Tyler here with this week’s Macro Musings.

As always, if you come across something cool during the week, shoot me an email at alex@macro-ops.com and I’ll share it with the group.

New MIR Report Out Soon Sign Up Now: In this month’s MIR, we’ll be revealing our highest conviction asymmetric macro trade idea for the end of 2018 and start of 2019. On top of that we’ll be talking about our process for short-selling and pitching some interesting plays that fit within that framework. To cap it off the report will end with a Greenblatt style hidden value spinoff. Lot’s coming for the month of November!

We have a 60-day money-back guarantee, so there’s literally no risk for you to read about our latest ideas. Sign up to the Macro Intelligence Report by clicking here.

Recent Articles/Videos —

China Won’t Bail Out Global Markets This Time Around — Alex explains why China will shy away from injecting liquidity into the system right now. It’s very unlikely we’ll see a reversal in policy until the end of 2019, at the earliest. This matters big time if your trying to time the recovery in EM.

Articles I’m reading —

The Critical Turtle Trading Teacher William Eckhardt: Launching 1000 Systems — Eckhardt began trading futures in the 1970’s and also ran the famous Turtle Trader program alongside Richard Dennis. He’s considered one of the founding fathers of the modern day CTA industry.

This article is in interview format with Futures Magazine and spawns a great discussion on the Efficient Market Hypothesis that I agree with.

Futures Magazine: Many in the traditional investment world cling to the notion that markets are efficient. Trend-following is not valid under the efficient market hypothesis (EMH) but here you are 30 years later. Why has the EMH persisted? Talk about this anomaly.

Bill Eckhardt: The random walk model of price change has been so durable because it’s nearly correct. The difference between futures prices and certain random walks is too small to detect using traditional time series analysis. Incredibly, this difference is detectable using trading systems.

Markets are tough to trade because most of the time there just isn’t any edge. The current price accurately reflects all known information. But once in awhile things line up to create a fat pitch where price is clearly wrong. That’s when we have to take a hard swing.

Chart I’m looking at —

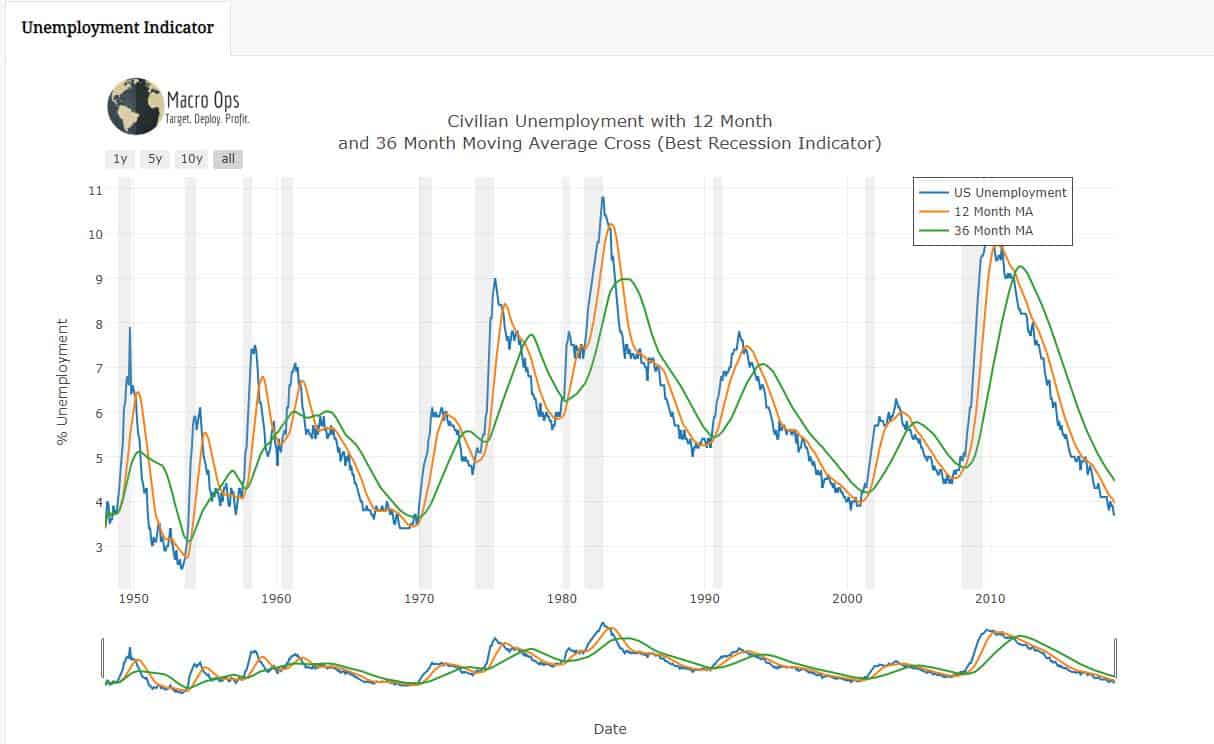

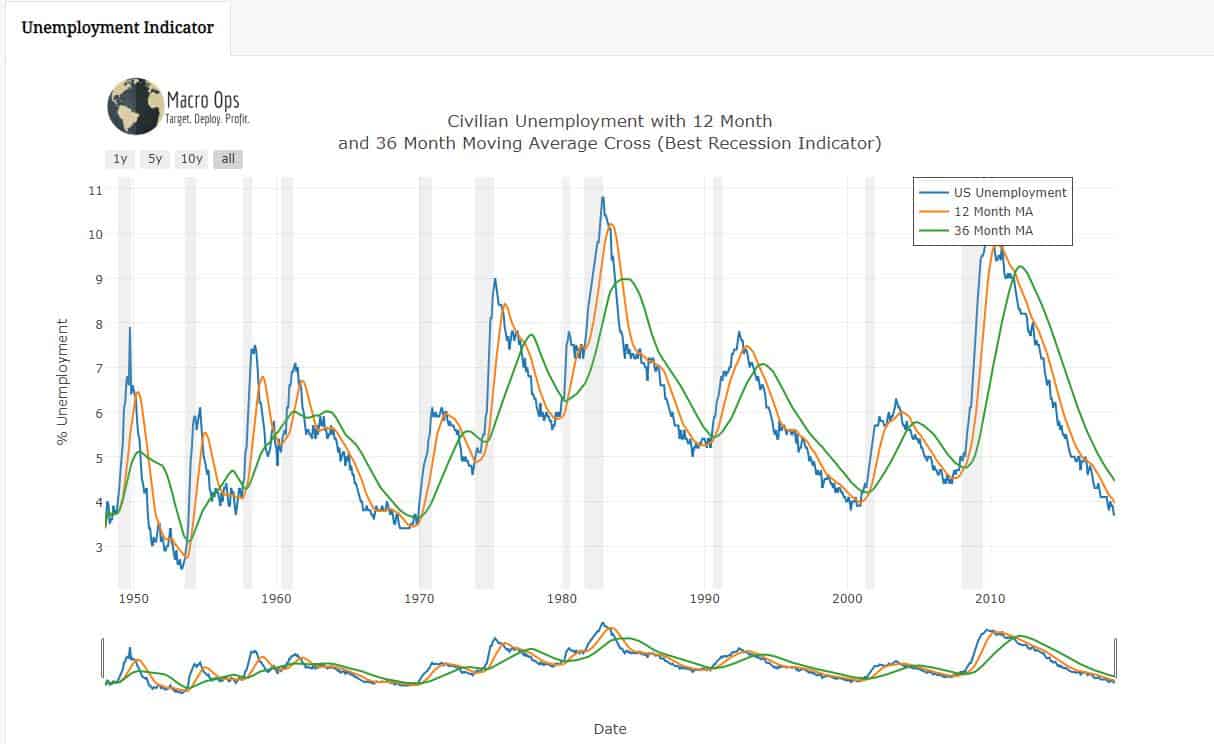

The stock market decouples from the real economy quite often. Fear, greed, news, risk control algos, performance chasing and a plethora of other stuff can cause wild gyrations up and down in the broad indices. But those moves don’t stick and continue unless the real economy follows.

That’s why I like keeping an eye on the trend in unemployment. It’s rare for the stock market to have a deep continued sell off without job loss starting to accelerate higher. Before the 2000 bear market and the 2008 bear market, unemployment started to scream higher and breach its 12-month and 36-month moving averages. Bears need to be cautious here in our opinion until the unemployment rate reverses in a meaningful way.

Trade I’m considering —

Energy commodities move in capital cycles. High prices lead to more investment which eventually leads to over-capacity and a supply glut which then drives prices lower sending the process in reverse. Low prices force inefficient producers to shutdown and others to scale back. Eventually these low prices drive excess capacity offline which then leads to tight supply and higher prices. And the cycle begins anew — rinse and repeat.

The Uranium market is at the trough of its capital cycle. CAPEX has shrunk big time as uranium prices have been in a brutal bear market for the last decade.

We’ve taken a couple of shots at some uranium miners over the last two years but with limited success. Price has continued to trend sideways… It’s tough to time when these capital cycles turn.

But now uranium has hit its highest level in more than 2.5 years as big producers of the nuclear fuel buy material in the market and China prepares to reaffirm its plans to build new plants.

We’re taking another research dive into the uranium to space to figure out if this is finally the time that the capital cycle reverses. In the past, one of our favorite picks for this theme has been Cameco (CCJ).

Video I’m watching —

A historic Wall Street documentary — This was shot somewhere between 1920 and 1960 (according to the website). If you watched PTJ’s documentary “Trader” from the 1980’s you’ll get a kick out of this short film too.

Taleb Says World Is More Fragile Today Than in 2007 — Taleb came on Bloomberg TV this Halloween to talk about how we still haven’t solved the leverage problems from 2008. Instead we just shuffled paper around and transferred private debt to the government. He says eventually the US government will hit a point where they won’t be able to borrow enough to service interest payments so they will be forced to inflate the debt away instead. That in turn means high or possibly even runaway inflation. Taleb goes on to explain that he holds gold and land to preserve his wealth for when that time comes.

Quote I’m pondering —

Remember that big stack poker is a game of patience. You don’t have to make a big play in every marginal situation that comes along, just as a good hitter in baseball doesn’t have to swing at balls outside the strike zone. Wait for good solid situations before making big plays. ~ Dan Harrington

Wait for those fat pitches!

That’s it for this week’s Macro Musings.

If you’re not already, be sure to follow us on Twitter: @MacroOps and on Stocktwits: @MacroOps. Alex posts his mindless drivel there daily.