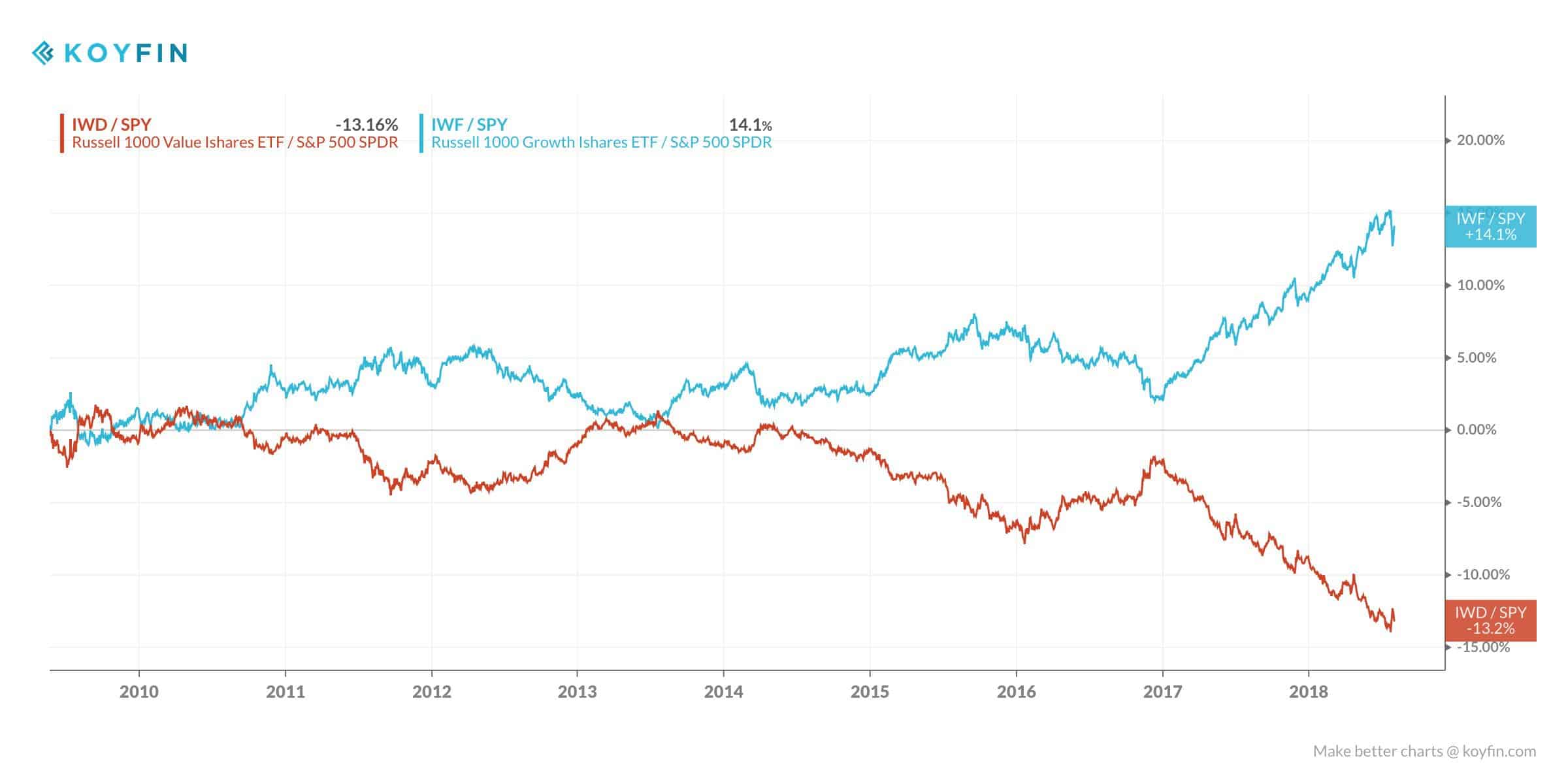

Value investing hasn’t performed so well this cycle. Here’s a chart showing value’s relative performance versus that of growth.

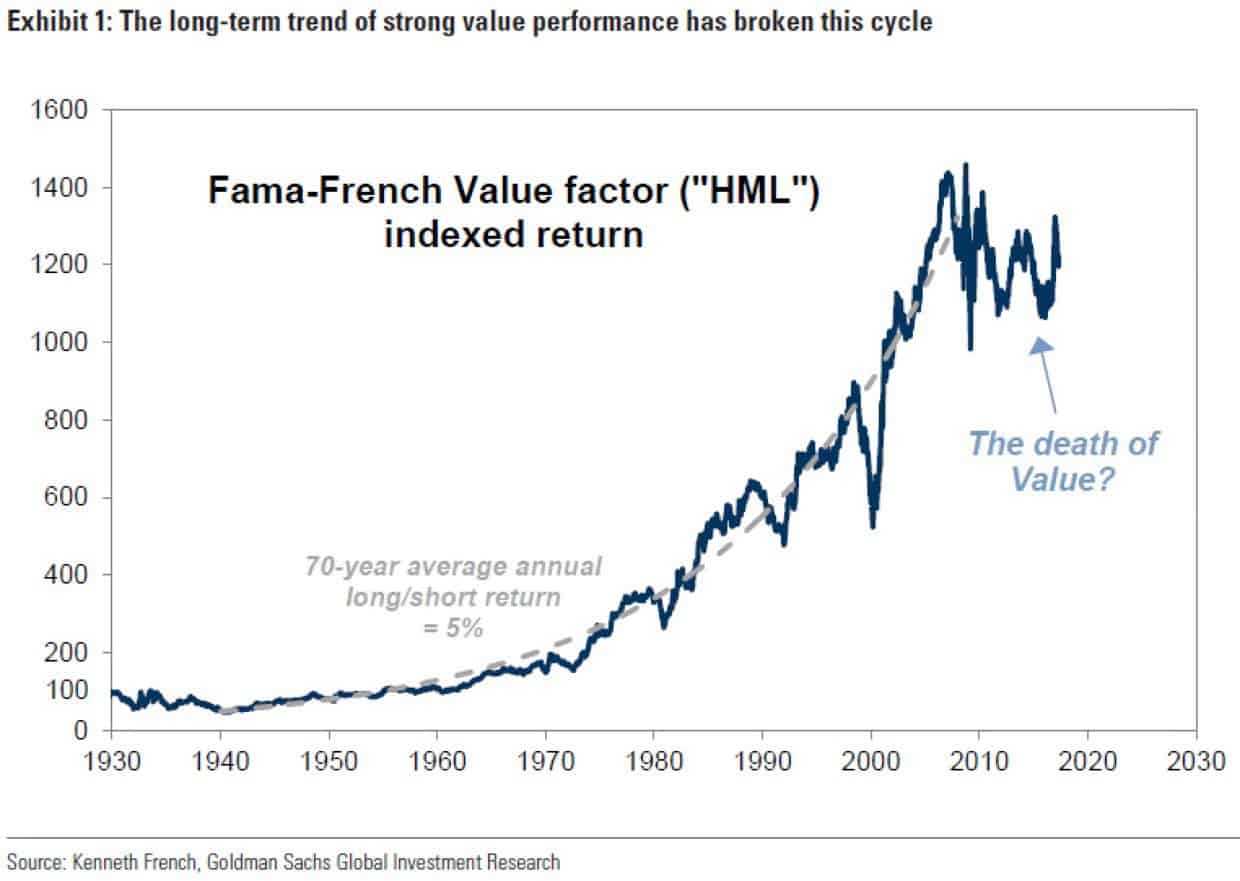

The value-factor strategy pioneered by Fama and French, which consists of buying stocks with the lowest valuations and selling those with the highest has produced a cumulative loss of 15% over the past decade, according to Goldman Sachs.

This is the longest stretch of underperformance for the value-factor strategy since the Great Depression.

And as to be expected, this prolonged drudgery has spawned the hyperbolic “Death of Value Investing” narrative that seems to come around at some point every other cycle.

What I find interesting though is that this “death of value” narrative doesn’t seem to be affecting the value fund managers I talk to. They mustn’t have gotten the memo because they seem to be doing just fine — actually, much better than fine with most of them beating the market by a wide margin this cycle.

Which of course begs the question: why the large performance gap between what’s considered classical value (ie, the Famma-French method of buying statistically cheap stocks) and select discretionary value fund managers who’ve been hitting it out of the park?

The answer is two-fold.

- Quantitatively arbitraged: Back in Benjamin Graham’s day getting hold of a company’s most basic accounting information was difficult. Figuring out classical value metrics such as price to book and price/earnings required a great amount of effort (the information simply wasn’t readily available). Today, every Joe Schmoe has access to free quantitative screeners that scan, decipher, and rank every stock in the world according to a long list of metrics. If a stock sells for a low price to book or earnings yield then it almost certainly deserves it. Put simply, the widespread availability of quantitative systems has arbed much of the alpha out of looking at the popular valuation metrics.

- Asset-light economy: Famed value investor, Bill Nygren of Oakmark Funds, recently wrote that “as the economy has become more asset-light, intangible assets — such as brand names, customer lists, R&D spending and patents — have become more important.” Nygren goes on to note that “the relative importance of tangible assets compared to intangibles has completely flip-flopped from what it was 40 years ago” and that now, intangibles “account for over 80% of the average company’s market value.” The funny thing is, standard GAAP accounting doesn’t even attempt to measure these assets!

So the headlines above decrying the death of value investing are right… at least sort of. Classical quantitative value investing has become a packed house and the edge has been competed away. But value investing still lives on… just in a new and evolving discretionary framework.

The core-tenets of value investing remain the same. The goal is still to buy companies at below the present value of their future cash flows. But the frameworks used for discerning this value have changed.

Value fund manager Joel Tillinghast puts the aim of value investing as this, “I’m looking for companies that are increasing the amount by which their intrinsic value exceeds their accounting values. This difference is called economic goodwill.”

Discerning “economic goodwill” takes discretionary research and deep thinking. It’s not easy and you won’t find a metric for it on any quantitative website, which is largely why it works.

The value managers that are thriving in this environment are the ones who’ve recognized this changing dynamic and have evolved their process along with it. This group of adaptable managers includes the old Oracle himself, Warren Buffett, who has said, “My own thinking has changed drastically from 35 years ago when I was taught to favor tangible assets and to shun businesses whose value depended largely on economic goodwill.”

As a global macro operator I’ve been fascinated with the changing landscape in value investing. Though we don’t ascribe to a certain narrow and rigid approach to markets, such as being strictly fundamental or trend following practitioners etc…Our approach at Macro Ops is, and always has been, to make high risk-adjusted returns by whatever means necessary. And value investing is one of these means.

Because of this, I’ve spent the last few years studying and dissecting the habits, practices, and frameworks of the very best in this evolving value investing landscape.

And in this month’s Macro Intelligence Report (MIR) I’m going to share all that I’ve learned. We will discuss the foundational principles of value investing and then I will walk you through MO’s framework for seeking out and properly analyzing highly asymmetric value investments. We’ll then apply this framework to three deeply mispriced value stocks that I’ve been digging into the last few months.

All three have multi-bagger potential and won’t pop up on any standard quantitative value screens. They are examples of where the quantitative metrics and GAAP accounting numbers obscure their true potential.

If you want access to my top three value stocks for August 2018, sign up to the MIR at the link below.

Click Here To Learn More About The MIR!

There’s no risk to check it out. We have a 60-day money-back guarantee. If you don’t like what you see, and aren’t able to find good trades from it, then just shoot us an email and we’ll return your money right away.

The S&P looks ready to break out to new highs on the back of strong US economic data. I think these three multi-bagger value stocks can start their run as soon as next week. Don’t miss out, sign up for the August MIR by clicking the link below.

Click Here To Learn More About The MIR!